Our Dollarama call is playing out, and while we’ll take the 11% move on the day, there’s considerably more upside to come as management pulls pent-up levers to introduce higher price points and re-accelerate earnings growth by a factor of 2x. So far the sales acceleration is primarily driven by the merchants executing on driving add-on consumable purchases. Effecting price increases with their other tools will likely start to happen in 2H and accelerate in 2020. DOL is a Best Idea Long, with 40%-50% upside over a TAIL duration. You get paid on this name by earnings growth alone – the inevitable multiple expansion is a bonus.

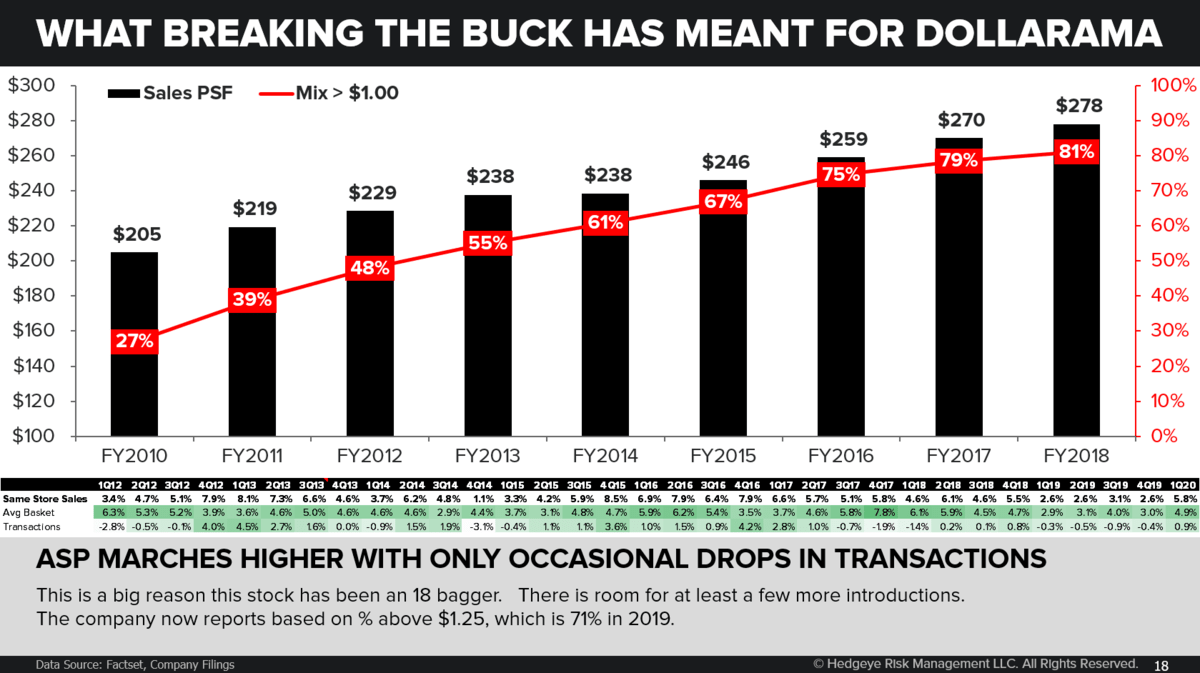

Dollarama reported SSS of 5.8% in Q1. This represented the strongest growth rate in two years. The comp increase was driven by both units per transaction and traffic. The most pushback we have received on our long DOL call has been the negative traffic last year. Even though the company before last year has only had just ten Qs of negative traffic in its ten year history since breaking the Canadian dollar price point. Negative traffic had not been a reliable indicator of future comp in the past. Without price increases or new $4.50 and $5 price points the Dollarama merchants entered this year with a plan to drive units per basket and traffic (if possible). The merchants focused on consumable basket builders as well having customers going to the cash registers to make their way through an aisle of items intended to be spontaneous add-ons similar to a longer version of a grocer’s/drugstore checkout counter. This clearly worked. I continue to believe Dollarama’s merchants are best in class and the most important of the company’s competitive advantages.

If there is any knock on the strong comps it is the gross margin contraction of 170bps. We were looking for an 80bps contraction. As a dollar store, Dollarama has limited ability to drive traffic through promotions. Management attributed the gross margin contraction to three causes: 1) Logistics costs -- specifically the construction of its second distribution center which is expected to be timing related. Management expects the headwind from the DC to continue in Q2 then fade. 2) The additional sales of consumables caused gross margin pressure. Most of Dollarama’s consumables are priced below $2 and have lower merchandise margins than other categories in the store. Consumables are generally sourced domestically and have a higher mix of brands than the other categories which are both causes for lower margins. 3) Dollarama merchandise margins were pressured from not passing on inflationary pressures.

Management was clear on the call that Dollarama will be the least aggressive among its competitive set to raise prices. It’s important to management that Dollarama maintains its ~25% pricing gap to the competition, but that doesn’t mean it can’t raise prices. We are starting to see price increases at Canadian grocers as they begin to pass on inflationary pressures in food from a weaker Canadian dollar. In hardgoods we are not yet seeing price increases at Walmart and Canadian Tire. The company still has two other methods for raising price. It has introduced higher price points in the past which have proven to bring higher merchandise margins, but we don’t expect to see the $4.50 and $5 price points until next year. Dollarama also refreshes 25-30% of SKUs each year which can have higher prices than the items it replaces on the shelves, but aren’t “price increases” since the items are new. Due to the longer planning required on refreshed items this benefit will accelerate throughout the year, especially in the seasonal items in the 2H.

Dollarama sets up perfectly in our Macro Team’s GIP (growth/inflation/policy) quad framework. Canada just exited Quad 4 (Growth Slowing as Inflation Decelerates) and like the US, is currently in quad 3 (Growth Slowing as Inflation Accelerates). Unlike the US, which is stuck in Quad 3/4 for another 2 quarters, Canada is set to shift into quad 2 (Growth Accelerating as Inflation Accelerates) and then Quad 1 (Growth Accelerating as Inflation Decelerates) later this year. Dollarama is exactly the kind of defensive consumer name you want to own in Quad 3, and works even better in accelerating environment of Quad 2, and then at the time we see Quad 1 (when virtually anything in consumer discretionary works) we’ll get visibility into higher price points and comp acceleration at DOL. Management reaffirmed guidance for this year, so there’s safety in near term numbers…then the Macro climate is at its back, and a multi-year company-specific growth ramp drives this beast higher. There’s your multiple expansion call.