Below are analyst updates on our sixteen current high-conviction long and short ideas. Please note that we removed Sony (SNE) from the long side and Lyft (LYFT) from the short side of Investing Ideas this week. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

EXP

Click here to read our analyst's original report.

We continue to see Eagle Materials (EXP) as one of the best longs in Materials (or Industrials for that matter).

Not only are the shares cheap relative to peers, transactions, and likely cash flows, but the company is exposed to several potential upside scenarios. These options include:

- An accretive sale to a competitor

- Substantial buyback, or

- Restructuring by shuttering/selling proppant business

Below are the key long thesis points on EXP from our Industrials and Materials analyst Jay Van Sciver.

GIL

Click here to read our analyst's original report.

Gildan Activewear's (GIL) management was in NYC meeting with investors this past week. While there were no major revelations, from what we heard management was very upbeat about gaining share via new private label contracts (management brought up the potential for category expansion at existing accounts) and the organic growth opportunity in fashion basics. The company is keeping financial expectations grounded with growth in the mid-single digits – a rate that we think will prove very conservative as it has officially entered the biggest capacity growth phase in over a decade. At the same time management is laying out how margins can push well beyond peak.

TSLA

Click here to read our analyst's original report.

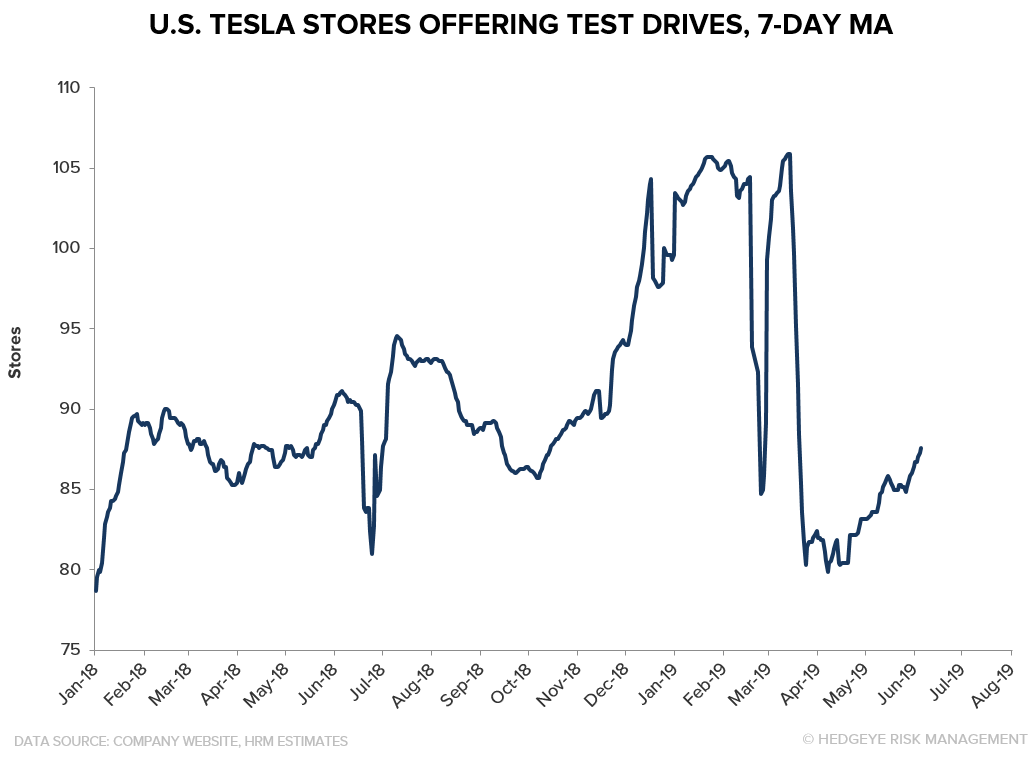

While Tesla (TSLA) CEO Elon Musk may have said “I want to be clear, there is not a demand problem” at the shareholder meeting, there are facts and data that suggest he isn’t being entirely - well - forthcoming. We continue to see ample evidence that demand is not matching lofty expectations. That Tesla management bothered to include a slide dismissing demand concerns is telling, as demand concerns have hit institutional confidence in the Tesla story. We’ve long thought that getting demand right was critical and we have built tools to track that core aspect of our thesis. On that front, we reiterate our TSLA short call.

ROL

Click here to read our analyst's original report.

Rollins (ROL)... Quality Bias, Or GDP-ish Grower? Acquisitions have filled in during periods of weaker organic growth. This is fine, as long as the acquisitions are reasonably priced and successfully integrated. However, smaller pest companies often have better relationships as acquisitions by larger players destroys culture and employee retention. We estimate that, across the pest control industry, the acquisition price relative to revenues has nearly doubled in the last five years.

With GDP-type organic growth rates, housing headwinds, competitive entry, and a feuding family with a controlling stake, one would reasonably expect ROL to trade at a discount to the market.

DVA

Click here to read our analyst's original report.

On Thursday, CMS sent to the White House for review a rule regulating third party payments to insurers on behalf of dialysis patients. According to a recent lawsuit in Florida, DaVita (DVA) contributes approximately $120 million to a third party, the American Kidney Fund, which, in turn, pays commercial insurance premiums for dialysis patients who receive about $400 million in services from DVA. As a result, about 10% of DVA's treatments account for 110-115% of its profit. While not likely to eliminate the practice entirely, CMS is sure to insist that dialysis providers engage in greater disclosure and reporting of the practice so patients are aware of their Medicare eligibility.

EAT

Click here to read our analyst's original report.

Knapp-Track (KT) released May sales estimates recently that showed continued weakness in both Restaurant sales and traffic. Bad weather may have caused some weakness, but not enough to call-out as a major problem.

KT reported casual dining comp sales for May 2019 of 0.9%, although positive on a 1-year basis, represented only a 30bps acceleration in the two-year average. KT comp traffic in January was (1.8%), representing (2.1%) and a 10bps sequential decline in the two-year average.

For the first two months of 2Q same-stores sales are flat and traffic is (2.0%). This compares to the first two months of 1Q19, where same-stores sales were 0.9% and traffic was (1.1%).

Three of our top four shorts in the Restaurant Sector are in the Casual dining sub-segment. Brinker International (EAT) is at the top of that short list. We reiterate our short call on EAT.

PENN

Click here to read our analyst's original report.

The Pennsylvania Gaming Control Board (PGCB) approved the Hollywood Casino Morgantown license, paving the way for the satellite to open in late 2020. This is the 1st mini-casino license granted by the PGCB. Construction will take about 18 months, and we had been modeling the $111m project to open in the beginning of Q4 2020 but it looks like it may not open until mid-to-late Q4 2020. We anticipate ~$50m and ~$13m in annual revenues and EBITDA from Morgantown in 2021.

Penn National Gaming (PENN) remains challenged by its financial structure and secular, macro, and competitive headwinds.

We measure a number of proprietary regional gaming metrics and demographic trends that have implications for regional players. Many of these threats are unknown or underappreciated by the Street, in our opinion. We reiterate our short call on PENN.

UNH

Click here to read our analyst's original report.

We're interested in UnitedHealth Group (UNH) as a technology forward company. It appears there have been 800,000 cumulative downloads since September 2015 with a growing monthly active user count of between 500,000 and 600,000 in recent months. These are impressive in both the trend and magnitude, although we don't believe the adoption of these techniques and technologies can entirely offset the rebate risks.

HQY

The US economy is balanced between two negative growth environments, Quad 3 and Quad 4 in Hedgeye terms, and the Federal Reserve that has already turned dovish and market yields have already fallen. With HSA member growth likely to continue to decelerate, and potentially decline in a recessionary scenario, we are watching HealthEquity's (HQY) deteriorating Risk Score as complimentary to our fundamental outlook. With fundamental pressures mounting, a negative economic backdrop, and a deteriorating Risk Score, high valuation, we remain short HQY.

NFLX

Click here to read our analyst's original report.

We believe investors are overestimating Netflix's (NFLX) pricing power and ability to drive further adoption in the U.S. with looming competition from content goliaths Disney (DIS) and WarnerMedia (T). We surveyed 1,000 U.S. consumers, and 40% of Netflix subscribers said they were either 'likely' or 'extremely likely' to subscribe to the Disney+ service.

We have developed a proprietary real-time model using mobile app download data to track international and U.S. paid membership growth, which tracks NFLX’s Int’l paid membership growth data with a 0.98 correlation over the last 7-years.

We see risk to 2H19 consensus subscriber estimates as the growth rate of Netflix (NFLX) mobile app downloads worldwide has slowed materially in recent months. The slowdown is occurring as the company works through a series of price increases in the U.S., Latin America and Europe. We believe NFLX mobile app downloads are a good proxy for gross subscriber additions based on the high absolute correlation to NFLX's reported metrics. The deceleration in growth is consistent with our view that price increases will slow the rate of adoption, especially in developed markets where NFLX is > 50% penetrated.

WSM

Click here to read the short Williams-Sonoma (WSM) stock report Retail analyst Brian McGough sent to Investing Ideas subscribers earlier this week.

SBUX

Starbucks' (SBUX) CEO is betting that Luckin’s growth is not sustainable. As Group President of International, John Culver, said on the last earnings call, “as a company in China, we're not looking to buy short-term revenue. Rather, we're looking at continuing to build on the 20-year history and the success that we've had in the market.” SBUX defense of increased competition has three components to it: (1) Premium quality of its coffee, (2) handcrafted beverages and (3) the exceptional third place experience created in each store and the emotional connection the Starbucks partners have with its customers.

The Luckin business model goes right at the heart of the SBUX business model. Luckin intends to open thousands of smaller locations near the current SBUX locations, charging significantly less than what SBUX must charge to justify the third-place experience and the emotional connection. What is that emotional connection worth to the Chinese consumers and why can’t Luckin build an emotional connection?

The goal of Qian Zhiya, CEO of Luckin, is clear “Our goal is to defeat Starbucks in China” and right now the market does not see any threats to Starbucks in China. We do.

W

Click here to read the short Wayfair (W) stock report Retail analyst Brian McGough sent to Investing Ideas subscribers earlier this week.

UBER

Click here to read the short Uber Technologies (UBER) stock report Industrials analyst Jay Van Sciver sent to Investing Ideas subscribers earlier this week.

NSP

Click here to read the short Insperity (NSP) stock report Industrials analyst Jay Van Sciver sent to Investing Ideas subscribers earlier this week.

MAR

Click here to read the short Marriott (MAR) stock report Gaming, Lodging and Leisure analyst Todd Jordan sent to Investing Ideas subscribers earlier this week.