This could be an important week for our VVV call given 13Fs are due. The stock has performed very well since we made it a Best Idea Long on 6/1/19, especially in a tough market. There are a few things we think are driving the stock higher… the quarter's results, potential activists building their positions, and a possible flight to safety as concerns over macro rise, with VVV being a relatively low cyclicality name within consumer.

What Changed With the Quarter

Investor confidence in management may have been the area that saw the biggest inflection in this quarter. Afterall this was the first quarter in the last 6 where the company beat revenue and didn’t have to temper expectations around the North America DIY issues. Perhaps management finally has a grasp on the issues at hand, and the actions are working to improve performance on the margin. But we don’t think full confidence in management simply from this quarter is well founded. Regardless, any investor was happy to see improvement on the margin in Core NA as it means better visibility to the downside vs prior trends. Also, we definitely like the persistent strength displayed VIOC, which we think will continue to exceed expectations.

Where We Stand

At $22 we're still buyers of VVV. If the stock heads much above $25, we think a spin is likely priced in. From there the upside in the stock will be driven by VIOC outperformance and growth over time. Over 1-3 years we see another 30-60% upside from the full realization of the VIOC value as it scales.

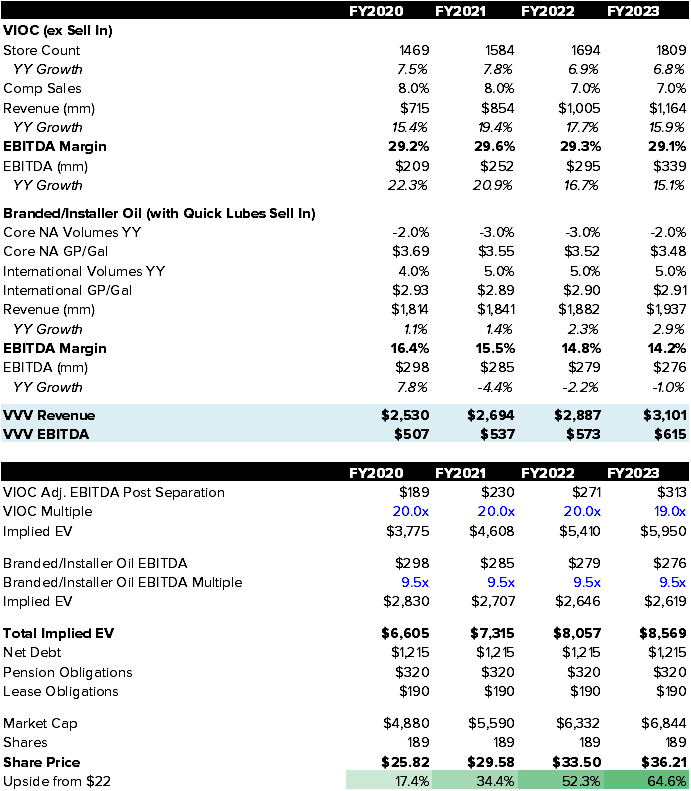

In terms of the model, though we don’t have street segment estimates for Quick Lubes or VIOC (which is one of the core reasons for us making the activist spin call in the first place), we think the biggest variance in our model vs the street is VIOC revenue performance. We see higher store growth than guided, and we expect comps to be toward the higher end of the long term guidance range. After reviewing the results of the quarter and following up with the company, we are slightly accelerating our store growth, slightly revising up near term comps, and we are taking up profitability slightly with opportunities from leveraging the planned cost cuts, as well as the potential of a product cost tailwind from base oil downward price revisions given the move in crude oil and our current macro view of slowing inflation in 3Q19. Also, given the improving rate of change for Core NA, we're taking up our multiple for the Branded/Installer Oil RemainCo to 9.5x EV/EBITDA.

Activism Timeline

Let's face it, it is unlikely the stock is going to attract new activist attention at these levels. However we think the chance of one or more activists currently owning the stock is probable. The relative price performance means there was clearly incremental buyers given the low short interest. If a single activist took a large stake in this, there is a decent chance we would have heard about it by now. However we think given the attractiveness of the VVV opportunity in the 17s, there could have been multiple activists buying in June, perhaps keeping their stake's lower. This week is 13-F week, and we'll keep a close eye filings for who might be involved here. As for hearing about a real activist campaign, remember nominations for director must be received no earlier than Oct. 3 and no later than Nov. 2 2019 for consideration for the 2020 annual meeting. So there is a decent chance we could hear something over the next few months. If we don’t it doesn’t nullify the activist play, just obscures the catalyst timeline.

For a full replay and slide deck of our Long VVV Black Book CLICK HERE