watch the replay below

https://cdn.jwplayer.com/players/a2Yg9Vwd-KY3o17gg.js

|

“Phase 1 was the alarm bells. Phase 2 is strap yourselves in. When we head into Phase 3 things start to get ugly.” |

This is an absolute must-watch.

We just hosted a conversation between Macro guru and Real Vision co-founder Raoul Pal and Hedgeye CEO Keith McCullough.

When two sharp Macro minds are in agreement, like Keith and Raoul are right now, it’s worth closer analysis. Here’s an important quote from Raoul that nicely sums up their hour-long conversation:

“We're now in the longest cycle in all recorded U.S. history. So it's already very long in the tooth. The structure of the cycle looks negative.”

Below we’ve transcribed essential takeaways from this conversation between Raoul and Keith.

* * * *

Keith McCullough: Hi, I'm Keith McCullough and welcome back to another Real Conversation with my friend Raoul Pal. He's the visionary and fearless leader of Real Vision. He’s probably one of the best people to talk to today, thinking clearly about what is happening in the market. I think a lot of people have been surprised by the abrupt move across asset classes, bond yields in particular. So, we timed this conversation well. Did we not Raoul?

Raoul Pal: Exactly. We knew the markets were going to set up like this perfectly for a conversation.

McCullough: You've absolutely nailed a massive call in euro dollars. But you've not been shy in talking about recessionary risks and I just want to lay that out there first and just give you the opening volley.

Pal: First of all, like you, I don't deal in certainties, I deal in probabilities. I use a business cycle framework as my format for analysis and understanding where we are in the world. And if I look at the business cycle and I can use, let's say the ISM as an easy way of looking at it. I looked at a bunch of forward-looking indicators too. That could be Semiconductor sales or it may be global trade or it may be exports.

Many of those indicators are starting to flash signals to suggest if we continue on this trend, then we're going into recession. We could be there maybe end of this year, maybe beginning of next year. So I'm starting to really focus on this whole process and obviously the bond market's telling us something very similar as well. So I always pay attention to the bond market.

McCullough: I mean, we already have a recession in corporate profits, depending on what sector you’re looking at. We have a recession in Tech. Tech earnings are actually negative year-over-year for the second quarter in a row. Tech doesn't look as bad as Energy and Materials yet, but those are recessionary numbers.

Pal: This is a function of the business cycle getting weaker. But what gets interesting to me is once these corporate profits start falling, corporate cash flow start falling, then the probability of buybacks start falling as well. So the markets themselves become more volatile.

People in the interest rate world keep saying, ‘Well isn't it all priced in?’ My answer is no rates are going to zero or lower.

I think people struggle with multi-asset class analysis. People have been so focused on equities. Bond futures are an incredible source of profits. Stan Druckenmiller came on Real Vision and said, the dirty truth is he makes a lot of his money in the 18 months going into recession and he makes it all out of euro dollar futures because you know, that's where massive leverage but with low volatility comes from.

McCullough: You’re seeing massive returns this week in euro dollars. No wonder you’ve got a nice smile on your face. What is it that people don't quite get about this stage of the cycle?

Pal: I think structurally it's a big shift for people to get their head around interest rates not rising. So that's why when everybody was betting on the rates going to 4%-5%-6%, all that nonsense that went on, I kind of knew and you knew as well, that the actual fast rate of change was when that view was wrong because the market wasn’t entirely set up for it. So even when we look at positioning in bond markets right now, they still haven't priced that in.

McCullough: Yeah, that's a super important point. If you show CFTC futures and options positioning, in October there was a max net short position on 2-year, 5-year, 10-year Treasurys, pick your vintage. People says, ‘But that’s come in.’ Well no. It's still a massive net short position on a nominal basis. And for whatever reason that just has not gone away. Do you have any thoughts on that?

Pal: I don't understand why it's not gone away. In the euro dollar markets, people were short 4 million contracts. It was the largest position in the history of euro dollars when I started going the other way. So I just think we've got a huge move still to come. And I understand that the pension system is still dramatically underweight fixed income and as are almost all portfolios.

McCullough: Just like you said, you need to look at the rate of change data in the business cycle – and the rate of change in positioning.

Pal: I mean that's key. The rate of change is everything in macro because everything happens at the margin. We're always looking for those shifts of the rate of change because once it actually shows up in price, it's too late.

McCullough: That’s one thing that obviously annoys me because I don't start with valuation. But we have a bunch of people that are playing catch up to this rate-of-change view. U.S. growth is slowing but there are a lot of investors that have these magical, optimal P/E models. These people now tell me growth slowing is priced-in and the ISM can’t go lower. What do you say?

Pal: We're now in the longest cycle in all recorded U.S. history. So it's already very long in the tooth. The structure of the cycle looks negative. Now people say, ‘Yeah, but so did it in 2015 and so did it in 2012.’ So let's deal with those two examples. In 2012, US GDP growth hit zero and Europe almost fell apart. So we came to a point of extraordinary stress and had a bear market around the world. We thought the entire European banking system, and in fact Europe itself was going to go away. So that's a pretty valid reason there was a massive Quantitative Easing and everybody was stimulating. Everybody was trying to avoid bankruptcy of the entire world's financial system. Okay, they saved it. Great.

The next one was 2015 when the dollar exploded higher and the whole world went into slowdown, as oil prices collapsed, commodity prices collapsed and global dollar flows shrunk. So that was a situation that was a global issue. It spread to U.S. manufacturing and the Chinese ended up stimulating just in time to save the day.

Now we have a situation where tariffs are imposing a slowdown in global trade. All of the global trade supply linkages are breaking and corporations are paralyzed in what they can do in terms of rebuilding trade linkages.

So corporate expenditure collapses in that environment. We're seeing global trade falling and then we've got the dollar, which you can't keep it down. If that goes higher, we start to shift all the balance of probabilities in for lower ISM.

McCullough: So to wrap it, you don't think that – even though we've seen weakening since Q1 of 2018 in China, Emerging Markets, Europe, etc – they can comp easier comps just because they're a little bit easier.

Pal: Yes. We've just got marginal recessions everywhere, in all of those regions.

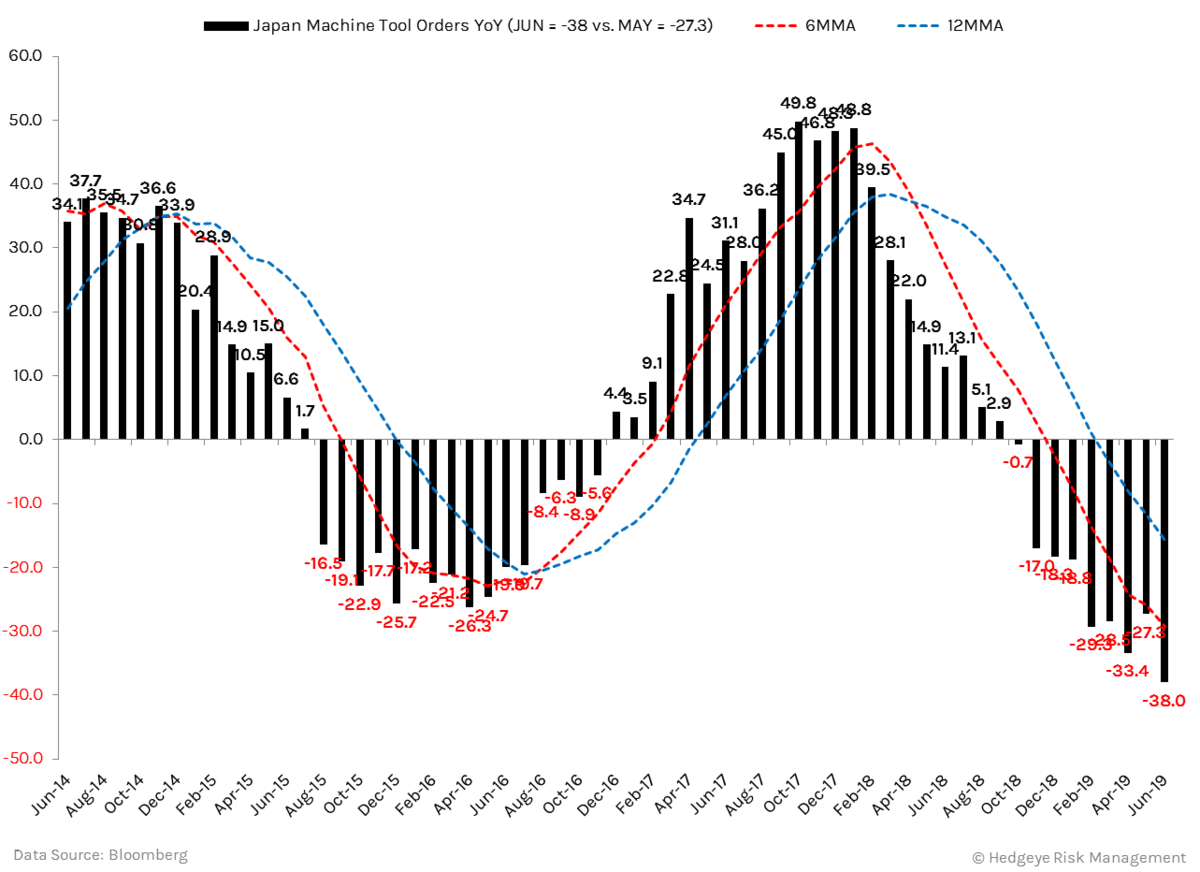

McCullough: That makes sense. You take any Asian export data and they are some of the worst numbers I’ve ever seen. I've never seen down negative -38% year over year for Japanese Machine Tool Orders. Now this data is starting to find its way into the main line of consumption. French Consumer spending went negative -0.6% year over year this week. German retail sales negative. Companies exposed to the European consumer are probably getting a little alarmed. I can't find a green shoot. I just can't, there's zero.

So what does the Fed do with that?

Pal: You and I know Fed cuts are usually terrible because they're going on when the economy is weakening. They are never bullish for equities. The first cut is because everybody gets excited. But after a while you very quickly realize that when the Fed are cutting rates, the stock market is falling and the economy is slowing. People's mindsets are really screwy about this.

McCullough: Well the Old Wall does a pretty good job saying it's different this time. I mean that's what their research departments have said, ‘Hey, as long as you don't have a recession, it's okay.’ That’s just not true. I mean you don't have to have a recession to lose 30-40-50% of your money. We didn't have a recession in the U.S. in 2016 but the average decline for a stock in the Russell 3000 was -38% from the 2015 high to its trough in 2016. What happened was you had a profit recession in certain parts of the economy.

Pal: Exactly. What we're trying to say is growth is slowing down. This is how you can take advantage of it or how you can protect yourself. And right now I believe bond yields are going much lower.