"How can I prepare for what comes next?"

That’s a question we’ve been understandably receiving a lot lately from investors after a sharp selloff in U.S. equities (and the huge rally in what’s been our favorite allocation for some time now… U.S. Treasurys).

We hosted a special edition of The Macro Show earlier this week to dissect our Macro team’s call on the ‘Bearish Black Hole’ in financial markets and the associated investing implications.

Below are some key takeaways (and important charts) transcribed from this edition of The Macro Show hosted by Hedgeye CEO Keith McCullough.

* * * *

Keith McCullough: This is the biggest thing that investors should be talking about for the next two to three months and that’s earnings. The Macro Tourists are jumping from headline to headline, from rate cuts to Yuan devalation to Trade wars. You notice that? There’s an anxiety to that – jumping from headline to headline instead of from time series to time series.

Earnings is a time series. A cycle. It is slowing. It is slowing faster this morning. ISM Services– which is a momentum indicator of the U.S. consumption economy – just hit a 35-month low. Not 35 days. A 35 month low. Not shockingly the ISM Services number peaked at the peak of the economic cycle in September at 60.8.

McCullough: What is slowing growth going to mean for Q3 earnings? If you watch Old Wall TV they’ll tell you, ‘The U.S. consumer is in great shape.’ That means absolutely nothing to me. It’s a qualitative assumption that is complacent at the core.

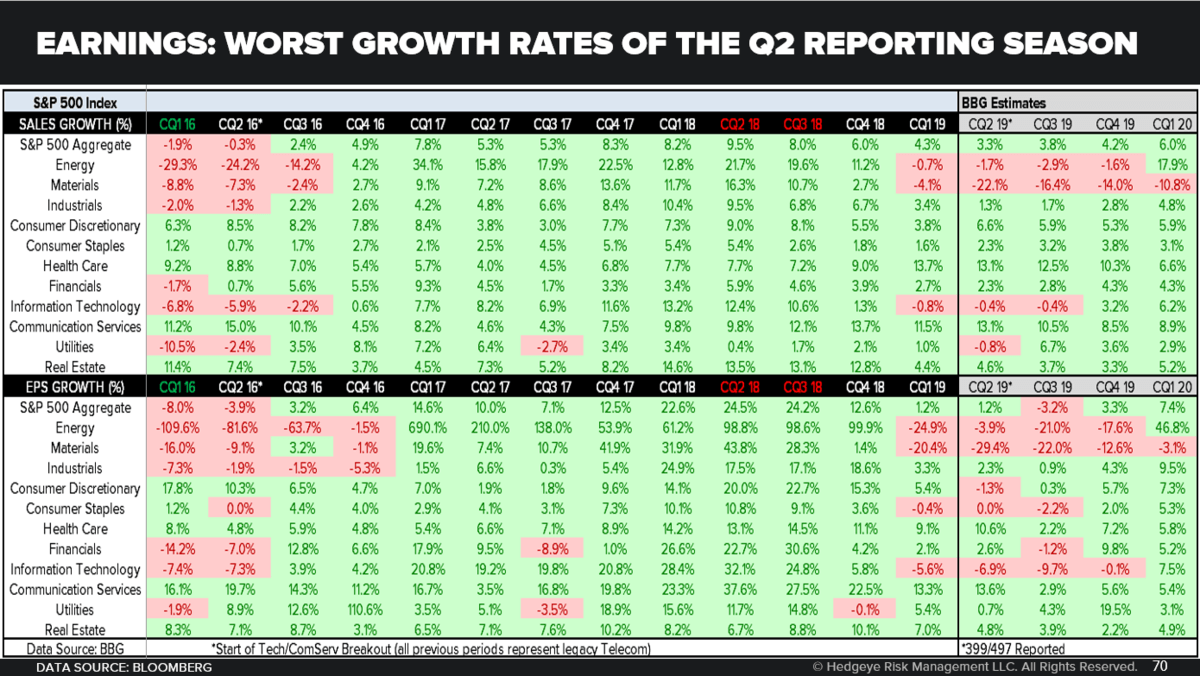

What I care about is the rate of change in Growth, Inflation and Earnings. As you can see in this chart here, we’re now currently at the slowest growth rate for earnings so far in the second quarter. 399 of the S&P 500’s companies have reported aggregate year-over-year (y/y) growth of +1.2%. That’s down from +12.6% EPS growth in the prior quarter and having fallen from the peak growth rate of 24.5% in 2Q 2018.

And now Consumer Discretionary earnings are negative for the first time. You have Tech and Consumer Discretionary – the most complacent and over-owned sectors of the U.S. stock markets – that now have negative earnings.

Tech has down -6.9% year-over-year earnings growth. That’s a very bad situation that continues to develop there. This is alongside the credit risk that continues to develop and the widening of credit spreads in Tech and Consumer Discretionary too.

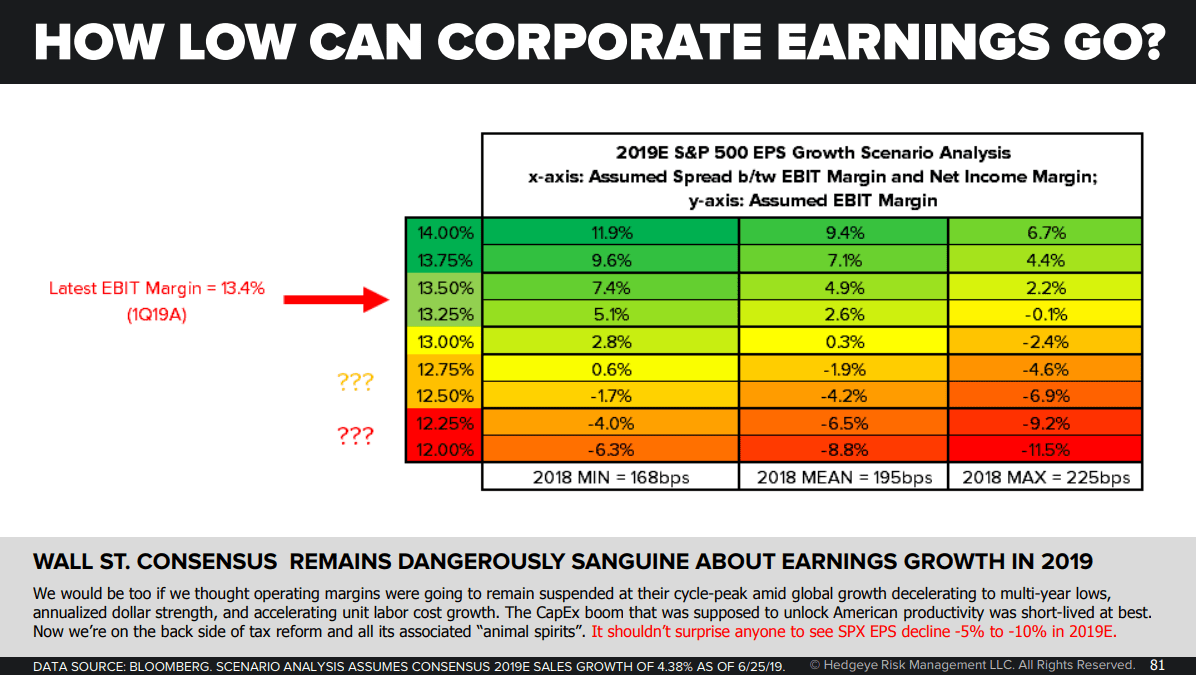

Our scenario analysis suggests that even a modest degradation of EBIT margins could translate into year end S&P 500 earnings declining by -5% to -10% in 2019. Wall Street certainly isn’t prepared for that.

McCullough: On China, the Chinese did exactly what I said they’d do and that’s tone down the currency move they created. At the end of the day they control that part of the game and they wanted to remind Trump that’s the case.

On the news, the rest of the world, including China, piked to a lower-low. The Shanghai Composite dropped another -1.6%. There really was no progress in terms of a trade deal or economic activity. You can flush that into the Kospi, which continues to crash this morning. The Kospi is a broader barometer of Asian economic activity, as an exporting nation. The Kospi continues to crash falling another -1.5% to down -25.5% versus where we got you out of China, Emerging Markets and all of Europe in the first part of 2018.

Daryl Jones: There’s a question from a subscriber about how functionally do the Chinese devalue the yuan.

McCullough: That’s easy. They sell the Yuan. When you’re trying to command and control something you sell it to make it go down and buy it to make it go up.

Jones: Basically, to devalue they increase the supply.

McCullough: Exactly. The problem with the Chinese here is that they’re short dollars. This is not your grandpappy’s Chinese yuan.

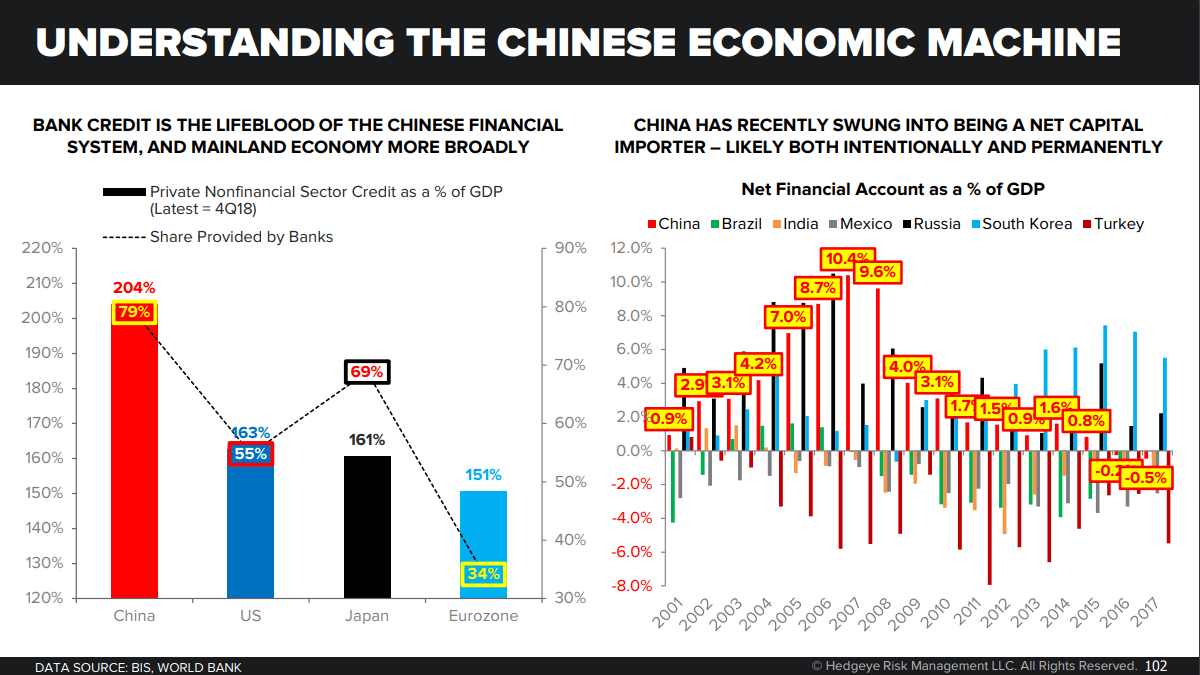

If you look at slide 102, the Chinese have massive amounts of leverage on any relative or absolute score. On the left hand side of that chart we’re showing Chinese private nonfinancial sector credit. On the right hand side of the chart, in sharp contrast to prior cycles and specifically throughout the 2000s when China was running a current account surplus, they now have not only a closed capital account but a current account deficit developing.

That means to fund the deficit they have to fund things in dollars. So they are basically short dollars. They need dollars. They do not need to do what they did to the currency to make their point. I think that was a 1-day to 1-month move.

People are saying what the Chinese just did is the most important thing since the Plaza Accord. I don’t believe that. From here they’re not going to let the Chinese yuan go like some Emerging Market currency. By the way, a traditional Emerging Market currency that does not have a closed capital account is subject to massive outflows.

But that’s not what’s happening in China because they have a closed capital account. That’s what people have had wrong about China for many years. They have wholeheartedly ignored the fact that there are different mechanics at play.

McCullough: Let’s talk about volatility. Volatility broke out. A VIX above 15 is a lot different market environment than VIX below 15. The top end of the VIX risk range is 27.34 and the low end of the risk range (or the vol of vol) is at the former top end of the range from the prior day. A very dangerous set-up.

So no matter how much the S&P bounces this morning, it’s what you’re going to learn on the bounces that matters most. Don’t forget that the S&P 500 broke its intermediate-term Trend line of support at 2924. It did hold 2820, which is our long-term Tail risk line. If it breaks below 2820 all hell would break loose and everyone on CNBC will be citing more Dow Bro 800-900 point down days. Be careful of that.

Measuring and mapping the vol of vol is important to measuring and mapping investor anxiety. After 6 straight down days you get the bounce. As you can see here, there have been three different times that you could have lost a lot of money chasing charts. We don’t want you chasing charts when everyone on the Old Wall tells you the smoothing mechanism or the 50-day Moving Average is safe. That doesn’t work.

McCullough: I’m showing you the tools that I use and have developed over the last 20 years, not only as a hedge fund manager but as an analyst and now your risk manager. I also run my personal accounts using the same exact tools. So if you do care to learn, let’s get into it. After six down days in a row, today’s risk range for the S&P 500 implies -0.8% downside (at 2820) versus +4.2% to the upside (or 2964). So there’s more upside than downside for today. That makes a lot of sense.

If you look at the volume underneath the hood yesterday, what you’d see is an explosion of volume and an explosion of volatility to the upside. We measure and map that across durations. The 1-month average volume was up 25%. So yesterday was a capitulatory day.

It already happened in options space. If you look at implied volatility data you’d see implied volatility premiums explode to the upside, with 66% being the implied volatility premium on the S&P 500. That’s one of the many reasons why you don’t short SPYs on the lows here. You’d expect a bounce.

So what happened? This morning we’re now close to the top end of the VIX risk range. We’re near the low end of the risk range for SPY, right on the screws, with a big explosion in implied volatility premiums. That means people are panicking and having to hedge after coming into the move not hedged.

Only one month ago you’d see implied volatility discounts, meaning expectations in the futures market suggests investors weren’t that concerned. We called it a black hole. Wall Street was on the wrong side of this.

But getting back to the big call here. The biggest thing that investors should be talking about for the next two to three months is earnings and the U.S. economy slowing. If we’re right on both of those and Quad 4 conditions persist, you’re going to be glad you didn’t panic about the Chinese Yuan and how that’s bullish for stocks.

Everyone keeps asking ‘Is the bad news priced in?’ Unlike consensus FOMO, I didn’t think so at the highs of April or July.