Below are analyst updates on our thirteen current high-conviction long and short ideas. Please note that we removed Williams-Sonoma (WSM) and Penn National Gaming (PENN) from the short side of Investing Ideas this week. We also added Anthem (ANTM) to the long side and Canada Goose (GOOS) to the short side. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

EXP

Click here to read our analyst's original report.

Below are some notes from our Materials team on why we like Eagle Materials (EXP) on the long side:

- Construction is the largest cyclically depressed industry in our coverage. Construction recovery is set to resume.

- Activity remain bigly depressed and tightening utilization should allow for robust pricing as demand resumes

- Growth in the proppant business is a toehold for activist/shareholder engagement. Shares don't reflect strategic transaction value.

We continue to see EXP as one of the best longs in Materials (or Industrials for that matter).

Critically, activist Sachem Head is now involved and pursuing a break-up strategy to unlock value that we previously identified. We expect others to join in to Sachem Head’s reasonable efforts to improve value creation. Management felt embattled on both the money-losing proppant business and market valuation. The break-up value could easily be worth north of $120/share, as we see it.

GIL

Click here to read our analyst's original report.

The growing penetration of private label apparel in the US mass channel represents an attractive growth opportunity for Gildan Activewear (GIL) as the world leader in low cost basic apparel manufacturing.

The transition from selling its own brand inside Wal-Mart to supplying the George brand should have several benefits for Gildan.

Walmart now has a private label “horse” in the basic apparel department that it should support. By having a strong private label program Walmart avoids the price pressure of matching online competitors. Gildan also manufactures many more products than just the men’s underwear shirts, boxer briefs, and briefs it is currently supplying. As a private label supplier in good standing with Walmart, Gildan is positioned to win many further programs in several other apparel categories.

So the George brand represents space gains, improved placement, unit velocity opportunity, and the optionality of further program wins at WMT. And, contrary to the concerns of many the change should be neutral to margins for Gildan.

Management’s announcement new manufacturing hub in Bangladesh is in part due to the growth prospects for private label. The launch of the Gildan made George men’s underwear program is just the start.

GIL is setup for a highly accretive multiyear acceleration in revenue growth that will drive significant earnings upside vs street expectations.

ANTM

Below is a brief note written by CEO Keith McCullough on why we added Anthem (ANTM) to the long side of Investing Ideas earlier this week:

|

With Healthcare being a long in Quad 4, and one of our Best Ideas (Institutional Research product) on sale today (ANTM -2%), it's a good time to review why Healthcare analyst Tom Tobin went bullish on Anthem back in May. This is what he wrote: OVERVIEW The volatility of the last several weeks surrounding #M4A and a host of other bipartisan attacks on the Health Care Industry have opened up an opportunity to get long the other side of our rebate trade and short in UNH. Anthem has long suffered at the hands of the large PBMs, whether it was their partner (supposedly) ESRX, or a competitor like UNH. Aggregating drug spending and extracting rebates was a never a core competency that ANTM developed, until now. With changes in policy that governs rebates coming in 2020, Anthem should finally be on a level playing field. Our view is less rebates for others will lead to greater market premium parity and incremental enrollment share gain for ANTM. Looking back, ANTM enrollment has tread water while UNH accelerated. In our view, ANTM is starting IngenioRx, their new in house PBM, at exactly the right time. Assuming premium differences narrow and ANTM can take Medicare Advantage +/- PDP enrollment, every point of share is worth ~$1.00 to ANTM EPS. Buy when they're for sale. Don’t chase, |

TSLA

Click here to read our analyst's original report.

Tesla (TSLA) demand data is reflecting a collapse in demand asynchronous with Musk’s lofty expectations. We see continued risk in 2H19 with incremental subsidy cuts, eroding used car pricing, and a cash constrained company that needs to invest to launch new platforms with increasing competition suggesting a gradual death by dilution.

Below are some key highlights from our Industrials team regarding our Tesla short thesis:

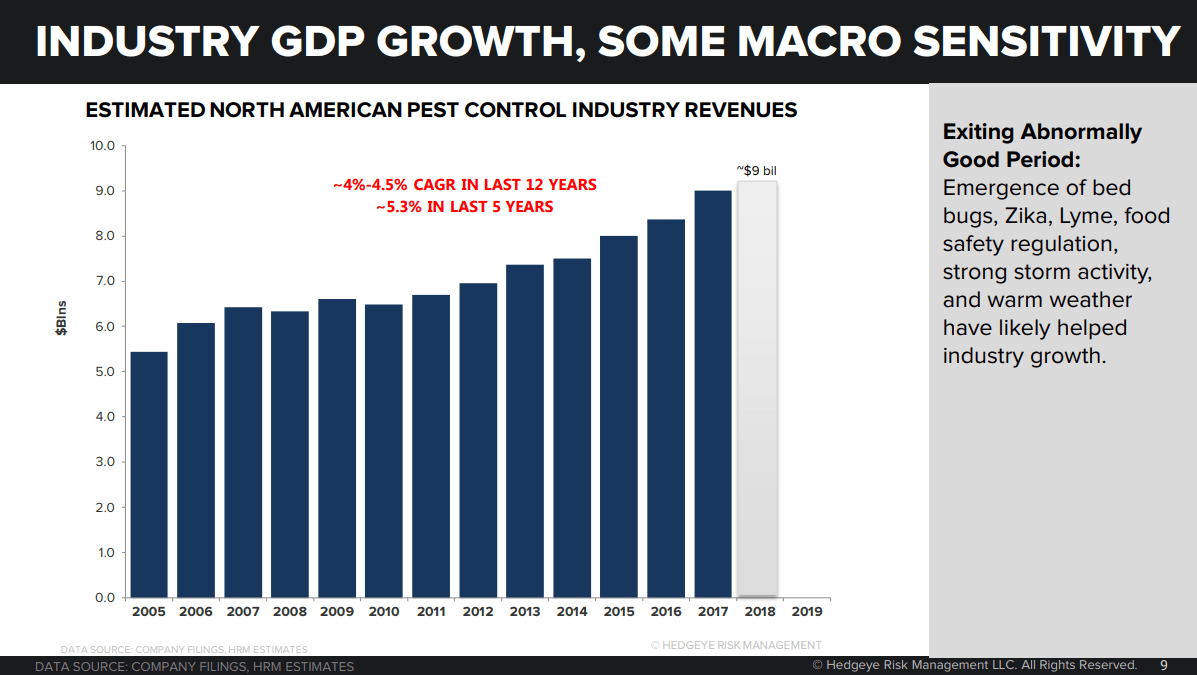

ROL

Click here to read our analyst's original report.

Our Rollins (ROL) work continues to show signs that the tailwinds behind the pest control industry are fading. Pricing trends in the industry suggests rates have been stretched and may now be facing competitive pressures based on our work. Customer counts have stalled, while revenue per customer has ramped significantly over the past five years following ROL’s pricing study.

With GDP-type organic growth rates, housing headwinds, competitive entry, and a feuding family with a controlling stake, one would reasonably expect ROL to trade at a discount to the market. We expect a growth deceleration, consolidation of leases, a host of yellow/red flags, and broader coverage to generate >50% downside, as the S&P 500 addition premium fades from the share price.

DVA

Click here to read our analyst's original report.

An important event on our DaVita (DVA) short thesis is the movement of AB 290 through the California Legislature and the Third Party Payment rule under consideration at the White House.

Having cleared the California Assembly and been referred to the Senate, AB290 is set for Senate Committee hearing on July 3rd, following more or less the same path to approval as last year’s identical but vetoed legislation. This bill, if enacted singles out Large Dialysis Organizations for Medicare level reimbursement when a third party, like the American Kidney Fund, pays commercial insurance premiums for ESRD patients. Depending in the federal response, the California solution may spread to other states.

There is also an ongoing lawsuit in Florida where Florida Blue has accused DVA of similar practices highlighted in California, among other things. With the ~10% of patients who are commercially insured accounting for 110-115% of DVA’s profit, the increased regulation and prohibition of third party payments will be a much bigger deal to DVA than the baked in sale of DMG.

UNH

Click here to read our analyst's original report.

Earlier than expected, the CMS sent to the White House for review and approval the final rule that would require manufacturer rebates to be shared with Medicare beneficiaries at the point of sale. We expect the rule to delay implementation until mid-2020 instead of the proposed Jan. 1, 2020. UnitedHealth Group (UNH) has aggressively used rebates to manage medical cost trend and keep Medicare Advantage plan premiums consistently low. ANTM on the other hand has not had the benefit of rebates and ceded market share in Medicare Advantage. The playing field will level under the new set of rules.

HQY

Sooner than expected, the Trump administration released its final rule expanding the use of Health Reimbursement Accounts to permit integration with individual health insurance. The proposal, which really just represents a return to guidance in place prior to 2015, presents employers with an alternative to the HDHP-HSA combination that has fueled HealthEquity's (HQY) growth since passage of the ACA.

As we pointed out in Best Ideas Short on HQY, small businesses are disproportionate users of HDHP-HSAs relative to their larger peers. For that reason, some of the shift of enrollment from traditional employer-sponsored plans to HRAs is bound to take a bite out of HSA-eligible HDHP offerings, presenting HQY with yet another policy headwind, in addition to the planned repeal of the Cadillac Tax and waning interest in expanding the HSA program.

NFLX

Click here to read our analyst's original report.

We see risk to 2H19 consensus subscriber estimates as the growth rate of Netflix (NFLX) mobile app downloads worldwide has slowed materially in recent months. The slowdown is occurring as the company works through a series of price increases in the U.S., Latin America and Europe. We believe NFLX mobile app downloads are a good proxy for gross subscriber additions based on the high absolute correlation to NFLX's reported metrics. The deceleration in growth is consistent with our view that price increases will slow the rate of adoption, especially in developed markets where NFLX is > 50% penetrated.

SBUX

Luckin (LK) is looking to raise up to roughly $560M with a price per share in the range of $15 to $17, at a roughly $4B valuation. The company has been given a license to lose money in an effort to gain market share – Starbucks (SBUX) is a big loser with this dynamic. Luckin’s coffee costs on average 25% less than the equivalent SBUX cup. Whether this strategy is sustainable or not, it will last for at least a couple more years, and during that time SBUX will have to compete against someone that doesn’t care about losing money.

SBUX has invested billions of dollars in growing the coffee culture in China, now start-up companies such as Luckin have a paved path in which to jump on the coffee train and undercut Starbucks on price. Luckin, with lower prices, more appealing occasion and local branding, has likely already and will continue to impact Starbucks business in China.

NSP

Click here to read our analyst's original report.

Insperity (NSP) is a highly cyclical company. Shares of Insperity are trading as though the PEO (i.e. Professional Employer Organization – providing comprehensive HR solutions for small and mid-size businesses) industry isn’t cyclical and increasingly mature. The cyclical elements extend beyond employment trends to costs, regulations, and marketing. Unit metrics track broader employment trends. A tight labor market pulls workers off the sidelines, while driving the need for better benefits.

The Hedgeye Macro team sees U.S. GDP growth slowing over the next three quarters, not an environment beneficial to NSP. The team's dynamically re-weighting 30-factor predictive tracking algorithm for US GDP growth is at 2.53% YoY/1.53% QoQ SAAR for 2Q 2019. The latter figure compares to 1.80% for Bloomberg Consensus and 2.05% for the Atlanta Fed’s GDPNowcast.

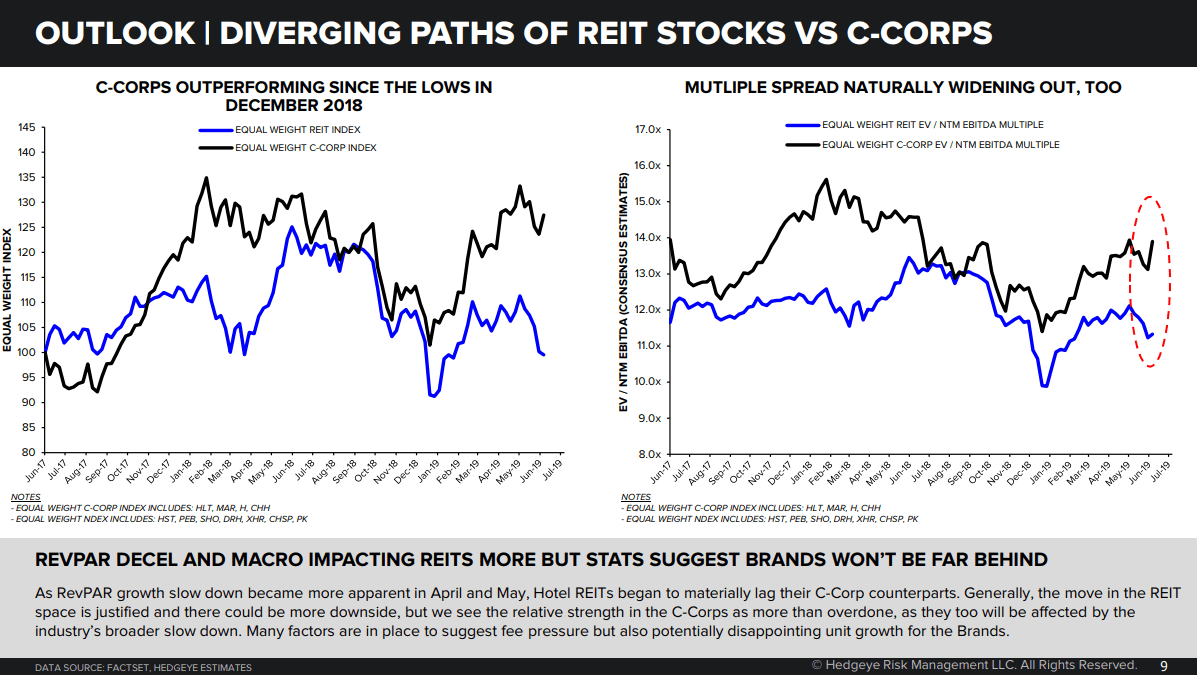

MAR

Click here to read our analyst's original report.

The hotel industry, and investors therein, once again find themselves at a critical juncture. At the same time the RevPAR cycle shows signs of old age, owners are battling the onslaught of higher construction and operating costs and consequently slower, or even declining profits.

As the RevPAR growth slow down became more apparent in April and May, Hotel REITs began to materially lag their C-Corp counterparts. Generally, the move in the REIT space is justified and there could be more downside, but we see the relative strength in the C-Corps as more than overdone, as they too will be affected by the industry’s broader slow down. Many factors are in place to suggest fee pressure but also potentially disappointing unit growth for the Brands.

The Brand companies, such as Marriott (MAR), are not immune and not just because of the direct RevPAR effect on fee growth.

GOOS

Below is a brief note written by CEO Keith McCullough on why we added Canada Goose (GOOS) to the short side of Investing Ideas this week:

|

Another way to think about month-end markups (especially in less liquid, smaller cap names) is that you get to pick them off on the short side at lower-highs before the next decline. One of Brian McGough's best new ideas (on the short side) has been Canada Goose (GOOS). Here's what he wrote (to our Institutional Subscribers) at the beginning of June: “We added GOOS to our Best Idea Short list 2 weeks ago calling for 50%+ downside in the stock. While I’ll definitely take the selloff since last week's print, let’s not forget that there’s still at least another 30%+ downside left in this stock. This stock is stuck in growth purgatory – and broken growth stocks don’t work in Macro Quad 4 (actually, they don’t work in any Quad). There is a fundamental disconnect between $4.1bn in equity value and the trajectory of the profitability of the core business, and the inherent risk to growing outside of its coat business. We’re probably going to see some obligatory downgrades on this name tomorrow morning – but ultimately I think the bulls will come out and defend it. They will defend guidance as a conservative starting place and that this is Moncler 2.0 (which it's absolutely not). They likely don't share my view that there’s there’s 1,000bps downside in risk to margins embedded in this model as it transitions away from its core jacket into innerwear/knitwear – something that wholesalers (and ultimately consumers) largely don’t want from Canada Goose. As part of our diligence for our presentation, my team had a call with a private outwear buyer in Canada yesterday noting that wholesalers -- and presumably consumers -- have little appetite for anything other than its core coat offering, and that might even be getting thin – especially as stores open adjacent to the best wholesale doors. We’re presenting our Black Book on GOOS tomorrow, June 5th at 12:30 to outline the bear case from here, which I still think is powerful.” Short the bounce, |