As much as I’d like to say that this is the quarter to press the HBI short, the reality is that it’s probably not. We’re in-line on EPS at $0.45 and ahead on revenue as we think the Innerwear puts and take are a net positive in 2Q, and we don’t expect a miss in Champion. The revenue upside we see is likely given back on SG&A as the street number looks too low as the company is spending for its growth in Champion brand. Guidance will likely ignore the risks we see to 2H numbers, so we definitely want to be shorting on strength ahead of 2H and 2020 earnings misses. We think the model relative to expectations gets much tougher in the back half where we are 9% below the street, and we would get heavier on HBI if we see any rally on a revenue beat and inline EPS without a guide down.

Innerwear Puts & Takes

The expectation and guidance is for Innerwear growth in 2H to be better than that of 1H. We think that is unlikely to be the case due to the following:

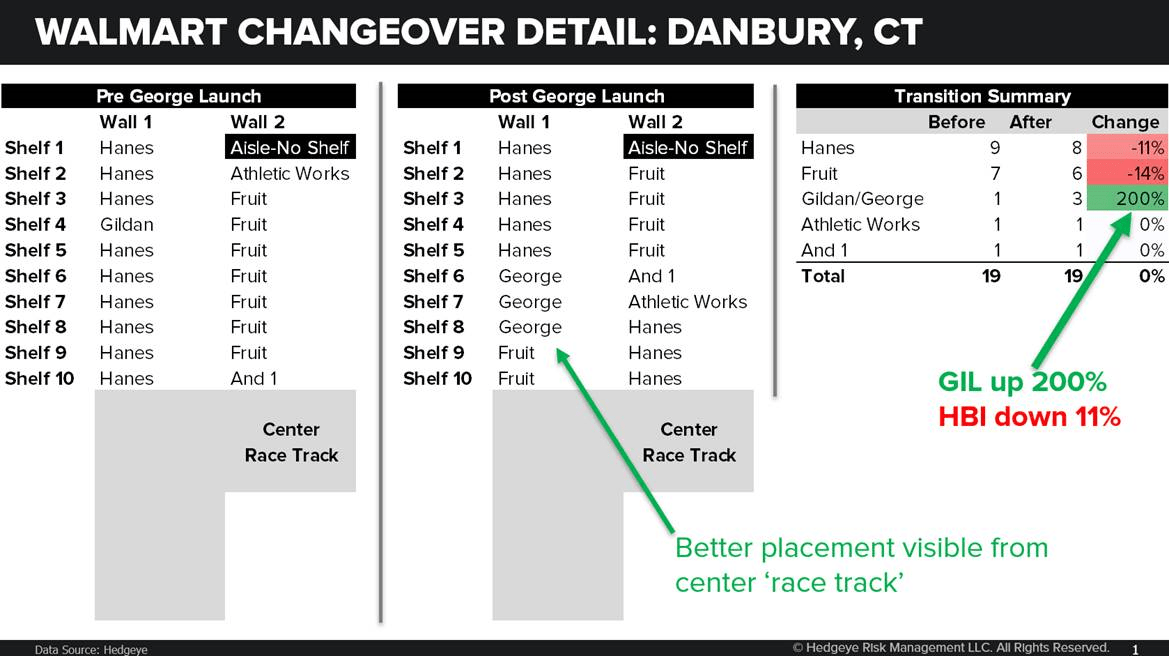

George Brand: We think the WMT George private label launch will ultimately be a clear negative for HBI unit share. After all, it’s the first private label program for WMT in Men’s basic underwear.

The timing of the impact could be a little squirrelly. George was rolled out to WMT stores starting in May (mid HBI 2Q). There were some weeks leading up to the changeover where Gildan product saw little to no in-stocks, which may have been a temporary unit share opportunity for Hanes. So perhaps 2Q sees a muted impact relative to what we expect in 2H. The George assortment appeared to continue to be rolled out or expanded in store as late as thr end of June from our store checks.

Looking at the changes in shelf space in the stores (illustration below), we saw George/GIL space expand anywhere from 50% to 200% in a 3 store sample. Also some stores upgraded the location and presentation of the George brand to be more visible and accessible from the main “racetrack” in the Walmart apparel section. The shelf space changes mean the risk to HBI space is anywhere from 5-15% across the store fleet, and given the placement and investment for Walmart in the brand, we think unit velocity risk could exceed the space losses. That translates to something in the range of 150-400bps of incremental Innerwear pressure.

Dollar General: On the last call HBI indicated it was replacing a private label sock program with Hanes in the discount channel. Turns out to be replacing Gildan inside DG, which was rolled out in June. We see it as $20-$30mm in revenue potential for Innerwear annually, with heavier impact to 2Q due to the sell-in this Q. We confirmed with GIL that it chose to end this program based on margin profile. GIL probably requested better pricing/margins and DG declined deciding instead to switch to Hanes. It’s unlikely Hanes margin / terms are any better than what GIL had, otherwise it wouldn’t be worth switching for DG. So there is a small help to Innerwear revenue here, but the margin and earnings flow through will be small.

Door Closures: With the DG ‘win’, it’s important to remember the secular pressure on sales from HBI losing its doors of distribution as retailers shut them down. JCP is closing stores in 2019, as well as Family Dollar, and of course Sears/Kmart. Door closures will continue to be an issue putting negative pressure on Innerwear growth.

Champion

Our gauge on Champion brand interest on google in 2Q looked to be similar to 1Q, though slowing from the peak seen in late 2018. There was talk that Champion could be rolling due to discounts inside URBN. We’re not surprised to hear about discounting, the brand is notably over distributed (see our note HBI | Champion Distribution Case Study). Does discounting mean the brand is now suddenly losing favor with the consumer now? Not necessarily.

Our view on Champion is that inventory is building at retail for demand growth that simply won’t be there, and it eventually will lose favor with the consumer. So it ultimately blows up, probably sometime in the next 18 months. The brand will see revenue declines, and the stock likely tests new lows.

The company guided a Champion growth number for the first time last Q stating it would be in the area of ~40%. So Champion is likely to slow materially this Q from the +75% 1Q result, but perhaps Champion beating that guide is a risk now for shorts.

C9

We still don’t think C9 risk is in expectations. It is ~$450mm in revenue with $66mm in Innerwear and the rest in Activewear that is going to comp down materially in 2H, then likely go to zero in January. Given the price points and single customer nature of the brand, we think its margin is above company average and likely close to an Innerwear margin. The company stance on C9 in its FAQ last quarter was not bullish.

Q: Can you provide an update as it relates to your plan for C9 after the January 2020 transition?

A: We continue to see significant momentum building globally within the Champion brand (excluding C9) and we are focusing our energy and resources on maximizing this business. While there may be an opportunity in the future to build the C9 brand with another retailer, we currently do not have any plans in place.

HBI has no new agreement locked up with the clock ticking, the odds of C9 finding a new home are low from where we sit.

FX

With a third of the company sales now international we have to keep an eye on FX. The topline drag from FX is fading, last Q was ~2.5% this Q looks like just under 2%. At current exchange rates, FX remains a drag over next 12 months.

Cotton & Tariffs

Cotton should be inflecting here in mid 2019 from headwind to tailwind. The impact for HBI isn’t that large, but still a 10% move is in the area of 40-60bps of gross margin impact. We’ll see to what extent HBI can keep that margin vs adjusting units per package to compete at retail.

Carter’s last week commented how tariff concerns have pressured manufacturing capacity in Asia, and it hurt its margins in 2Q. It is taking steps to reduce the impact next year and sees the potential for average unit costs to drop low single digits in 2020. HBI might see similar margin dynamics on the sourcing side even as somewhat more than half of COGS are made internally.