“We’re attuned to potential risks to the outlook. If we saw a downside risk to the outlook, then that would be a factor that could call for a more accommodative policy.” -Richard Clarida, Fed Vice Chairman, yesterday

Reflation continues to take his ball and go home. It’s all Quad 4 out there again this morning.

On the market side, Oil is down (another) -1.6% and continuing to break bad, the pike formation in Inflation Expectations remains ongoing, Dr. Copper’s differential diagnosis on global growth remains unequivocal, DM bond yields continue to plumb new lows, negative yields and curve inversions continue to proliferate globally, credit spreads widening remains pervasive, Semi’s are down -15.4% (for the month!) and U.S. & EU equity benchmarks are pacing for their first monthly loss of the year.

On the fundamental front it’s a congruous story.

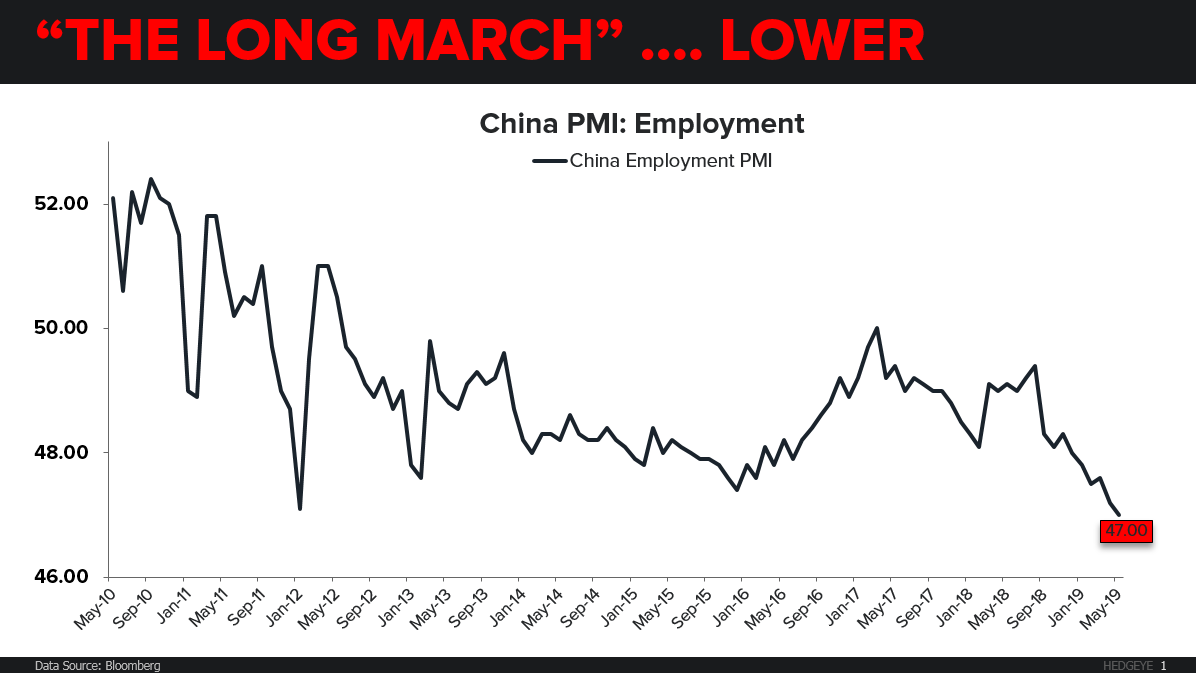

Brazil GDP printed negative, Italy GDP printed negative, South Korean and Japanese Industrial production growth remained negative and China’s Manufacturing PMI missed as New Orders re-breached 50 to the downside, Export Orders fell to an increasingly contractionary 46.5 while factory employment printed a fresh cycle low.

On the geopolitical front, the latest policy by tweet decree vis-à-vis Mexico is only serving to amplify growth angst that was already in crescendo.

Not to put too broad a stroke on it, but at some point, the market becomes overtly disabused of the notion that quantifying or otherwise reasonably discounting the derivative effects of a multi-front trade war is a tractable exercise and just punts... particularly when a stubbornly persistent drip of Quad 3/Quad 4 (growth slowing) high frequency, global fundamental data continues to confound green shoot enthusiasts, price momentum is corroborating those fundamental trends and the first order effects of the latest trade escalation haven’t even hit yet.

Granted, the Friday policy broadside is a somewhat quixotic choice given Trump's penchant for proxying his performance via market prices and one supposes the “Trump put” isn’t too far out of the money here, but low conviction suppositions aren’t a risk management strategy.

And, of course, the post-GFC paradox remains alive as ever. Bad is bad until it becomes bad enough that it becomes good as expectations for rhetorical or explicit policy easing drive the re-rotation into reflationary exposures and long carry strategies.

But, as investors were again reminded over the past three quarters, there’s a lot of risk, price reflexivity and PnL in the spread between willfully blind equity ebullience and low liquidity, reflexive drawdowns.

The latest cross-asset, global price action is also a reminder of the increasingly complex, interconnectedness of global markets and commerce – to which the push towards protectionism is an explicit affront.

That reality holds all manner of political, social, and economic implications and the complexity of that interconnectedness is what makes teasing out the higher-order and network effect with any precision so challenging.

For our purposes, the simple point is that nothing in global macro happens in a vacuum or via a single channel.

Take policy tightening as an example: Tighter policy generally = more demand for dollars which is dollar positive, but the other side of the more demand coin is lower supply, and a shift in both the supply & demand lines pushes the equilibrium price higher than a shift in either line in isolation.

That’s about as 101 as it gets.

As simple as that is, however, it’s only really one level (of complexity) removed from practical investment implications and the important reality that most macro integrations of consequence are reflexive cycles .... slowing growth begets a stronger dollar and a stronger dollar is disinflationary and also cultivates tighter financial conditions for a global economy that transacts and finances in U.S. dollars. Both of which serve to further pressure growth and around we go.

That Growth-Currency setup characterizes (global & local) Quad 4 and currently prevailing conditions. Typically, and predictably, the central bank reaction function in Quad 4 is easing … which serves to reflate asset prices while generally pushing the economy into Quad 3.

We go to Quad 3 because prices are comparatively more sensitive to the policy response while growth remains hostage to base effects and gravity of the cycle. Outside of some mammoth, immediate stimulus injection with direct flow through to the real economy, a move from Quad 4 directly into Quad 1 or 2 only occurs if the underling cycle is set to inflect anyway, in which case the effect is to amplify or accelerate that inflection.

We saw this exact procession of dynamics to start the year, except the currency impact (i.e. lower Dollar) of the Fed pivot was muted by the subsequent, commensurate pivot out of everyone else, leaving the relative change the same.

So, no matter where you go this morning, here you are.

On with the Global Macro Grind …..

If you do this long enough you’re amusingly reminded that everyone is an insta-expert on everything. Who knew there were so many rare earth experts until this week?

Q: How rare is the rarest rare earth metal?

- Rarest mineable element on earth.

- Half as rare as gold.

- About as rare as gold.

- None of the above.

A: Thulium, the rarest rare earth metal, is, in fact, 125X more common than gold.

I certainly didn’t know that. Tbh, I thought “rare” meant “rare”, not rare in the sense that they are dispersed in low concentrations across the planet.

Of course, we don’t claim to know everything or hold analytical dominion over all macro and market phenomenon.

We do claim to have a process to measure and map evolving macro dynamics. The Slope Citizenry of @Hedgeye faithfully employ a second derivative centric process. We’re proficient in tourism but over here we speak RoC-anese.

It’s a close but non-exclusive brotherhood. Everyone is welcome and encouraged to join.

Anyway, I’m trying to keep it tight and light here to close the week.

The larger point, I suppose, is that just because we are charged with high frequency, tactical macro commentary doesn’t mean the investment landscape undergoes wholesale changes on an hourly or daily basis.

Sometimes phase transitions are actively in motion, critical thresholds are being breached and there is a lot to do. Most of the time, active risk management simply involves risk managing an exposure within its given rage range and within the prevailing Trend.

As it relates to recent and current market developments, let me simply come back to what I said a couple months back:

|

“What you’d like to be long is redundancy. … Complex bio-physical pathways are a marvel of redundant systems. Redundancy is a defining feature of evolution not a byproduct…. If you want an investing process for the long-term, you can be like Buffet, take a bath and hope for an epiphany or you can model Mother Nature and get long redundancy. For our purposes, long redundancy equates to being long exposures that work in Quad 4 and Quad 3 or, more preferably, that work in both” |

There can be elegance in simplicity. If that simplicity is distilled out of macro complexity by a repeatable process, all the better.

Best of luck out there today and enjoy the weekend. Sunny, 70’s (and the longest U.S. expansion ever) on tap.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signals in brackets) are now:

UST 10yr Yield 2.18-2.41% (bearish)

UST 2yr Yield 2.03-2.22% (bearish)

SPX 2 (bearish)

RUT 1 (bearish)

NASDAQ 7 (bearish)

Utilities (XLU) 57.38-60.25 (bullish)

REITS (VNQ) 85.76-88.65 (bullish)

Financials (XLF) 25.28-26.95 (bearish)

Shanghai Comp 2 (bearish)

Nikkei 20811-21370 (bearish)

DAX 110 (bullish)

VIX 14.19-20.54 (bullish)

USD 97.12-98.35 (bullish)

EUR/USD 1.11-1.13 (bearish)

USD/YEN 109.00-110.50 (bearish)

GBP/USD 1.25-1.28 (bearish)

USD/CHF 1.00-1.02 (bullish)

Oil (WTI) 55.27-60.20 (bearish)

Nat Gas 2.50-2.70(bearish)

Gold 1 (bullish)

Copper 2.60-2.74 (bearish)

Christian B. Drake

Macro Analyst