“The fiercest serpent may be overcome by a swarm of ants.”

-Isoruko Yamamoto

Last week, I flew 2,000 miles across Canada on a rare week-long vacation from Hedgeye to take a group of the top 10-year old ice hockey players in Connecticut, New Jersey and New York to play in the Brick Invitational in West Edmonton Mall. "The Brick" as it's commonly called, is hockey's equivalent of the Little League World Series. It's a big deal in the hockey world, featuring the top players in North America, many of whom eventually go on to play in the NHL.

Bottom line is we were extremely fortunate to go on an undefeated 8-0 run. The kids I helped coach beat (then undefeated) Team Alberta in the championship game to become the undisputed top Squirt hockey team in North America . . . the first American winner in 17 years.

The obvious question you may be asking yourself right now is what does youth hockey have to do with investing? Fair enough, At face value, perhaps not a lot. However, if you examine the underlying reasons why this team went on to win it all (which were process, preparation and teamwork) then perhaps quite a bit.

We developed a defensive system which ultimately stymied every team we played in the tournament. In our "top-secret" playbook, it is called The Swarm. Of course, the 3-month development towards the tournament was not without its shortcomings and soul searching. But as Andrew Carnegie famously said:

“Teamwork is the fuel that allows common people to attain uncommon results.”

Whether it be youth sports, our family lives, volunteering for a non-profit, whatever... the lessons we can learn to improve our business and investing careers are meaningful. Personally, if it took me a week in a mall in Edmonton with a bunch of 10-year old kids competing at the highest level to reinforce and build on some of my beliefs about process, preparation, and teamwork . . . then that is a vacation well spent!

But to the Global Macro Grind...

The global macro “news du jour” was Fed Chair Powell's semiannual testimony to Congress. A couple key tidbits from his testimony:

- “Economic momentum appears to have slowed in some major foreign economies... Moreover, a number of government policy issues have yet to be resolved, including trade developments, the federal debt ceiling, and Brexit. And there is a risk that weak inflation will be even more persistent than we currently anticipate."

- "The economy performed reasonably well over the first half of 2019, and the current expansion is now in its 11th year. However, inflation has been running below the Federal Open Market Committee's (FOMC) symmetric 2 percent objective, and crosscurrents, such as trade tensions and concerns about global growth, have been weighing on economic activity and the outlook."

- "Since our May meeting, however, these crosscurrents have reemerged, creating greater uncertainty.... These concerns may have contributed to the drop in business confidence in some recent surveys and may have started to show through to incoming data."

So, strangely enough, P.E. (Private Equity) Powell’s outlook is not dissimilar to ours – slowing global growth, incoming data in the U.S. decelerating, and inflation remaining benign. Now the question of course is: what does this mean for interest rate policy?

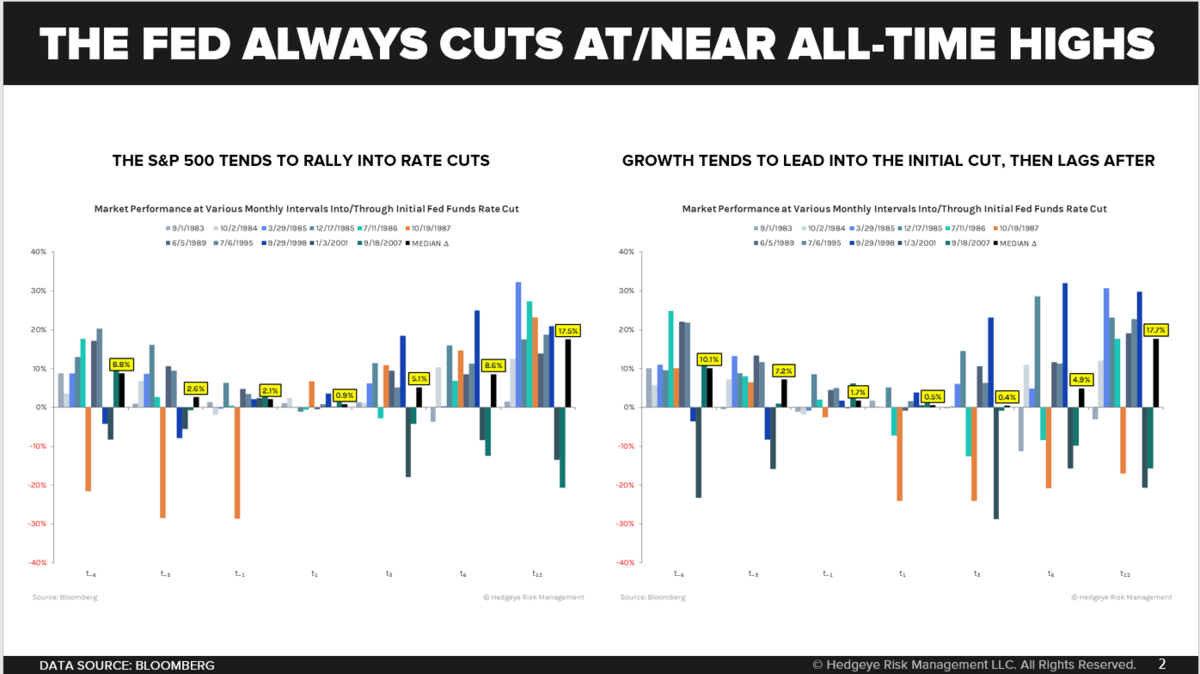

Consensus is largely baking in a 25-basis point cut in July. In fact, at last look the Fed Futures are pricing in a 69% likelihood of a 0.25% cut in July. A quick glance at major media outlets endorses this same consensus. One question we’ve been fielding from many investors recently relates to whether the Fed will cut when U.S. equity markets are at, or near, all-time highs.

As our ever data driven Senior Macro analyst Darius Dale highlighted during The Macro Show yesterday, the short answer is yes. This occurs frequently.

In fact, as the Chart of the Day below shows, this is almost always the case for initial interest rate cuts. So, to the extent you think the stock market will prevent P.E. Powell from cutting rates, it will not. Conversely, a market sell-off will almost certainly force his hand.

Additionally, in interest rate policy-land, the ECB released minutes from its June policy meeting. A couple key takeaways include:

- Broad agreement ECB needs to be ready and prepared to ease policy further as appropriate; and

- If low inflation continues to prevail, considerations of more strategic nature might be warranted.

In a nutshell, the world’s two largest central banks are prepared to bring the cowbell!

The downside of being aggressively (or potentially aggressively accommodative) is that a mispricing of assets can occur. As the most obvious case in point, let’s consider some sovereign bond yields around Europe:

- Italian three-year bonds sold at 0.49% and an auction for 50-year Italian was 5x oversubscribed;

- France 10-year bonds are trading at 0.01%;

- Portugal 10-year bonds are trading at 0.52%;

- Greece 10-year bonds are trading at 2.21%; and

- Spain 10-year bonds are trading at 0.43%.

Given that context, the U.S. 10-year Treasury continues to look rather juicy (and safe) at 2.06%. Portugese bonds with a national debt / GDP of 121.5 . . .not so much. It won’t be long until everyone is trotting out Reinhart and Rogoff’s seminal paper “Growth in at Time of Debt” . . . was the European sovereign debt crisis really that long ago?

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signals in brackets) are now:

UST 10yr Yield 1.94-2.10% (bearish)

SPX 2 (bullish)

RUT 1 (bearish)

Utilities (XLU) 58.99-61.56 (bullish)

REITS (VNQ) 86.09-91.76 (bullish)

Financials (XLF) 26.98-28.54 (bearish)

Shanghai Comp 2 (bearish)

Nikkei 21152-21951 (bearish)

DAX 120 (bullish)

VIX 12.00-16.87 (neutral)

USD 95.18-97.30 (neutral)

Oil (WTI) 55.74-60.81 (bearish)

Gold 1 (bullish)

Copper 2.64-2.74 (bearish)

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research