Position: Long Germany (EWG)

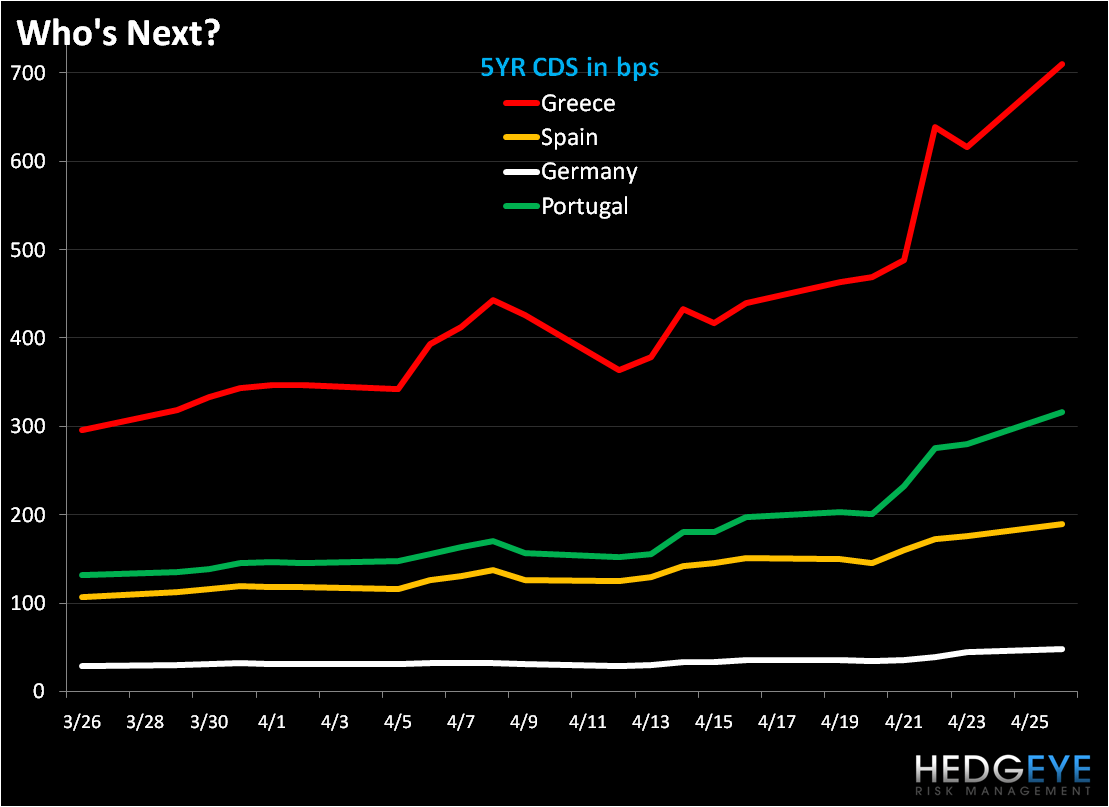

While Goldman claims the spotlight today, European sovereign debt concerns remain at large; in fact risk has heightened for the PIIGS in recent days (particularly Greece) despite a European and IMF guaranteed loan of €45 billion to fund Greece’s debt. We’re seeing confirmation of our 2Q10 theme of Sovereign Debt Dichotomy via rising CDS spreads, higher yield spreads, and weakness in equity markets from the PIIGS (see charts below). What is Germany’s role in this risk equation?

In the near term, the PIIGS continue to shake as conservative German Chancellor Angela Merkel reiterates her position that Greece must do more, i.e. increasing austerity measures, before funds are certain. [Note that Germany is on hook to contribute some €8.4 Billion Euros to Greece, the largest contribution of all Euro member states].

While we believe Germany’s “contribution” is inevitable, what we’re currently seeing from Merkel is political posturing. On May 9th, Germany’s largest state by population and the industrial heartland, North Rhine-Westphalia (NRW), holds a state election. Merkel’s Christian Democratic Party (CDU) along with her coalition partners the Free Democrats (FDP) need a win to retain the majority in the Bundesrat (upper house of parliament), which is critical for her party to carry out scheduled reforms, including tax cuts and health care reform.

Recent polls suggest that Merkel’s opposition, the alliance of the Social Democrats-Greens, has a slight advantage. With government spending a hot topic in the election, Merkel must show that she’s not writing a blank check to the Greeks, and will continue to drive a hard line.

In the longer term, we believe that the deeper debt-laden countries, globally, will underperform more fiscally conservative countries, like Germany. Please see our post titled “Q2 2010 Themes: Sovereign Debt Dichotomy” on our portal that lays out one play: long Germany, short Spain. Currently, the DAX is outperforming Spain’s IBEX 35 by a spread of 1,560 bps YTD. It may not be long before we see equity and credit charts from the likes of Spain or Portugal that resemble Greece. That said, we also believe the selloff in Greek equities and bonds is overdone given Germany’s ability to support Greece when it is politically expedient. Stay tuned.

Matthew Hedrick

Analyst