Below are analyst updates on our thirteen current high-conviction long and short ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

EXP

Click here to read our analyst's original report.

Eagle Materials (EXP) is in play here with activist Sachem Head now involved pursuing a break-up strategy to unlock value. We expect others to join in to Sachem Head’s reasonable efforts to improve value creation. Management felt embattled on both the money-losing proppant business & market valuation.

As we outlined in our original long thesis not only are EXP shares cheap relative to peers, transactions, and likely cash flows, but the company is exposed to several potential upside scenarios. We have discussed a number of options for the company including: an accretive sale to a competitor, substantial buyback, or restructuring by shuttering/selling proppant business.

Wallboard capacity utilization is likely much tighter than it looks on nameplate capacity, while cement imports are likely to be needed to match demand growth. Infrastructure may hit investor screens again as the political season renews, a rare topic on which there is some bipartisan agreement. Critically, we will look at the potential for “self-help” at EXP, including some value creation opportunities within the negative net income Proppants business.

The break-up could easily be worth north of $120/share, as we see it.

GIL

Click here to read our analyst's original report.

Last year Gildan (GIL) opened its latest factory named Rio Nance 6 in its manufacturing hub in Honduras. At full utilization the factory represents 30% revenue growth. Rio Nance 6 will give Gildan the capacity to manufacture various fashion basics products using different blends of cotton and polyester while also enabling shorter production runs (which allows for more product diversification without impacting margins).

Fashion basics have several different characteristics than a traditional cotton t-shirt as seen in the slide below. The more fitting cut and better feel of the fabric has driven a shift away from the older style cotton t-shirts.

The most important demand driver for Rio Nance 6’s new capacity is the growth of fashion basics t-shirts. What is especially appealing about the growth of the new category is the significantly higher price points with small added costs leading to much higher margins for Gildan. We estimate the market size of fashion basics to be ~$1.5bn and growing at a mid-teens rate. Gildan now has five different brands to meet different customers’ needs within the segment and the manufacturing capacity to supply it.

ANTM | UNH

Click here to read our analyst's original UNH report.

Earlier this week the White House told reporters they were withdrawing the rebate rule for Medicare Part D. The rule change was a major headwind for the MCOs land its withdrawal is good news, especially for those that have an in-house PBM, for now. For pharma, the shift in policy is very, very bad news.

The advantage Anthem (ANTM) has in developing a PBM in a new era is probably more valuable than ever. Recently, we had highlighted a significant delay or withdrawal of the rule as a risk to the UnitedHealth Group (UNH) short because it was so hotly debated at the White House. More to come.

TSLA

Click here to read our analyst's original report.

Was there something fishy about Tesla's (TSLA) 2Q delivery report? The unusually curt release that left significant ambiguity in the definitions, perhaps suggesting that additional detail would have detracted from the ‘upside surprise’. We’ll need the earnings release & 10-Q, as regional sales, ASPs, and definitions would help show the underlying trends. We were too low in our estimates and need to understand the error to improve. Still, some of the data and anecdotes we do see raise questions about pricing and quarter-end management.

Used Pricing On Tesla Site: We monitor the pricing of Tesla’s used vehicles listed for sale on its site. It has been boring for years – but not over the last few weeks. This occurs across most of the Models and MYs we track. Note that the price drops occur on the day of the Annual Shareholders Meeting, as Musk says, “So it's hard to be profitable with that level of growth… but I think we can be cash flow positive despite having a very high growth rate.” (Musk 6/11/19)

ROL

Click here to read our analyst's original report.

Rollins (ROL) margin gains have stalled amid increasing competitive intensity in a mature, slow growing market. Attractive markets for growth and acquisitions – those where route density offers cost advantages – present less runway and higher transaction prices. Acquisition spending targets customer contracts, with acquisition spending likely best viewed as an alternative to advertising or other expensed means of growing the customer pool.

With GDP-type organic growth rates, housing headwinds, competitive entry, and a feuding family with a controlling stake, one would reasonably expect ROL to trade at a discount to the market. We expect a growth deceleration, consolidation of leases, a host of yellow/red flags, and broader coverage to generate significant downside, as the S&P 500 addition premium fades from the share price.

DVA

Click here to read our analyst's original report.

The Fifth Circuit panel of judges met today to hear oral arguments on Texas v. USA on appeal of a decision by lower court that the Affordable Care Act was unconstitutional. We expect a decision in late 2019 that will affirm in part the lower court’s decisions that the individual mandate is unconstitutional, and the parties have standing and reverse in part the lower court’s decision that the entire law should be voided. Given that outcome the case is likely to be remanded to the lower court to work out what parts of the law should be severed, and which ones should stay. But first the Supreme Court is likely to have its say.

If the Fifth Circuit declares the individual mandate unconstitutional and sends the case back to the district court to determine what parts of the ACA can be severed and which parts would remain, provisions likely to join the unconstitutional club are section of the ACA known as Title I. This section includes sections on:

- Health insurance market reforms such as community rating, age bands, guaranteed issue, etc.

- Requirements of Qualified Health Plans sold on the ACA exchanges

- Standards for Essential Health Benefits including certain requirements for preventive services

- Permanent reinsurance program individual and small group market

- Employer mandate and penalty

- Individual mandate and penalty

- Cost-sharing reductions, premium tax credits to support individual and small group markets

Eliminating Title I from the ACA is a significant headwind for DaVita (DVA) which depends on commercial reimbursement for its margin.

HQY

HRAs offer employers an opportunity to shift from a traditional defined benefit health plan to a defined contribution plan similar to the way in which employers moved from traditional pensions to 401(k)s. The administration estimates that about 11 million employees will move from traditional employer plans to individual coverage HRAs as a result of the rule change.

As we pointed out in Best Ideas Short on HealthEquity (HQY), small businesses are disproportionate users of HDHP-HSAs relative to their larger peers. For that reason, some of the shift of enrollment from traditional employer-sponsored plans to HRAs is bound to take a bite out of HSA-eligible HDHP offerings, presenting HQY with yet another policy headwind, in addition to the planned repeal of the Cadillac Tax and waning interest in expanding the HSA program.

NFLX

Click here to read our analyst's original report.

Good article from WSJ this week (click here to read).

T recently announced that the name of their new streaming service will be HBO Max, and will take back the exclusive rights from Netflix to stream Friends beginning in 2020. In the last month, we received confirmation that Netflix will be losing its top two series (The Office and Friends). All consistent with our thesis from the March 2020 black book.

Netflix (NFLX) stock was up earlier this week in a red tape on “Stranger Things” bump (NFLX announced it broke viewership records with ~40M Households viewing and ~18M Households having finished all of season 3), but then paired gains following the T/Friends announcement. As a reminder, Stranger Things is one of a handful of blockbuster series that NFLX has, and the ONLY one where they own the rights to.

The fact patterns that matter and the data we are tracking support our short thesis, despite “hype” around Stranger Things (see two tracker notes attached). NFLX reports earnings on 7/17, and if we are right on the guide (or even directionally right), I think it is down stock on the print.

SBUX

As Starbucks (SBUX) will tell you, the potential for the coffee market in China is tremendous and they are creating a path for new competition in the market. It appears that Luckin did not happen by accident, and now celebrity CEO Qian Zhiya (Jenny) has been able to attract a tremendous amount of venture capital to support the company’s growth.

Make no mistake, the emergence of Luckin into the coffee market in China is a binary event for Starbucks. Luckin has a better than 50% chance of causing significant disruption in the China coffee market. The implication of this will be significant pressure on Starbucks China profitability and growth rate.

The Luckin business model goes right at the heart of the SBUX business model. Luckin intends to open thousands of smaller locations near the current SBUX locations, charging significantly less than what SBUX must charge to justify the third-place experience and the emotional connection.

What is that emotional connection worth to the Chinese consumers and why can’t Luckin build an emotional connection?

NSP

Click here to read our analyst's original report.

Shares of Insperity (NSP) are trading as though the PEO industry isn’t cyclical and increasingly mature. The cyclical elements extend beyond employment trends to costs, regulations, and marketing. The industry has enjoyed exceptional tailwinds in recent years, while limited Street coverage, arcane business metrics, and a move up in index membership have left the shares untethered to underlying business realities.

With steep comps, intensifying competition, slowing growth, and a lack of incremental tailwinds, investors will likely be just as surprised by the cyclical downside as they were by the post-GFC recovery. We see significant downside in the shares, with catalysts positioned through 2020.

MAR

Click here to read our analyst's original report.

Big picture, our Macro team is forecasting the economy to remain in Quad 3 / Quad 4 in 2H19, with the likelihood of oscillating between Quads 3 and 4 well into 1Q20. The hotel industry will suffer in this environment – particularly, C-Corps suffer in Quad 3 and 4, which relatively favor hotel REITS.

Our models flag continued RevPAR deceleration, which means the rising OpEx tide will unlikely be offset; even stable RevPAR growth will just not cut it. The industry is at record profit levels, but gross operating profit margin is in decline since 2015, and are largely negative on SSS basis, and the number of markets with negative growth is increasing.

RevPAR and margins are the core drivers of owner ROI and matter in a big way to future unit development, which bodes ill for growth in C-Corp / brand companies. Profits are slowing, margins falling, but the C-Corps stocks have hung in there as near term earnings are likely insulated. However, looking ahead, we see owner level pressures impacting C-Corp earnings as developers pare back their plans for unit growth.

Looking specifically at Marriott (MAR), this is basically a valuation compression call: MAR continues to see lower unit growth. Even just 1% difference will have huge impact on value. We are using lower numbers overall in the industry, and MAR should suffer the most from the overall downward trends.

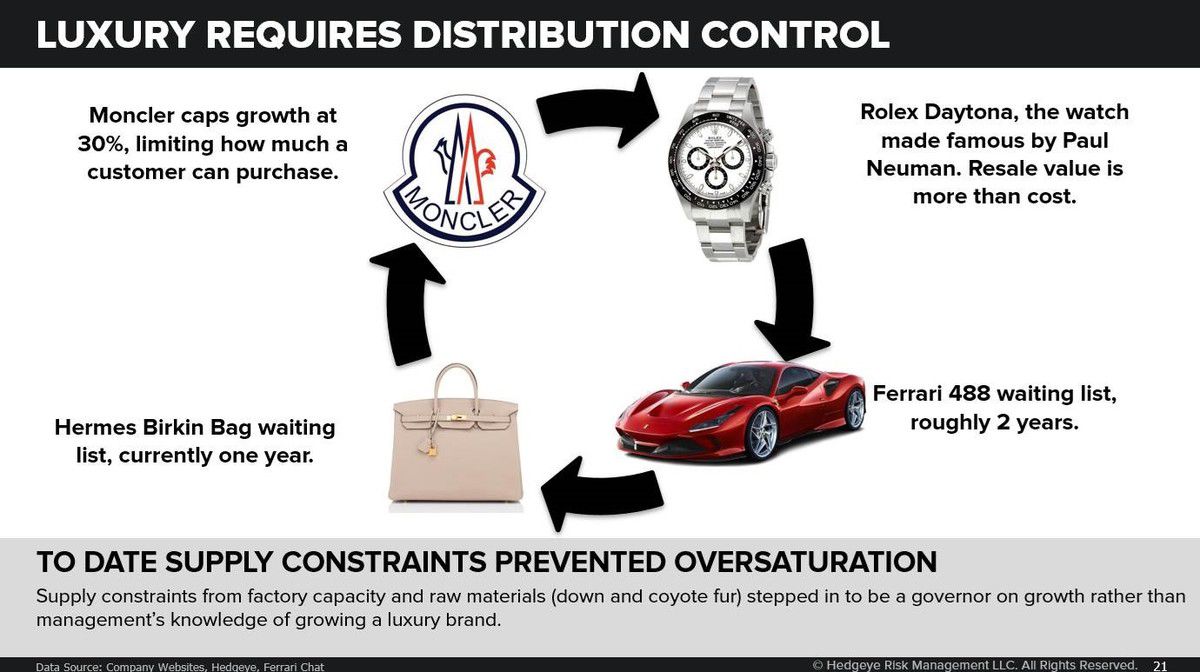

GOOS

Click here to read the short Canada Goose (GOOS) stock report Retail analyst Brian McGough sent Investing Ideas subscribers earlier this week.

Luxury brands have to control their distribution and growth or they will lose their exclusivity. Canada Goose’s demand has exceeded supply to date. In combination with Canada Goose’s high prices it has been confused as a luxury brand. The company’s supply growth has been limited by raw materials and labor to make the jackets, not by management’s awareness and experience with luxury brands. With the addition of new owned capacity in the past year supply appears to be overtaking demand. The deceleration in wholesale and direct to consumer growth in FQ4 are warning signs that the GOOS growth story has broken.