The guest commentary below was written by Jesse Felder. He recently joined us on our "In The Arena" podcast. Click here to listen.

Back in March of 2009, within days of the bear market low, I shared a chart that highlighted a very interesting long-term Fibonacci support level.

That chart is recreated below and it shows that the S&P 500 bottomed almost exactly at the 61.8% Fibonacci retracement of the bull market gains that began in 1982.

Obviously, this proved to be a very durable low as stocks went on to gain more than 300% over the following decade.

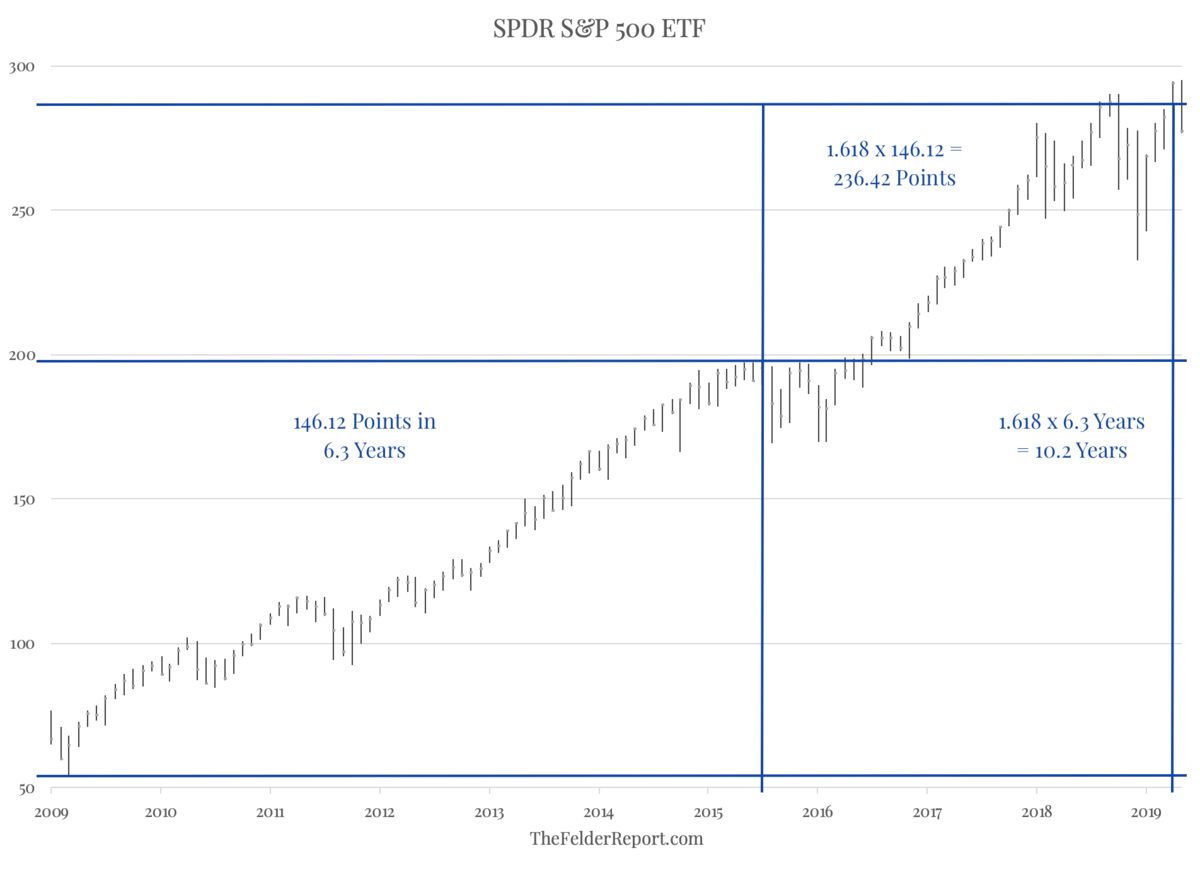

Just over a year ago I shared another chart that highlighted yet another long-term Fibonacci level that could prove to be equally important.

Below is an updated version of that chart and it shows the S&P 500 SPDR ETF struggling to overcome the 1.618 Fibonacci price extension of its gains from 2009-2015. I have also added the 1.618 Fibonacci time extension, as well, which comes into play right about now.

Just as that earlier Fibonacci level marked an important turning point for the broad equity market, this current one could do so, as well. Time will tell.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Jesse Felder and reposted from The Felder Report blog. Felder has been managing money for over 20 years. He began his professional career at Bear, Stearns & Co. and later co-founded a multi-billion-dollar hedge fund firm headquartered in Santa Monica, California. Today he lives in Bend, Oregon and publishes The Felder Report. This piece does not necessarily reflect the opinion of Hedgeye.