At long last the Federal Trade Commission cleared the sale of Davita Medical Group to UNH with some conditions. Those conditions include divesting the HealthCare Partners of Nevada unit in a sale to Intermountain Healthcare. Meanwhile, Intermountain will be required to sell its minority stake in P3 Partners, a Las Vegas area service provider. The divestiture will be handled post close by UNH and the deal price is not reduced.

Since our short thesis has presumed eventual close of the DMG sale, a more important event is the movement of AB 290 through the California Legislature and the Third Party Payment rule under consideration at the White House.

Having cleared the California Assembly and been referred to the Senate, AB290 is set for Senate Committee hearing on July 3rd, following more or less the same path to approval as last year’s identical but vetoed legislation. This bill, if enacted single,s out Large Dialysis Organizations for Medicare level reimbursement when a third party, like the American Kidney Fund, pays commercial insurance premiums for ESRD patients.

Similarly, the White House is reviewing a rule that would regulate third party payments at the federal level. While we do not expect CMS to take as bold a step as the California legislature, they are likely to require more disclosure and reporting that discourages migration to commercial payers by dialysis patients that are otherwise eligible for Medicare. Depending in the federal response, the California solution may spread to other states.

There is also an ongoing lawsuit in Florida where Florida Blue has accused DVA of similar practices highlighted in California, among other things.

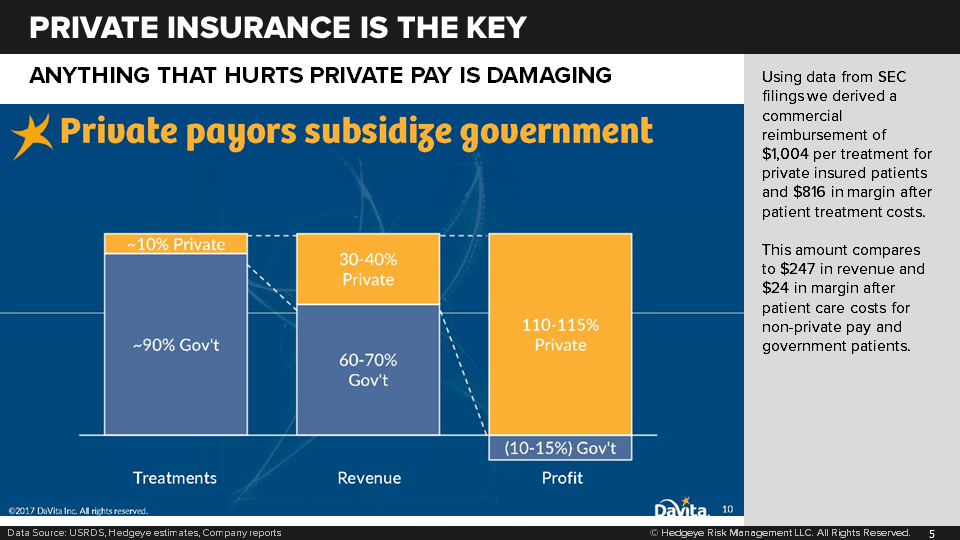

With the ~10% of patients who are commercially insured accounting for 110-115% of DVA’s profit, the increased regulation and prohibition of third party payments will be a much bigger deal to DVA than the baked in sale of DMG.

Additionally, DVA is planning to use the entirely of the sale proceeds for debt pay down with the company electing not to use the amount of $750 million permitted by their credit agreement for buybacks. Both consensus and our estimates include share buybacks funded by the deal proceeds in the 10-13 million share range.

On the facility cost level, wage rates continue to accelerate against an exceedingly tight labor market for registered nurses and alongside accelerating health care labor demand. Our forecast calls for a deterioration for the remainder of 2019 for the largest cost item in the P&L.

Of course, none of these items impact the negative mix issues being driven by demographic trends and the lack of acquisitions available to either DVA or FMS.

Call with questions.

Thomas Tobin

Managing Director

Twitter

LinkedIn

Emily Evans

Managing Director – Health Policy

Twitter

LinkedIn