THE HEDGEYE EDGE

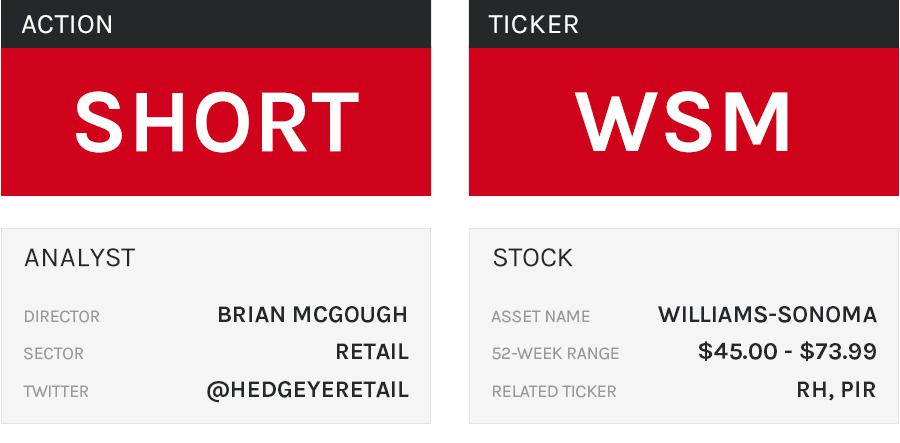

Below is our outline on the Williams Sonoma (WSM) short thesis:

Williams Sonoma and Pottery Barn might be brands to Baby Boomers and Generation X, but to Millennials the banners are overpriced concepts with the slow distribution networks of yesterday. Wayfair’s platform in particular represents an existential threat for Williams Sonoma with better customer service, lower prices, faster delivery times, and seemingly little interest in earning a profit any time soon. This is when Williams Sonoma should be investing in its future instead of cutting costs to beat a quarterly estimate.

INTERMEDIATE TERM (TREND)

Williams Sonoma is also over-earning. In the most recent quarter Williams Sonoma cut its SG&A spend to flat compared to the prior year. This is when the company needs to be making investments in order to better position its brands for the increasing competitive intensity from digitally native startups like Amazon and Wayfair as well as new online businesses and home product lines from large brick and mortar competitors like Walmart, Target, and Ikea.

Our Macro team is making a call for reversion into Quad 4 in Q319, after recent data is revising their GDP outlook. And while almost nothing in retail works long-side in Quad 4 (growth slowing, inflation slowing, dovish monetary policy) in particular you want to avoid high beta, small cap, high end consumer exposure, and leverage. In that Macro factor context, Williams Sonoma is especially poorly positioned. High-end spending takes a hit (i.e. short the rich) as market woes lead to wealth effect pressure on discretionary spending. Add on the certainty that 25% tariffs will have a particularly strong negative impact on the furniture business, and the timing is right to short WSM – even though valuation is undemanding at 13x earnings and 7.5x EBITDA. But Quad 4 is valuation agnostic.

Long Term (TAIL)

Ultimately WSM has a weak management team with zero vision for how to adapt for the changes in the industry. Williams Sonoma has no organic growth. West Elm is its only brand growing its store base, but it’s undifferentiated and slowing.

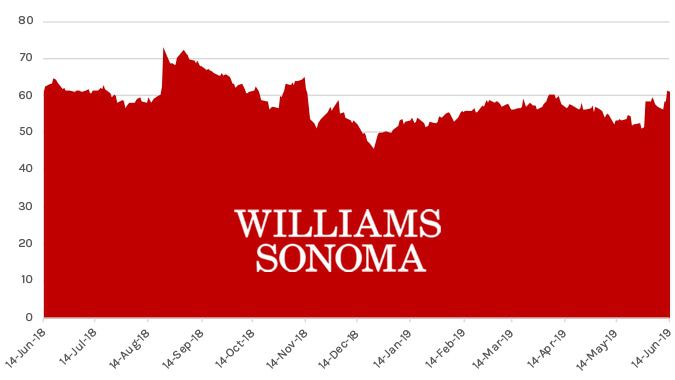

ONE-YEAR TRAILING CHART