Editor's Note: Below is a brief excerpt transcribed from today's edition of The Macro Show hosted by Hedgeye CEO Keith McCullough. Click here to learn more about The Macro Show.

Keith McCullough: First on Asia. It was a bloody mess. This situation in Hong Kong becomes Macro Tourist type news. You get the Hang Seng down another -2% overnight which puts its crash at -23.7% since the cycle in all of Asia peaked in Q1 of 2018.

So again while it is touristy to talk about protests the point is the precipitating factor behind all this has been Asia slowing, Europe slowing and Emerging Markets slowing for some time now.

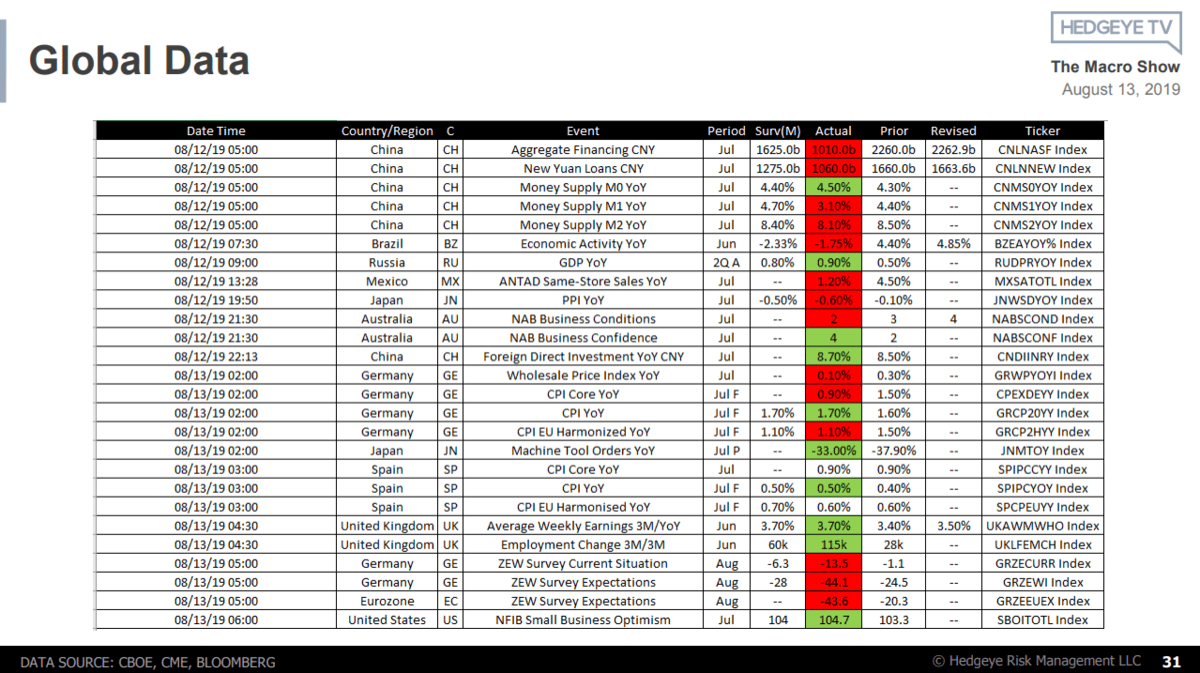

As you can see in the data, there is absolutely red. The German data looks like hell. This bearish economic data is against easing comparisons. The cycle has been slowing for going on 19 months.

The other side of global growth slowing is India and Thailand both cut interest rates last week. People on CNBC would probably assume that stocks go up on rate cuts. No. Thailand is down a full -2% post the rate cut.

This is what happens when you get deeper and deeper into the rate cutting cycle. People start to realize, and even our illustrious central bankers acknowledge it, that the economy is slowing.

McCullough: Point number two is the curve. You subtract the 10-year Treasury yield from the 2-year Treasury yield and you have +6 basis points left. It’s so small you can barely see it. If you look at the 5-year relative to the 2-year yield it’s -8 basis points. That’s inverted. It’s hard to believe but the curve looks worse today – i.e. it’s flatter and more inverted – than it did in December when credit stopped trading. So if you ever hear anybody say, ‘Nobody could’ve seen this coming,’ it’s staring you right in the face this morning.

The final point that’s related to the yield curve is the Financials (XLF). The last thing on earth you should have in your portfolio right now is a U.S. bank stock. You know that right?

Our subscribers are not long the Financials, which are down almost -6% in August alone. We’re only 13 days into August. That’s a terrible thing to have in your portfolio, even on any bounce because the trend remains definitively bearish.

The other side of that is REITs (VNQ). That’s been a beauty.