The guest commentary below was written by Christopher Whalen.

In May of last year, we suggested that it may be time for Elon Musk to declare victory and sell Tesla Motors (TSLA) to one of the top global auto manufacturers.

A year later, we watch as the likes of Audi AG and Daimler AG hammer away with advertising in new and old media displaying well-executed electric car offerings. Owing to a shortage of operating cash, TSLA has no response in terms of advertising message and no retail sales network either. Under the leadership of Elon Musk, TSLA operates in extremis for all to see.

As we wrote in “Ford Men: From Inspiration to Enterprise,” the global auto industry is a scary proposition for even the largest and most efficient operators. TSLA has neither scale nor sufficient funding to make let alone even market its products adequately. Adequate funding, to recall the wisdom of our friend Bill Janeway, provides the opportunity to properly plan and execute a business strategy.

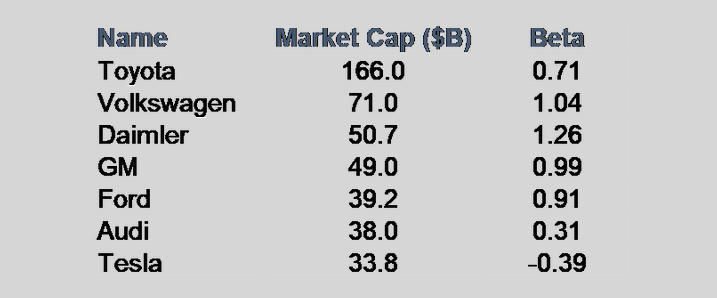

Notice the negative market beta for TSLA in the table above c/o CapIQ. To us, Elon Musk is a really smart man who needs an exit strategy. We like to say that hope takes a stock price up, but credit concerns bring stocks down. Right now credit concerns are predominating with TSLA as it becomes clear that the company cannot spend its way to profitability. Like Uber Technologies (UBER) and so many new age ventures hatched during the irrational era of negative interest rates, TSLA’s continued existence is predicated on access to new investor cash needed to finance operating losses.

There does not seem to be any possibility that TSLA can grow to sufficient size and profitability to contend with the global incumbents led by giants such as Toyota Motor and Volkswagen AG. The TSLA common is now down about 30% over the past year, a reflection of the bad boy behavior of Musk and the now explicit need for new cash -- this after months of denying that any such need existed. Indeed, TSLA's price is about where it was five years ago.

When Henry Ford started to display truly idiosyncratic behavior in the 1920s and 1930s, Ford Motor was private and protected by a gang of thugs led by the infamous pugilist Harry Bennett. The company was run like a plantation, bills were paid in cash, and Ford Motor Co had no net debt. Economists and writers could make fun of Henry Ford’s increasingly bizarre public conduct and monolithic product offering, but the company was not subject to a daily auction as is the case with TSLA’s stock and debt.

Despite efforts by TSLA’s board and lawyers to control Musk’s obfuscation, he continues to paint a hopeful image of the future that seems difficult to square with reality described in his public disclosure. In the April 2019 TSLA conference call, Musk stated:

|

“We are the only Company in the world producing our own vehicles and batteries, as well as our own in-house chip for full self-driving. We're in a position unlike anyone else in the industry. And in 2020, we expect to have 1 million robotaxis on the road with the hardware necessary for full self-driving. We believe we'll have the most profitable autonomous taxi on the market and perhaps the -- yeah…. In Q1, Model 3 was yet again the best-selling premium car in the US, outselling the runner-up by almost 60%.” |

Due to the reluctance of mainstream auto insurers to cover the TSLA cars equipped with the wondrous self-driving feature, Musk announced during the April conference call that the company would launch its own insurer. Adam Jonas of Morgan Stanley asked Musk why he did not take TSLA private given the “alternative capital and large amounts of strategic capital that is incrementally deployed in domains where Tesla has real leadership.” Good question.

Musk’s reply: “I would prefer we were private, but unfortunately, I think that ship has sailed, so... Well, I mean, being public, does feels like the sort of price of the stock is being set in kind of a manic-depressive way. And I think Warren Buffett's analogy is just like perhaps being a publicly traded company is like having someone stand at the edge of your home and just randomly yell different prices for your house every day. It's still the same house.”

Well, maybe. The house Musk describes in his inflated public statements bears little resemblance to the TSLA that has debt trading at a 20% discount to par. Sadly the ship may have indeed sailed for Musk in terms of obtaining new funds or even selling the company to a larger premium marque like Daimler or Audi. When Musk himself conceded during the April conference call that “I think there is merit to the idea of raising capital at this point,” he stated the obvious.

A couple of days later on May 2, Musk told investors that he was planning to raise $2 billion in capital through new common equity and convertible notes. The move came after literally months of rejecting the idea of new share issuance, including during the April 2019 conference call with investors.

“I don’t think raising capital should be a substitute for making the company operate more effectively,” Musk told shareholders on the company’s quarterly conference call, reports CNBC. “I do think there is some merit to raising capital, but this is sort of probably about the right timing.”

Sort of probably? It is remarkable to us that the Securities and Exchange Commission gets visibly upset about Musk’s use of Twitter for his public dissembling, for example, yet ignores the seemingly clear manipulation of investors via selective and conflicting statements regarding a future offering of securities. But those poor helpless investors do seem to have figured out the basics since the announcement of the offering several weeks ago and have pushed down the price of TSLA sharply to close at $190 on Friday.

Notice that Ford Motor just announced the layoff of 10% of all salaried workers as part of the latest restructuring at the Blue Oval. Renault and Fiat Chrysler are discussing a merger, this in the wake of the palace coup launched against Carlos Ghosn by his former colleagues at Nissan. This is bad news for Nissan, of course, who must now merge with another Japanese automaker since they apparently cannot abide the idea of union with a foreign company. None of these discussions, mind you, are driven by the potential for growth in the global auto industry. Instead the imperative is to cut costs in a stagnant commodity industry that suffers from chronic overcapacity and low or no profits.

A number of former supporters of TSLA have abandoned Musk since the April conference call. “Morgan Stanley threw the biggest blow, declaring that in a worst-case scenario, Tesla’s shares could sink to a shocking $10,” Bloomberg reports. “A Wedbush analyst said the carmaker is facing a “code red situation” and cast doubt on whether Tesla can sell enough of its electric cars to make a profit. And Citigroup and Robert W. Baird & Co. analysts, among others, slashed their target prices, citing concerns about cash flow and consumer demand.”

We still think that Elon Musk can salvage his reputation and value for his shareholders by selling TSLA to a global manufacturing company that makes premium cars. Audi, Daimler, Honda and Toyota are all obvious suitors. And TSLA is already cooperating with Fiat Chrysler Automobiles to help reduce the Italian-US firm’s liability for emissions in the EU. Just imagine Fiat-Chrysler, Renault and Tesla under a single roof.

As part of the equity offering, TSLA will no doubt receive inquiries about an acquisition from several global automakers in Europe and Japan. As we noted last year, Musk has validated the idea of electric vehicles and has also created a very valuable brand. But can this accomplished business man and technologist admit that his brilliance is wasted on making mere automobiles? We’re thinking more of the Jetsons. Flying car to LGA please Mr. Musk.

A century ago, Ford, GM and other US makers could not manufacture cars fast enough to meet demand. Today the name of the game in the shrinking auto industry is alliances and consolidation. Given that large Sell Side firms like Morgan Stanley have decided to throw TSLA under the bus, maybe it’s time to think about a sale?

Even a valuation near Friday’s close for TSLA would be a gift compared with the worst case scenarios making the rounds on the Street. As and when the question is asked about acquiring TSLA, will Elon Musk be smart enough to take the call? For the sake of TSLA holders, we certainly hope that the answer is yes.

EDITOR'S NOTE

Christopher Whalen is Chairman of Whalen Global Advisors LLC. He has worked in politics, at the Federal Reserve Bank of New York and as an investment banker for more than 30 years. He is the author of three books Inflated (2010), Financial Stability (2014) and Ford Men (2017).

In 2017, he resumed publication of The Institutional Risk Analyst and contributes to many other publications and media outlets. He recently launched the first volume of The IRA Bank Book, a review of the operating and credit performance of the US banking industry written for institutional investors.