Editor's Note: Below is an excerpt transcribed from a recent edition of The Macro Show hosted by Senior Macro analyst Darius Dale with Director of Research Daryl Jones.

* * * *

Darius Dale (Senior Macro Analyst): Lastly, I want to talk about Housing (ITB). The ITB bucked the trend yesterday, and was down -0.6% versus +0.3% for REITs (VNQ) and +0.1% for Utilities (XLU). I thought this was really interesting. This article came out a couple days ago from Bloomberg saying that “Hedge Funds are having their best start to the year in a decade.”

Golf clap on that.

But the article failed to mentioned hedge funds had their worst December ever, and the worst fourth quarter ever, ex the financial crisis.

Basically everything bottomed at the end of December. If you were still sitting in a seat at the end of December, you were going to have a good quarter. We don’t want to mince words. We like it when our clients do well. But cherry-picking that bottom to me is quite dangerous. It sends a signal that all is fine with respect to global markets which we obviously think it’s not.

Since that December 24th low in the S&P 500, the market is up +26.7%. So you could’ve just bought the S&P 500 and crushed it. You’re not commanding a 2 and 20 fee structure being long the SPY. There are certainly cheaper vehicles to capture that type of return.

For us, it’s all about the types of asset allocation decisions you’re making at these pivotal moments.

You could have bought all the SPY you wanted if you had capital to put to work or you could’ve bought all the Housing you wanted and you’re beating the S&P by 700 basis points. ITB is up +34.3% from 12/24. Gold Miners (GDX), if you had the cojones to buy on its lows in September, it’s up +46.0% from 9/11.

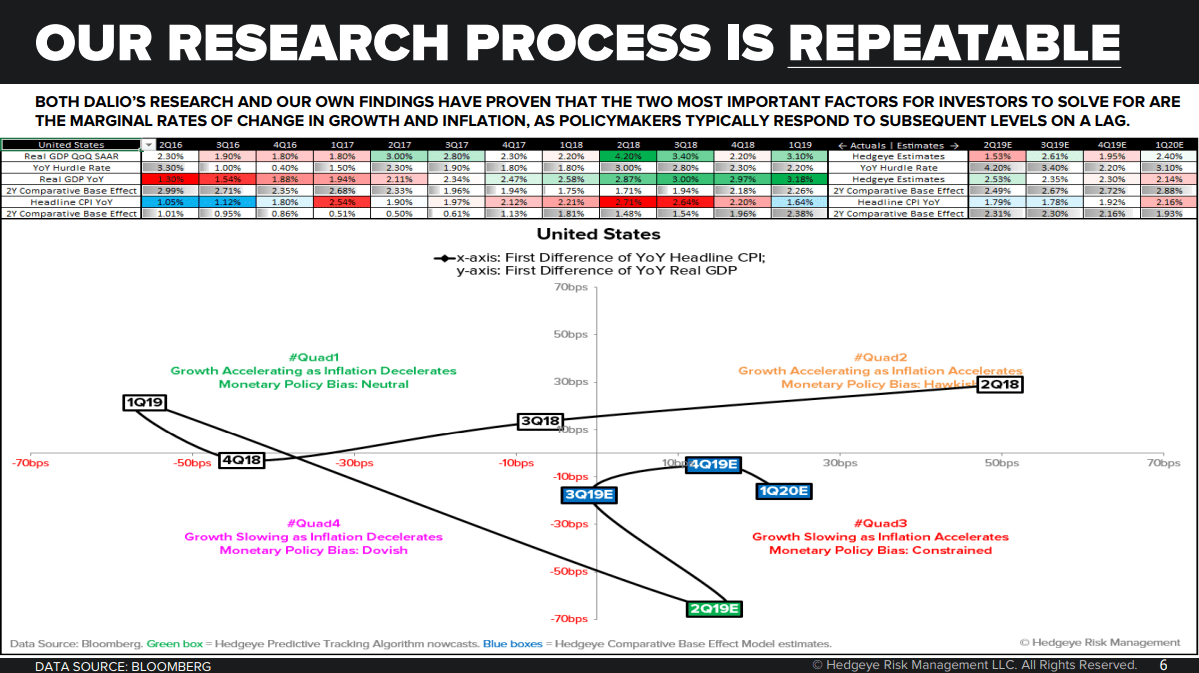

It’s not about charging 2 and 20 for S&P-type returns. We think we’re on to something with this full cycle investing thing. This stuff really matters. We think about these things as it relates to our GIP model. “G” stands for Growth. “I” stands for Inflation. “P” stands for Policy.

Dale: We look at the changes in growth and inflation to front-run and proactively predict central bank policy changes and their targeting of those two factors. In this chart on slide 27, we highlight profits as the third leg of the stool when it comes to talking about our negative thesis on the cycle.

If you go back to the end of 3Q 2018 when we put together our Macro themes deck, we were basically saying that all three of these factors, Growth, Inflation and Profits, had peaked in Q3 and were likely to trend lower over the next 12 months. But you don’t even have to get the Quad movements exactly right. If you just follow the change implied by the color scheme in this chart, we bottomed in 2016. We accelerated for nine consecutive quarters, 10 of the last 11 quarters if you look at it in real GDP terms.

If you look at Real Final Sales, which is the bolus of this chart, basically everything peaked in Q3, has been slowing since and is likely to continue slowing over the next three to six months. You go back and look at the returns since a lot of these things peaked, the Russell peaked on August 31st and is down -10.2% from there. If you look at when the “globally synchronized recovery” peaked in January of last year, Industrials (XLI) are down -4.9% from its January 26th peak in 2018. Basic Materials (XLB) peaked on January 26th as well and is down -10.6% from there.

Dale: The point here is that you can cherry-pick December 24th and say everyone was a cowboy and hero who bought the market with leverage on December 24th. But if you just respect the cycle, and understand that most people probably didn’t or couldn’t do that then look at what’s leading the market higher, it’s low beta/minimum volatility stocks.

If you look at the S&P 500 Low Volatility ETF (SPLV) as a proxy for low beta/minimum vol factor exposures, it’s making new highs. One of the things that’s been perpetuating the broader market highs is the return of sectors like Consumer Staples (XLP), Healthcare (XLV), Utilities (XLU) and REITs (VNQ) continuing to break out.

Tech continues to be a holdout as it relates to our Quad 4 theme, but we think it will give up the ghost as we get into the thralls of earnings season and companies begin to acknowledge some of the downside other companies have already signaled. I’m thinking about Broadcom (AVGO) and BASF (BASFY) earlier this week.

As it relates to bond yields, basically everything peaked in Q4 as it relates to full cycle investing. Both the 2-year and 10-year peaked on 11/8. The 2-year is down 104 basis points. The 10-year is down 114 basis points. The real 10-year is down 80 basis points. Basically two-thirds of the decline in rates has come from real rates declining which obviously means that growth has been a bigger driver of the decline in interest rates. It tells you everything you need to know on a trending perspective that everything is slowing.

Daryl Jones: Subscriber question here. Has the Fed ever cut rates with markets at all-time highs?

Dale: Yea almost always. Go to slide 125.

This is a really interesting table because I effectively got sick of people talking about Fed rate cuts with no historical context. So what we’re showing here is Fed Funds rate cutting cycles going back to 1982. If you recall, I don’t specifically recall because I wasn’t born yet – but the Fed effectively started targeting the Fed Funds rate as its main policy tool as opposed to the quantity of money.

So from there you can look at 11 rate cutting cycles since then. And what you see is that markets tend to be up a lot into these rate cutting cycles. My expectation is that the market is at or near all-time highs for the vast majority of these. If you go back through the table the median return of the S&P 500 is up 5.8% three months out from the initial cut but it’s lead by low beta/minimum volatility exposures that I’ve already hit on. When we’re in Quad 3 or Quad 4 you want to be long low beta minimum volatility exposures as opposed to cyclical or high leverage.

High beta is still down -6% from where it peaked in January last year. So these are the kind of things that we continue to callout. The cycle really does matter. If you look at the table, low beta/minimum vol is up 8.5% three months out from the first cut. That compares to basically flat for the Russell 3000 Growth. You see that same type of defensive posture in the long bond as well, which is up 5.3% 3 months out from the initial cut. That compares to 3.8% for Investment Grade Credit and 2.8% for High Yield Credit.

So as long as we’re careening down the backside of the cycle you get paid to be long financial assets because the Fed is cutting interest rates but it’s what type of financial assets are you long? Are you long Housing and Gold Miners or Financials (XLF)? Are you long Treasury Bonds or High Yield Credit and Leveraged Loans? Those are the types of questions we spend countless hours trying to answer. Just telling someone to buy stocks because the Fed is going to cut interest rates is meaningless.

Powell is testifying before Congress today and he’s going to reiterate what he already did in June, that the Fed is ready and willing to cut interest rates. Now whether they do 50 basis points at their upcoming meeting remains to be seen but according to our models they don’t have the river card yet (i.e. bad enough economic data) to cut.

But certainly by the time Jackson Hole rolls around they will have the River card to cut interest rates. They will continue that progression in interest rate cuts because we’re continuing to careen down the backside of the cycle of growth, inflation and profits. We think an earnings recession is beginning to materialize here in Q2.