TREND WATCH: What’s Happening? The spread between long- and short-term bond yields, after narrowing for more than two years, is now turning negative. This worries investment advisers—since “yield curve inversion,” perhaps the most ominous phrase in the financial lexicon, has directly preceded each and every recession since Elvis recorded “Heartbreak Hotel.” Others aren’t convinced that the term spread-business cycle relationship will hold up this time around, for reasons including the strength of the economy, QE, the low level of interest rates, and negative “term premia.”

Our Take: The arguments of the critics aren’t persuasive. The term spread reflects a rich variety of business-cycle dynamics—everything from central bank policy-setting, the timing of firm capex, and bank lending to consumer sentiment and rational investor expectations about the future. So when the yield curve inverts, the negative term spread cannot be explained away by any one errant variable. All eyes are now on the Fed, which doesn’t want to lose face by cutting rates again so soon after raising them. Markets, on the other hand, expect the Fed to do just that. Alas, it may be too late for the Fed to avert recession no matter what it does.

TERM SPREAD... TOUCHDOWN!

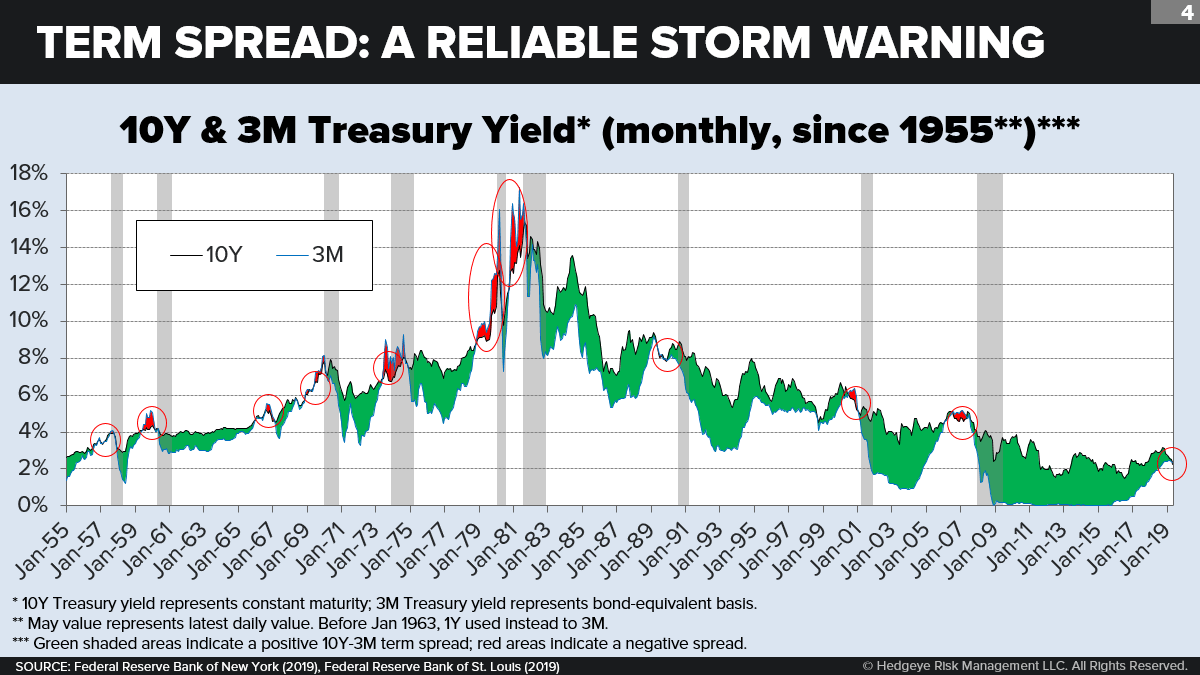

Like a flying stone starting to skip on the water, the long descent of the term spread (10 year minus 3 month) is at last beginning to turn intermittently negative.

Two months ago, on March 22, 2019, the spread turned negative for the first time in nearly 12 years (since August 27, 2007, to be exact). It stayed negative for six market closes in a row, until March 28. Then it went positive again. A couple of weeks ago, it went negative on two daily closes (May 13 and May 15). Now, two days before Memorial Day weekend, it went negative and—thus far—is staying negative.

As of market close today (Friday), the spread hit negative 21 basis points. The stone, at last, may have stopped skipping and started sinking.

We anticipated this was likely to happen ten months ago. (See “The Power of the Spread.”) In this note, we “revisit” the term spread.

Let’s cut to the chase. What does this yield curve inversion—or any yield curve inversion—have to do with the timing of the next recession?

The answer to this question has two parts. First, we need to determine the exact starting date. When can we truly declare that a new inversion period has commenced? After looking at the research and the daily historical data, I conclude that a good working definition of starting date is any day followed by more than six consecutive negative market closes of the 10-year minus 3-month spread.

Back in March, by this definition, the inversion came tantalizingly close to filling this condition—but didn’t quite get to a seventh day. Let’s see if we get there by early next week. Or by early next month.

Once the starting day is established and clock starts ticking, how much time do we have before the next recession begins? Well, if you follow the track record, the next recession will begin somewhere between 6 months later and 16 months later. The shortest lag was set by the recession of 1973-75. The longest lag was set by the recession of 2007-09.

Which inversion indicator works best? IMO, the 10-year minus 3-month spread has the best timing record. As we will see below, economists Arturo Estrella and Frederic S. Mishkin came to that conclusion in 1995. And the New York Fed uses this spread to calculate its recession probability indicator. But other indicators also work well. The 10-year minus 2-year is a commonly used alternative.

How reliable is this recession warning? Very reliable. Each time a major term spread has turned negative since just before the 1957-58 recession, a recession has ensued within the next two to six quarters.

Over these same sixty-odd years, there has only been one false positive: In 1967, after several Fed hikes put a nasty squeeze on investment, GDP faltered—without however triggering a recession.

In earlier decades, as far back as the data allow, the same basic business-cycle pattern in term-spreads prevailed: Spreads widened coming out of recessions and narrowed at the end of recoveries. But exact “inversion” comparisons before the late 1950s are difficult for many reasons—including reshuffled bond maturities; the Fed’s subservience to the Treasury during World War II and the Korean War; the severity of the Great Depression; and different tax treatment for short- and long-term government debt.

Unmistakable term inversions, however, did occur. The Crash of 1929, for example, was preceded by the mother of all inversions: For nearly two full years (January 1928 to November 1929), 3- to 6-month Treasury yields exceeded long-term Treasury yields—and did so by an average of 91 basis points. The maximum inversion, reached in the summer of ’29, hit an impressive 145 basis points.

Term spreads don’t just predict recessions. They also closely track future economic growth. This implies that, even if the yield curve doesn’t fully invert this month or next—or even if it does and a recession is somehow averted—the course is already set for an impending business-cycle slowdown. Plenty of economists are thus pointing to the narrowing term spread as a giant amber warning light, if not a giant red stoplight.

Others aren’t convinced. They say things are different this time around.

Who’s right? Let’s investigate.

TRACK RECORD AS A LEADING INDICATOR

Economists have been studying the relationship between the yield curve and the business cycle ever since they were able to get their hands on plentiful macro data—that is, at least since Wesley C. Mitchell (a numbers glutton if there ever was one) published Business Cycles and Their Causes in 1913. More recently, in 1965, University of Chicago economist Reuben A. Kessel was probably the first to tie term spreads to predictable phases of the business cycle. He wrote that, since the end of WWII, the gap between 20Y and 3M yields tended to widen coming out of a recession and to narrow heading into a recession, with outright inversions only occurring at business-cycle peaks.

For the next four recessions, interest in the topic languished. Then, in 1988, Campbell Harvey (who now teaches at Duke) submitted a remarkable doctoral dissertation for the Chicago Business School that tested the yield spread as a recession forecaster. He concluded that “yield spread forecasts are at least as reliable as those from the commercial econometric services.” That same year, Chicago Fed economist Robert Laurent similarly concluded that the term spread compared favorably to other available economic indicators.

Soon thereafter the term spread became a staple of econometric modeling and forecasting. In 1995, researchers Arturo Estrella and Frederic S. Mishkin tested various leading indicators to gauge which ones were best at signaling future recessions. They found that the 10Y-3M term spread performed better than any other indicator, including variables such as stock prices and changes in the money supply. The Federal Reserve Bank of New York even publishes a model that uses the 10Y-3M spread to predict the likelihood of a recession occurring within the next 12 months.

There’s a reason why forecasters are in love with the term spread: Historically, its performance is nearly flawless. Researchers at the Federal Reserve Bank of San Francisco noted last year that every U.S. recession since 1955 has been preceded by a negative 10Y-1Y term spread. They also noted (as we have seen) the single false positive in 1967. The rule appears to hold even when substituting 1Y Treasuries for 3M or 2Y Treasuries.

To be sure, this sort of binary “probit” modeling has its downside. After all, there have been only a small number of recessions in the postwar era, especially back when economists first started studying this topic. There are thus only a handful of data points on which these models can be trained. Another drawback is that the odds of a recession in these models don’t rise dramatically until the next recession just about underway. It’s like turning the signal lamp red when the locomotive is only 30 seconds away from an oncoming train.

But, as it turns out, the term spread is useful not just as a recession indicator. It’s also a superior leading indicator of future GDP growth. Laurent back in 1988 compared the term spread between 20Y Treasuries and the federal funds rate with three other leading indicators—the level of the nominal federal funds rate, the level of the real federal funds rate, and the growth rate of the money supply (real M2). He found that, between 1964 and 1986, a predictive model based on the term spread would have been the best at forecasting near-term real GNP growth.

We tested this idea ourselves by comparing the 10Y-3M term spread with future GDP growth. Going back to 1959, we see that the term spread decently tracks the 6Q-forward GDP growth rate, both in direction and magnitude. This relationship puts to rest at least one big criticism levied against the term spread—that it is not informative until it turns negative.

The term spread stacks up well against other leading economic indicators. Unlike many of the others, which hinge on monthly or even quarterly data, the term spread is real time. It can be calculated at any moment. It is also context-agnostic: Policy decisions and macroeconomic trends which may affect the absolute level of interest rates (expected inflation, for example) often have marginal impact on the spread between rates.

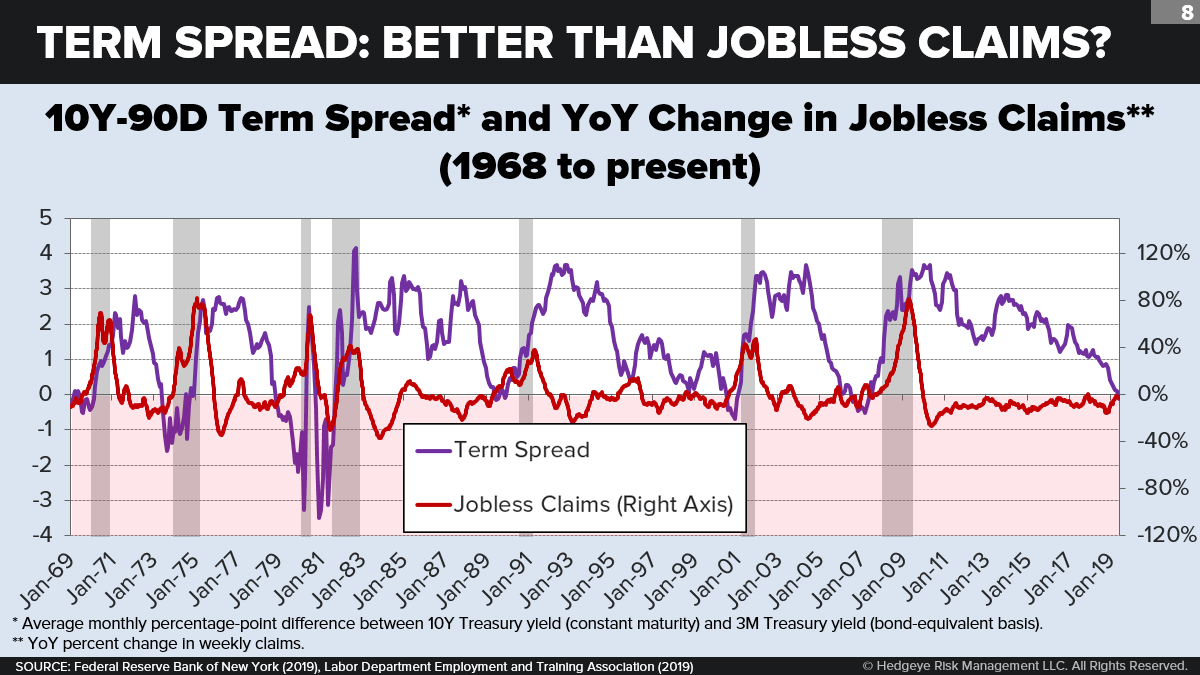

Let’s compare the term spread with two other trusted leading indicators. First, we look at the “consumer confidence spread,” which is the difference between people’s future expectations and their perceived current condition. (Once people start feeling that they’re doing much better today than they will be doing tomorrow, a recession is typically close at hand.) Over the past several decades, the term spread and the confidence spread have moved in lockstep. Second, we look at the 3-month average initial jobless claims. This is a decent indicator, but not as good as the term spread—since jobless claims sometimes don’t begin rising on a YoY basis until well into a recession.

WHY IT WORKS

Normally, a long-term security carries a higher yield than an equivalent short-term security, even in the absence of default risk (a plausible assumption for U.S. Treasury debt). This higher yield, reflecting a “positive term premium” or bias, compensates investors for the downside risks of locking their money up longer term—risks that include crisis illiquidity and rising inflation expectations. Most of the time, in other words, investors demand a premium in return for lengthening the duration of their commitment.

But most of the time is not all the time. Why does the yield curve sometimes invert? And why is an inversion so closely associated with the next recession?

Business-cycle effects: central bank policy. Monetary policy is the most direct and obvious driver of the yield curve cycle. Going into a recession, the central bank serves as a “lender of last resort,” dramatically lowering short-term rates to ensure that commercial banks remain liquid and consumers remain inclined to spend. Conversely, when the economy is running hot, the central bank hikes short-term rates to curb aggregate demand and thereby stay ahead of inflation.

While the long end of the yield curve is not immune to Fed manipulation (witness all the QEs in recent years), it is mostly driven by investor expectations stretching far beyond the current phase of the business cycle. It is therefore slow to respond to Fed policy. The short end, however, is closely riveted to the Fed’s interest-rate target (typically, the federal funds rate). So when the Fed puts on the brakes and raises the short end 200 to 400 basis points over the CPI, that usually pushes the short end higher than both long-term future expectations of short-term rates and the term premium.

In other words, the inverted yield curve happens when the Fed is throttling the economy out of fear of rising inflation. That throttling in turn initiates the next recession—hence the adage that expansions never die of old age but are rather “killed by the Fed.”

Business-cycle effects: the real economy. The natural rhythm of employment, investment, savings, risk-taking, and expectations also underlies the yield curve cycle.

Over the course of the business cycle, the national savings rate rises. When the economy just emerges from a recession, there are lots of borrowers—households, firms, and (especially) the federal government—and not many savers. Even with weak capex, this demand for credit and liquidity stresses credit markets. While the short end is held low by the Fed, the long end is kept higher than it otherwise would be by the multitude of borrowers. These include firms and households that want to take advantage of relatively low long-term rates by refinancing. The duration of corporate bonds typically jumps early in a recovery.

All this reverses late in the business cycle, when there are more savers and fewer borrowers, when employment and production are decelerating, and when long-term financing seems a lot more expensive.

Early in the cycle, the yield curve is steep but still low at the long end, encouraging deals by borrowers who think it can’t go much lower. Late in the cycle, the yield curve is flat but still high at the long end, discouraging deals by borrowers who think it can’t go much higher.

Business-cycle effects: commercial bank lending. Consider how commercial banks operate. They are in the business of “maturity transformation”—taking short-term credit and transforming it into long-term loans. The more dramatic the upward slope of the yield curve, the more profitable this business is. But what happens near the end of the business cycle as the yield spread flattens and ultimately inverts? The industry’s “net interest margin” (the difference between income from loan assets and payments to depositors and other creditors) gets squeezed. Soon, banks are paying out more in interest on short-term loans than they are receiving in interest on long-term loans. This eliminates the incentive to lend, which suppresses economic activity.

Business-cycle effects: investor speculation. Finally, let’s look at speculation, which both amplifies the term-spread cycle and accelerates its timing. This is in some ways the most decisive force, because global speculators have bottomless pockets when they sense they can make a sure duration bet.

What’s the rationale for this sure bet? It comes from traders knowing or at least sensing where they are in the business cycle. When traders think that a recession has just passed and the worst is over—and that the entire yield curve is about to start rising—they will short the far end and park their extra money in the near end. They will simultaneously make money while steepening the curve.

Likewise, when they think that an expansion is getting old and the best is over—and that the entire yield curve is about to start sinking—they will go long the far end and avoid the near end. Once again they will make money, only this time they will help to flatten or invert the curve.

RESPONDING TO THE SKEPTICS

Most economists and policymakers are aware of the historical relationship between the term spread and the business cycle. But not everyone agrees that it still applies today. Let’s listen to the skeptics.

According to many, this time is different because the economy is still humming and rates are still low. They tell us to pay special attention to the low overall level of the yield curve. So long as rates are sub-3%, they say, an inversion is no cause for alarm. Some say that pessimists are looking at the wrong term spread indicator. Others claim that negative term premia are a positive differentiator. Still others, looking for “special” reasons why the yield curve is flattening, point to QE or global turmoil or big bond purchases by insurance companies. The Fed, meanwhile, wants to distract the pessimists by directing their attention to a new, shorter-term recession bellwether.

Whew! Let’s respond in order.

The economy is still growing. This was a better argument last summer when we first responded to the critics. Today, with both domestic and global GDP growth slowing and with earnings decelerating, it’s no longer as persuasive. But, in any case, the current state of the economy is really beside the point. By the time you’re certain that that the economy is tanking, you have already lost in the marketplace. That’s the whole reason why investors look for leading recession indicators. (We’ll say more below about the timing of market tops versus recession starts.)

Rates are still low. Is it relevant that rates are generally lower today than in past business cycles? Probably not. Analysts at the San Francisco Fed specifically examined this question. They found that it’s only the difference between short and long interest rates—not the level of the rates themselves—that matters for recession and GDP forecasts. Refer back to Chart 4: Any time a yield curve inversion occurs, whether rates are at 5% or 9% or 15%, it is followed by a recession. In 1956, in the inversion that preceded the 1957-58 “Sputnik” recession, short-term Treasuries shot past 20-year governments at only 3.3%. That’s not much higher than we are today.

Many plausible reasons can be (and have been) adduced to explain the generally lower level of interest rates during the current expansion. Heading the list would be lower inflation and inflation expectations. Other reasons might include a greater supply or a lower demand for global savings, driven perhaps by demographic aging, slower productivity growth, or technological change. (See “Demography, Economic Growth, and Long-Term Real Interest Rates.”) But it’s not clear how any of these forces would affect the relative yield-curve dynamics of the business cycle.

The wrong term spread. In a March note, Goldman Sachs researchers said that the recent 10Y-3M inversion pointed to a “curve inversion signal” that “could be less powerful” than a 10Y-2Y inversion. They implied that whereas the Fed prefers the 3-month comparison (probably because it understands the research), markets prefer the 2-year comparison.

GS correctly points out that it is unusual for the 3M to invert before the 2Y. The yield curve is ordinarily monotonic—so that, by the time the 3 month inverts, all the longer durations have already inverted. Of course, that’s why the 3 month spread is a more powerful forecasting tool: By inverting later, it tends to avoid false positives. Yes, you could say that today’s unusual yield curve suggests an atypically weak inversion, since the 2Y, 5Y, and 7Y maturities are all beneath the 10Y. But you could equally say that it suggests an atypically strong inversion, since the 2Y, 5Y, and 7Y maturities are all beneath the 3M.

Negative term premia. Other skeptics are pointing specifically to the anomalous plunge over the past two years in the so-called “term premium.” This difficult-to-measure entity (it can only be estimated by surveys, not through market prices) suggests that 10Y yields are now very low in comparison to investor estimates of future short-term yields. According to the popular New York Fed measure, the 10Y term premium is currently around minus 80 basis points. This means that investors are accepting 0.80% less on their 10Y yield than they are expecting on the future rollovers of 30D T-bills. Yes, this is weird: Term premia should normally be positive.

So what’s going on? Hard to say. It could be that the New York Fed measure is inaccurate. (There are competitors; here is one that generates a less exceptional number.) Or, if it is accurate, it could be reflecting any number of forces long known to reduce the risk premium. For example, the historical risk premia series tends to rise when inflation expectations are high and variable. Lately, inflation expectations have been low and stable. On the other hand, risk premia tend to fall late in the business cycle when credit spreads are narrowing, bonds become attractive as a risk-parity hedge, and the odds of interest rate declines are rising (more on that later). Guess what? We are indeed late in the business cycle.

Whatever may be causing negative risk premia, one wonders how we should interpret its significance. In their historical analysis of term inversions, the San Francisco Fed analysts wondered the same thing. After splitting up long-term yields into “term premium” and “expected future short-term rate” components, they found that neither component mattered more than the other in their forecasting models—it was the overall term spread that mattered as a predictor. In other words, it doesn’t matter why the term spread is falling, only that it is falling.

QE, insurance demand, and global turmoil. The skeptics won’t buy this explanation. They think today’s negative term premia point to market conditions that are historically anomalous. They say that long bonds are getting starved on the supply side by years of Fed QE and are getting overwhelmed on the demand side by worried global investors looking for a safe haven and glutted pension and insurance plans forced to match assets to liabilities. The implication is that, once this transient market imbalance expires, long-term yields will surge, and the risk of inversion will disappear.

My response would be: OK, let’s say all of these things are historically unprecedented. Is there any strong reason to believe that any of them will be weaker a year from now than they are today?

Let’s start with QE. Looking ahead twelve months, we are clearly on track to see more QE, not less. That’s because the Fed is currently engaged in net quantitative tightening (net selling of long-term debt), which is scheduled to stop in September and turn strongly the other way in CY 2020. Ditto for the other two items. Is their any reason to believe that insurers will soon demand fewer liability-matching bonds—especially at a time when long-term yields seem to be trending down. Or to believe that global markets will soon become miraculously tranquil?

A new Fed bellwether. Even as some eminent leaders within the Fed acknowledge the yield curve’s impressive track record, others have tried to brush aside its significance. Last summer, the Fed floated to the media that their researchers had discovered a new term-spread recession indicator that works even better than comparing short-term with long-term yields. They called it “the near-term forward spread.” Basically, you take the current 3-month yield and subtract the forward 3-month yield 6 quarters (or 18 months) in the future.

It’s hard to know what to make of this new indicator. The Fed believes it’s a “purer” measure of the difference between current and future interest-rate expectations. Yet at the same time, since it just compares current with future estimates of short-term rates, this near-term forward spread is basically just the market’s perception of upcoming Fed policy. Wrap your mind around this: The Fed is suggesting, as an alternative to the standard term spread, that the market instead watch its own expectation of what the Fed is about to do. Hmmm, yes, that’s a head scratcher.

What the Fed really liked about its new indicator was that—last summer—it did not show any declining trend over time. So unlike the standard term-spread measure, the new Fed indicator did not point to any impending economic slowdown. Why? Because, back then, the market believed the Fed would continue to raise rates in future quarters.

Ten months later, expectations have changed. Now the market believes the Fed will cut rates in the future. Now the new Fed indicator is flashing the same recession-ahead red light as all the other term-spread measures. Oops! I think it’s safe to say that we won’t be hearing much more from the Fed about its new discovery any time soon.

SO WHAT HAPPENS NOW?

Let’s assume, as now seems likely, that the yield curve definitively inverts sometime in June. The natural question to ask is: Will this time be different? And, if so, why?

Let’s look first at Fed policy, starting with its control of the near end of the yield curve. Could the Fed actively intervene to pull down the near end? Could this effectively “de-invert” the yield curve and thus stop the flashing red light. More importantly, could this simulate the economy and thus avert the danger that is triggering the red light?

Arguably, the Fed has already been trying to pull down the near end. On May 1, the Fed cut its interest rate on excess bank reserves from 2.40 to 2.35. The reason, it said, was to try to nudge the daily effective fed funds rate away from the upper end of its current range (2.25-2.50%)—as though this were just some sort of technical adjustment. The real reason, I think, was that the Fed was trying to nudge down the 3-month bill to avoid an inversion. The policy worked. The 3-month yield declined. Unfortunately for the Fed, the 10-year dropped a lot more.

So at this point, if the Fed wants to de-invert the curve, it’s going to have to do something a lot bolder. It’s going to have to formally and officially start cutting its rate bands.

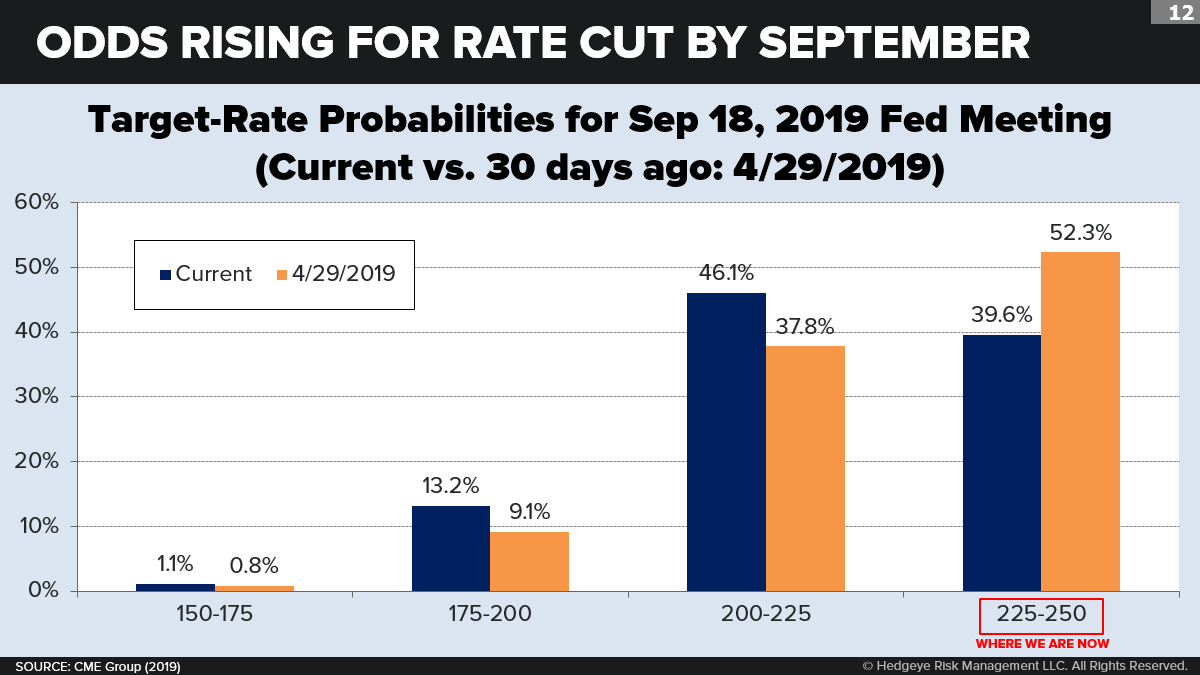

And, as it turns out, that’s just what the market now expects. According to fed funds futures prices, the implied probability that the Fed will cut by its June 19 meeting is 10%; by its July 31 meeting, 25%; by its September 18 meeting, just over 50%; and by its December 11 meeting, over 80%. By the end of 2019, the odds are 41% that the Fed will cut rates at least twice. And 11% that the Fed will cut rates at least three times. The odds the Fed will raise rates at any time over the coming year is now zero.

Compared to the expectation of ongoing fed funds hikes that prevailed through most of 2015 to 2018, most of the big outlook reversal occurred in December of 2018, when the Christmas season market crash and slowing global indicators persuaded the market that the hiking agenda was probably off the table. But a second big dovish hit to expectations came in the last week of March, exactly when the market was digesting the first 6-day dip into inversion. This week, with the yield curve again inverting, rate-cut odds are again rising.

So even if Fed Chairman Jerome Powell and most of the FOMC members still don’t see a “compelling” case for a rate cut, the markets believe that the Fed will indeed cut rates. Maybe not in the next meeting or two. But certainly by the fall.

Let’s try for a moment to read the Fed’s collective mind. If the market already thinks it is going to cut rates, why doesn’t the Fed go ahead and do it now? Why don’t the FOMC members just agree with President Trump, roll up their sleeves, pick up their axes, and start chopping?

Here’s why. The Fed is aware that every policy change it makes has two effects. The first effect is objective. It is to change a market price (like the fed funds rate) and thereby change the future speed and direction of the “real” economy (like employment, real output, and inflation). The second effect is subjective. It is to change what the market believes about what the Fed believes is the outlook for the economy. And because the market knows that the Fed spends enormous resources on economic forecasting, the Feds’ policy change will hugely affect the market’s perception of the economy’s current speed and direction.

I think now you begin to see the problem.

By cutting rates quickly and aggressively, yes, the Fed will gradually stimulate the economy relative to where it is heading now. Let me emphasize the word gradually. Most economists believe that interest rate changes require 9 months to start impacting the economy perceptibly—and up to 2 years to become fully effective.

But at the same time, rapid and aggressive rate cuts will change the market’s view of where the economy is now. And that change will be negative and immediate. Keep in mind that Powell along with other Fed committee members have until quite recently been reassuring the public that the economic outlook is “still positive” and that they continue to “anticipate moderate growth.” Just three weeks ago, Powell said the Fed continues to be vigilant about rising core inflation.

Sudden easing would not just be a loss of face for the Fed. (The FOMC just raised rates five months ago.) It would also signal to the markets that, all the recent balmy press releases to the contrary, the Fed now sees storm clouds on the horizon, very possibly a recession. That perception shift will figure instantly into the hiring and capex choices of business CEOs and into the portfolio choices of investors—long before the economic impact of a lower fed funds rate will even begin to register. Think especially of our earlier discussion of the speculative impact on bond markets. Now, in an instant, there will be a lot more money betting on the long end in the hope that the whole curve will soon fall.

Upshot: An abrupt Fed cut to the short end could end up lowering the long end as well. In that case, not only would the Fed fail to stimulate the economy, it would not even change the color or sign of the recession indicator.

So why are the markets convinced the Fed will be cutting rates later this year? I think the markets believe that slowing economic indicators will eventually leave the Fed with no other choice. By late this summer or this fall, as more people become persuaded that the economy may be in trouble, the Fed will no longer be changing perceptions by cutting rates. By then, in fact, it may be catching up to perceptions.

Until now, I’ve been assuming that lowering the near-end of the curve (by cutting the fed funds rate) is the only way the Fed could de-invert the curve. No, it’s not. But it is the most direct lever, and I doubt that any of the others are under serious consideration.

In theory, the Fed could try instead to raise the long end. Hey, we now live in the era of QE and QT, which means just about anything is possible. This would require the Fed to sell-off the long-term Treasuries on its balance sheet faster—in effect, intensifying its current QT regime. In fact, the Fed is currently planning to do just the opposite. It intends to stop its QT effort in September and move back to a much heavier schedule of net Treasury purchases next year.

Realistically, I don’t think the Fed will change these plans. After all the effort it has spent trying to control the long end—that is, keep it low—the Fed would suffer an enormous loss of credibility if it tried to trigger a bear market in Treasuries. What it might do, however, is announce (say) a “delay” in the end of QT for various technical reasons.

The Fed could also in theory try to reshape the yield curve by some sort of twist—or rather “untwist”—operation. Even if the Fed keeps its total balance-sheet targets unchanged, let’s say it starts buying only the on short end and starts selling only on the long end. It would probably help to have U.S. Treasury Secretary Steve Mnuchin on board with this strategy. But thus far Mnuchin is not letting on that he’s any more interested in the shape of the yield curve that Fed Chairman Powell.

To summarize: The Fed may not have many options left except just whistle past the graveyard and hope that all the worry somehow just fades away. You never know: Maybe this time will be different. But keep in mind that all this whistling does not necessarily mean that the Fed presidents and board members aren’t worried about the yield curve inversion. It just means that, if they are worried, they don’t dare let the public or the markets know they’re worried.

Sure, bulls might argue that there have been exceptions. What about that time in 1966-67, when the curve inverted for 6 months and Fed Chairman Martin managed to avoid GDP going negative? Or what about 1995-96, when the yield curve narrowed sharply (though never inverted) and Fed Chairman Greenspan similarly managed to avoid a recession. Isn’t a soft landing still possible?

Maybe. But two facts about these these exceptional cases are worth pointing out.

First, they both required decisive and substantial rate-cutting by the Fed (amounting to 200 bp in 1966-67 and 80 bp in 1995-96. If the Fed wants to follow that example in 2019-20, that means—at the very least—it will have to risk loss of face and start ratcheting down those fed funds bands. Tweaking around the edges is unlikely to work.

Second, they both occurred roughly midway through an economic recovery. In terms of consumer sentiment, credit spreads, and employment, for example, it was clear that the economy still had ample room to run before reaching its peak potential. Today, I don’t see the same room to run. Since Q2 of 2018, the economy has been running above potential (like 1966 but unlike 1995). Since October of 2018, the age-adjusted employment-to-population ratio has exceeded its previous cyclical peak in 2007. (see: “Howe: Unemployment At 20-Year Low. What’s Next?”) If you think it still can rise a lot higher, sure, go ahead and place your bet. Personally, I’m dubious.

BE CAREFUL OUT THERE

For equity investors, this means the path ahead becomes treacherous. A recent BMO Capital Markets analysis shows that stocks can still perform well in the flattening phase of the yield curve. But once the curve turns negative, things get a lot riskier. If you look at the seven inversions since 1968 (according to one count), the S&P 500 had already reached its pre-recession peak before three of the inversions had even started. When the curve fully inverts, the safest—indeed, the most profitable—place to be is in long bonds. And you want to start battening down the hatches on everything else.

Again, I know, there’s always a temptation to suppose that this time is different.

So to conclude on a cautionary note, let me quote from Chairman Greenspan, el maestro himself, as he sat before the Joint Economic Committee just before Christmas in 2005. Asked to comment on the recent narrowing of the term spread, Greenspan reassured the committee that the statistics underlying the inversion indicator “were weak” and added that, overall, “the yield curve has lost its ability to forecast recessions.”

Less than a month later, the 3M-10Y spread started to invert—skipping the water every few weeks. On July 19, 2006, it fully inverted, meaning the stone sank for good. And by December of the next year… well, we all know what happened then.