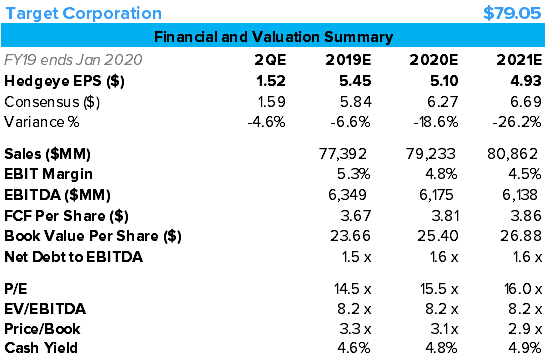

Can’t take anything away from TGT on this print. Clean quarter, though slowing on the margin, $0.10 beat, guidance maintained. Gross margin was the only line that actually surprised us to the upside, positive given the inventory improvement. Cash flow from ops down 37% is strange on up EBIT and cleaner inventories, driven by a big payables change. The thing I struggle with is that a glaring theme this quarter so far has been the lack of earnings flow through for the companies that are comping. How is it that TGT is bucking that trend? It’s facing the toughest headwinds via labor inflation and an all-out next-day delivery war between AMZN and WMT, and yet it’s the only company that puts up an outsized EBIT growth rate of 9% with EPS growth of 15%. I struggle to see how it can still comp for the balance of the year without investing more heavily in SG&A – especially when ~2/3 of the 3.3% SG&A growth rate is covering higher labor costs as it follows AMZN to $15 per hr. If SG&A grew where it should have – this would have been an in-line quarter. With the stock rallying on this beat, I think the market is in the Cornell camp that the company can gain share of wallet at a 6% EBIT margin – something that I think is unsustainable. Costs and investments need to ramp at TGT to grow – either way numbers for the balance of the year and 2020 are at risk. We’re 6.6% below for the year, and then 20% below over a TAIL duration. Best Idea Short, with higher confidence on today’s price action.

Guidance and Outlook – Jeremy McLean

Full year guidance was held, as we expected. The only real change in our model on this print is getting more bullish on gross margin. Inventories are cleaner, the 1Q result is better than we expected, and commentary sounds bullish. Still we see a decline of ~20bps, but thought previously that we could see something in the range of a 30-40bps decline. The company may stave off some e-commerce dilution this year, but we’re confident that remains a long term margin drag. We’re taking SG&A and sales up slightly with 1Q result coming ahead of our expectation on each.

Guidance for the year, as we see it, is all about the comp, and the company is guiding “low to mid-single digits”. By our math TGT needs about a 4% comp to hit earnings numbers. Given the comparison set-up, our macro view of slowing US GDP and the slowing consumer, and the toy tailwind evaporating, we think 4% comps are not achievable without sacrificing margins.

On 2Q specifically, we struggle to get to the mid-point of guidance. The line that is dragging us down is most likely comps, but we’re modeling a clear 2 and 3 year comp improvement at 2.7%, as management said 2Q should slow. So why should we expect something greater? More detail below.

Comps

The company acknowledged that we are soon lapping help in baby/toys as Toys R Us stores closed by July last year. Toy and Baby continues to be called out as an outperformer so we think this is a real headwind. So what drives sales strength from here to hit numbers? Perhaps its store remodels with TGT remodeling 300 stores this year, 53 done in 1Q. The remodels seem to have been successful in driving traffic over the last year or so, but the traffic compares are very difficult now.

SG&A

TGT’s minimum wage is going to $13 min next month. That’s about 150bps of incremental SG&A growth pressure. 1Q growth was actually greater than we expected, and that was with marketing expense timing help and cost efficiencies in tech operations. If the company wants to sustain comps, we’d expect to see greater spend towards tech/marketing. Perhaps that’s a risk for 2H comps.

Mixed Messaging

Commentary from CEO Brian Cornell still often perplexes us. Today in prepared remarks he described some early quarter choppiness. When asked to elaborate in Q/A, he seemed unwillingly to acknowledge his prior comment saying “We saw very consistent performance throughout the quarter” using the word consistent 4 times in the answer.

The other answer that struck us as odd was when asked to comment on competitive environment given inventory conditions for others in the space. He answered by saying “we're seeing a very consistent and healthy environment across the U.S.” and the market is just seeing winners and losers. That’s fine, and he is right to a certain extent, but it would give more confidence if he could share where TGT is winning best, and why they are winning. Retail results in 1Q are screaming that it's not the same environment as last summer, and it’s concerning if TGT is not aware of that.