R3: REQUIRED RETAIL READING

April 23, 2010

TODAY’S CALL OUT

Earnings season across the retail , apparel, and footwear space is hard to define. At the moment we’re in a period which one may describe as the “Creep”- essentially the build up into the bulk of earnings, and usually the period where the Street looks to take direction for the results on the horizon. With that said, there were a few interesting callouts from the past day or two:

-Decker’s management (and results) were about as bullish as we can remember as it pertains to the Teva Brand. After about five years of efforts to reposition the brand as an outdoor lifestyle product beyond the traditional open-toe sandal, results are beginning to take hold. Sales for the resurgent brand were up 21%, with the company noting that Teva is gaining share as well as traction with a younger demographic. Recall that the big challenge for the brand has been to create credible closed-toe offering, something that is now working in both Spring and Fall (as indicated by the backlog commentary).

-COLM’s backlog was up a strong 19% for the Fall. Importantly, management noted that part of the strength can be attributed to the company’s focus on innovation via the Omni-Heat platform. While the technology is still not proven from a retail sell through standpoint given its impending Fall launch, the company expects to support the product with an extensive integrated marketing effort. Plans call for in-store graphics and fixtures, print and online campaigns, as well as the company’s first new television commercials in two years.

-After indicating that sales momentum was “absolutely encouraging” in March, Sherwin Williams management went on to note that trends have continued into April. Interestingly, there is a bit of a catch-22 with the strengthening of the topline across the industry. Management noted that tight supplies of raw materials in the wake of improved sales will likely keep pressure on costs at least until the back half of the year.

-J Crew’s creative director was on Oprah on Wednesday, with the most interesting part of the segment revealing that Oprah herself is long some good old JCG in her PA. Even better will be the boost she gives the quarter as a result of loyal viewers heading out to purchase J Crew wares as seen on TV. It almost sounds like a conflict of interest on Oprah’s part. In all seriousness, it will be interesting to see if the show has any impact in light of Oprah’s history of having a positive sales impact on other brands in the past. Payless and Deckers are two that come to mind.

-While the consumer electronics industry and retailers alike are excited about the prospects for 3D TV (and the ability to charge more), another technology is also getting a boost. South Korea’s LG, is ramping up production and investment in OLED- a technology that offers the ability to offer very high contrast ratios, deep black levels, all in a very, very thin profile. The technology is not backlit, which allows for such features. Currently, the technology is expensive to produce and is only available in smaller screen sizes. LG’s investment should pave the way for faster adoption over the next 3 years.

Eric Levine

Director

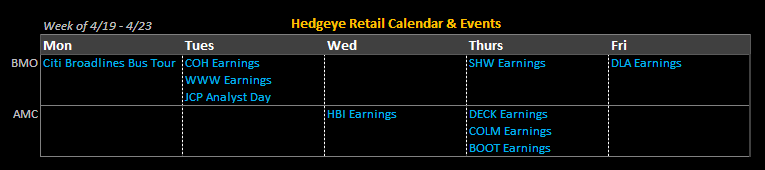

HEDGEYE CALENDAR

MORNING NEWS

Adidas Preannnounces Large Upside - Adidas Group said its preliminary results for the first quarter showed a 4% gain in sales and significant improvement in profitability. The better-than-expected results prompted Adidas to lift its full-year profit outlook to €2.05 - €2.30, up from its previous guidance of €1.90 - €2.15. Guidance was raised due to better than expected sales and margin with increased gross margin and operating expense leverage.

Largest Hong Kong Listed Clothier Sees Sales Declines Due to European Weakness- Esprit Holdings Ltd. said fiscal nine-month sales fell 1.8% as households in Europe, where it makes 84% of revenue, curbed spending. Consumer confidence in Europe remained weak in the first quarter. February retail sales in the 16-nation Euro region declined 0.6% from January, when they decreased 0.2%, the European Union’s statistics office in Luxembourg said April 8. Sales in Asia rose 5.8% and gained 8.4%. Espirit is pushing expansion in China where it says margins are similar to those in Europe. The company has bought out partner China Resources Enterprises Ltd.’s stake in their Chinese textile venture. <bloomberg.com/news>

UA Hires Senior VP of Apparel - Under Armour announced that Henry Stafford will join the company as senior vice president, apparel in June 2010. Stafford has extensive experience in the apparel industry, which includes top positions with American Eagle Outfitters and Old Navy. <sportsonesource.com>

Sears to Operate Edwin Watts Golf Shop in Shops - Sears Holdings Corp. signed an agreement with Edwin Watts Golf Shops LLC to operate 12 golf shops inside Sears stores. The shops, ranging from 2,700 to 3,000 square feet, will be located near Sears electronics, tools and sporting goods department. <sportsonesource.com>

Should Nike Drop Ben Roethlisberger? - This much is clear. However long Nike's contract with Pittsburgh Steelers quarterback Ben Roethlisberger is, the allegations against him (even if they won't be prosecuted), will assure us that Nike will never use him in a commercial again. Why doesn't Nike drop Ben now? The short answer seems to be that Nike doesn't sever contracts with athletes who haven’t committed a crime or haven't been found to use performance enhancing drugs. And without Roethlisberger being charged or convicted of sexual assault, he fits the bill of still staying under the Nike athlete roster. In July 2007 when Michael Vick was charged in a dogfighting scheme, Nike suspended his contract without pay. But it wasn’t until after he pleaded guilty, that Nike terminated its contract with him. <cnbc.com>

Brazil the Next Hot Spot for Luxury Brands? - Brazil might not offer luxury brands the same potential in terms of size as Russia, India or China, but it provides more near-term opportunities for expansion. Events such as the 2014 World Cup and the 2016 Summer Olympics, both to be held in Rio de Janeiro, could significantly boost local markets and justify additional openings. Although it is Latin America’s biggest economy, Brazil is often overlooked because its population of 192 mm is lower than that of China and India, which both top the one billion mark. Luxury retail distribution is extremely limited, with more than one-third of the companies in a sample of 15 leading luxury brands having no direct retail presence in the country. More than three-quarters of luxury stores are located in the financial hub of São Paulo, mainly in upscale malls. Brands with no retail presence in the country, such as Prada, Fendi and Burberry, have the option of entering via São Paulo and expanding from there. <wwd.com/business-news>

China Imposes Nylon Tariff - China imposed punitive tariffs on nylon imported from the U.S. and other countries on Thursday, alleging the goods damaged its domestic industry. The Ministry of Commerce said China will impose antidumping tariffs ranging from 4% to 96.5% on nylon-6 imported from the U.S., the European Union, Russia and Taiwan, according to state media reports. Antidumping tariffs are applied when imported goods are sold for less than fair market value or below the cost of manufacture. Nylon-6, also called polycaprolactam, is used to make products such as hosiery and knit apparel. The nylon tariffs will be in place for five years, extending temporary duties China established last fall. According to the International Trade Commission, in 2009 the U.S. exported $189.6 mm of polycaprolactam chips, which includes nylon 6. <wwd.com/business-news>

Vietnam's Textile Industry Harmed by Rising Cotton Prices - Vietnam Textile and Apparel Association reports that cotton price is estimated at USD$1.9-$1.92 per kg now, a 35% increase from January, and up to 50% jump in comparison with the same period last year. The price of imported cotton has been soaring since the beginning of the month. The local textile and garment production which relies heavily on imported cotton is threatened by the surge of cotton price. Furthermore, it makes worse situation for those Vietnamese enterprises signed contracts with international partners before the price increase, leading to further profit reduction. <fashionnetasia.com>

BOOT Grows Sales 32% - Sales in the workboot market jumped 38% to $26.3 million, while outdoor market sales increased 15% to $7.9 million. “We’re very pleased with our strong sales and earnings growth in the first quarter of 2010, driven by increased demand across our different channels and markets,” said Joseph Schneider, president and CEO of LaCrosse, in a written statement. “We saw very strong demand from various branches of the U.S. government due to the continued strengthening of our customer relationships throughout the government channel and our strong execution in exceeding their delivery timetables. We also saw much stronger at-once demand from our wholesale channel partners during the first quarter, reflecting the improved consumer spending environment and success of our core products.” <wwd.com/footwear-news>

Rocky Brands Reports Unimpressive Margins, Impressive Sales-Inventory Growth Spread - Net sales rose 12%, wholesale revenues advanced 5% and retail sales declined 5.8%. “Our first-quarter results were above internal and external projections driven by higher sales in our wholesale and military segments combined with improved operating expense leverage,” said Mike Brooks, Rocky chairman and CEO, in a written statement. "With regard to our bottom line, the seasonality of our business makes it difficult to realize positive earnings during the first quarter, which is typically our lowest volume sales quarter.” Nelsonville, Ohio-based Rocky also said Thursday that its Dickies footwear licensing partnership with Williamson-Dickie Manufacturing Co. will end effective Jan. 1, 2011. <wwd.com/footwear-news>

Tommy Hilfiger Finds a Better Way to Get and Engage Interested Customers - The fashion apparel brand and retailer has long known the value of e-mail marketing, but it has found a new cost-per-lead advertising system of acquiring e-mail addresses a better way to quickly engage prospective customers interested in its brand. <internetretailer.com>

UK Outdoor Footwear Brand Hi-Tec Grows Big - British outdoor and sports brand Hi-Tec is highlighting its growing strength and performance within the athletic and outdoor footwear markets. According to a company release, Hi-Tec’s Athletic footwear sales rose by 63% and Hi-Tec’s Outdoor footwear sales rose by 48% against the comp period in 2009. <sportsonesource.com>

Luxury Perfume Grows Most in 3 Years at L'Oreal - L’Oreal SA, the world’s largest cosmetics maker, said sales growth accelerated to the fastest pace in almost three years as shoppers spent more on luxury perfume and distributors stopped cutting inventories. <bloomberg.com/news/retail>

Remington Arms Hires New Agency to Contemporize the Brands Image - Campbell-Ewald has added Remington Arms and its subsidiaries and affiliates under the Freedom Group of Cos. following a review. The IPG agency takes over from Brothers & Co., and will handle advertising, media, digital marketing, social-media outreach and product development.

New work is slated to break in the fall, backing the company's waterfowl hunting firearms. The company spends about $1.5 million annually on ads, per Nielsen. <brandweek.com>

Clogs Hit the Junior Footwear Market - Clogs are hitting the juniors market for fall '10 with styles ranging from the classic wooden platform in neutral leather to freshened-up looks in bright knit. <wwd.com/footwear-news>