THE HEDGEYE EDGE

Insperity (NSP) is a highly cyclical company. Shares of Insperity are trading as though the PEO (i.e. Professional Employer Organization – providing comprehensive HR solutions for small and mid-size businesses) industry isn’t cyclical and increasingly mature. The cyclical elements extend beyond employment trends to costs, regulations, and marketing.

Economic growth appears to be slowing. The Hedgeye Macro team sees an environment of U.S. Growth Slowing throughout 2019. As we move from US Macro Quad 3 into Quad 4 (both real growth slowing) and Insperity faces more difficult comps, we think shares re-rate downward.

Why? Many of NSP’s cost items are pro-cyclical and may increase in a weakening economy. Insperity unit metrics track broader employment trends. A tight labor market pulls workers off the sidelines, while driving the need for better benefits. NSP gets a profit benefit if the estimated benefits cost change imbedded in pricing is less than the experienced cost increase. In the past seven years, benefit cost increases have been small to negative, so pricing has been as well. Benefits are often used more when employees are worried about job security. Busy, happy, employed seem to consume fewer benefits.

Employers have likely grown to expect muted price increases and may be experiencing other labor cost pressures. If the estimates used in pricing end up too high, say because of COBRA usage or other factors, recent gains in Gross Profit per Worksite Employee (GP/WSEE) could stall, or more likely, reverse.

If wage pressures increase and NSP tries to raise prices in a slowing economy to cover benefit cost increases, will churn increase? Seems likely. Other PEOs have seen retention increase, and churn is typically procyclical. Higher churn in recessions tends to add to unit costs at an already difficult point in the cycle. NSPs contract with its clients can typically be canceled within 30 days.

In short, we see a return to stagnation (or worse) based on the following:

- Costs per WSEE often decline in robust economies and increase in weak economies, exacerbating cyclicality.

- NSP itself discloses that $5 of the $11 GP/WSEE improvement was due to “changes in cost estimates for benefits and workers compensation.” Those changes can also detract if costs are greater than estimates.

- GP/WSEE gains have been surprisingly modest, although the company cites mix of customer size and other factors.

Ultimately, NSP’s PEO business has also benefited from legislative changes that made employment more complex for about a year. Tax reform was about a year ago. But we think this spurt in activity that benefited NSP won’t last beyond 2Q19.

Obviously, we don’t think NSP’s 2018 surge was merited. NSP’s excessive valuation leaves shares vulnerable to disappointment, too expensive for strategic interest and likely to revert after the tax reform bump fades.

The industry has enjoyed exceptional tailwinds in recent years, while limited Street coverage, arcane business metrics, and a move up in index membership have left the shares untethered to underlying business realities.

With steep comps, intensifying competition, slowing growth, and a lack of incremental tailwinds, investors will likely be just as surprised by the cyclical downside as they were by the post-GFC recovery. We see greater than -50% downside in the shares, with catalysts positioned through 2020.

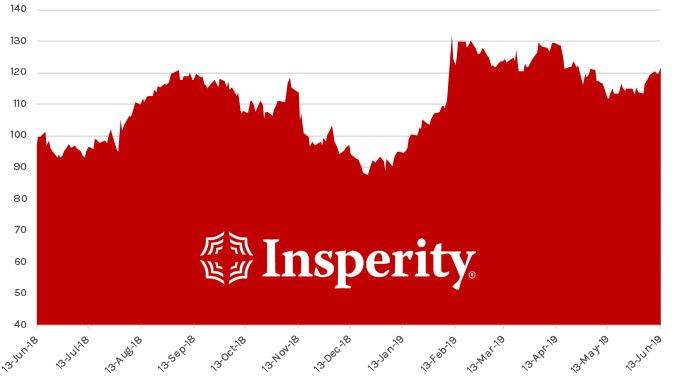

ONE-YEAR TRAILING CHART