If you were wondering why KSS issued warrants mid quarter to AMZN – its greatest existential threat -- for the right to accept Amazon returns in its stores…OR if you were wondering why KSS looked at buying HOME and diversifying egregiously out of its core – now you know. This quarter and guidance – and the overall state of KSS’ business -- is an absolute disaster.

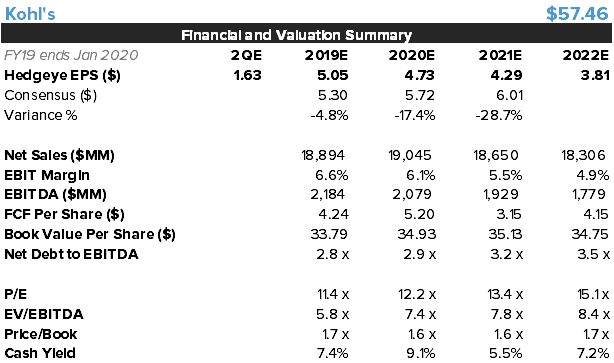

KSS missed comp by 330bps – comping down 3.4% (500bps slowdown on the 2-year) and missed the headline by $0.07 with 5 cents help from a lower tax rate. Management is taking the full year down $0.75 or 13%, only about 2.5 months after setting the original expectation. We can understand 1Q being weak, but why should the full year outlook have changed so materially? KSS is signaling that something is very different vs a quarter ago, something we expect TGT will express in its numbers within the next 4 months. People like KSS for its FCF yield, well CFFO was down $250mm, or -65%. That’s retail. The interesting part is that with the weakness this quarter, credit was still solid with other income up 4.3%. I think credit will be another shoe to drop later this year. I said it before and I’ll say it again…the consensus expectation for KSS to ever earn over $6 is a pipe dream. Back half numbers are predicated on an acceleration from Amazon – something that management went out of its way to give ZERO financial context or color about. I don’t think it was being evasive – I think management simply doesn’t know.

I almost never queue in to a ask a question in Q&A, but this time I did. Didn’t get called on, which is not a shocker. Not exactly KSS' practice to give the most vocal short air time. But my question is this... 'IF the KSS partnership drives traffic to your stores in 2H as you plan, what's stopping every other traffic-starved retailer from JCP to BBBY to PIR and even quality names like TJX and WBA from doing the same thing in 2020? And WHEN that happens, what will your competitive response be?' I’d pay money to hear the answer to that question.

Here's the link to our Black Book when we elevated KSS to our top short on April 29th at $72.

KSS | Here's Why The AMZN Deal Won't Work CLICK HERE

Guidance and Our Outlook – Jeremy McLean

Who would have thought a month ago that KSS would hit 1.5yr lows by Memorial Day. Exactly six months after Fortune declared that KSS had ‘cracked the retail code,’ the company shows it has almost no handle on its business.

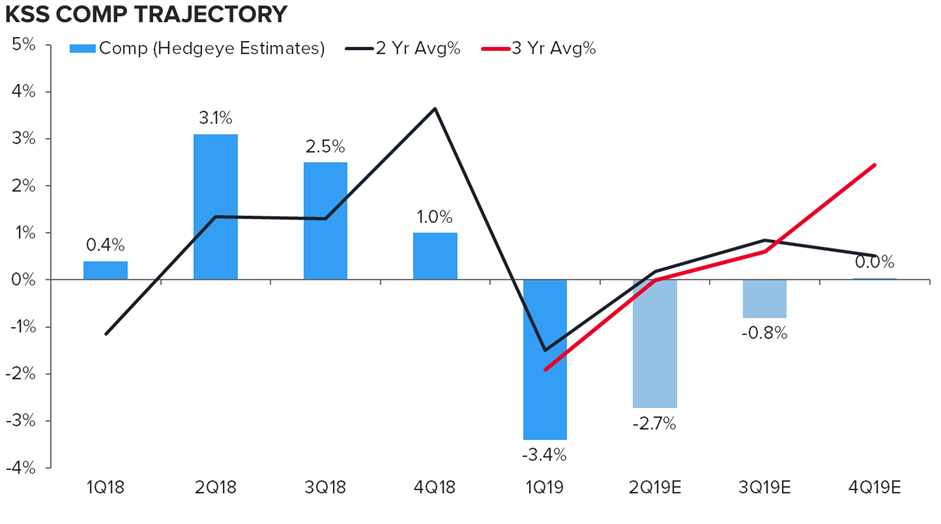

The company has rebased numbers materially, with the 13% EPS guide down it’s basically down to where our model was, and is now saying comps flat to down slightly. But the commentary implies a ramp throughout the year. That implies a drastically improving 3 year comp. Our expectations are shown on the chart below, and that gets us to a -1.5% comp for the year (a miss). The company is stating brand initiatives and Amazon as the driver of the acceleration, yet it is also taking down gross margin expectations as it intends to promote to maintain share. So maybe it can discount to drive comp in 2H, regardless of the success of Amazon and new brand launches, but that will mean some incremental gross margin risk. Gross margin was also revised partially due to tariffs. Perhaps it was poor risk management to not bake 25% into the plan before, or its just convenient to blame Trump for a bad margin guide 2.5 months ago.

Additionally there is extra SG&A (~50-100bps of growth) going into the plan for executing Amazon returns, despite the fact we repeatedly heard that the company was planning to do the returns without any extra people/logistics costs. Given the weakness in comp in 1Q, the weak start in 2Q (implied from the guide), the difficult compares, our macro view of a slowing US consumer, and our expectation that Amazon returns comp help will be underwhelming, we are modeling a comp driven earnings miss for the remainder of the year.

Amazon

A couple notable callouts from this quarter as it relates to the Amazon initiative. First, the company acknowledged it will spend more to execute it, which wasn’t the consensus coming out of the going nationwide announcement. The guidance of an implied 50 to 100bps of SG&A growth is actually in line with our base case from our quantification of the Amazon impact. Second, the company is making it clear that the initiative was driving traffic in the tests. However, it seems much less clear about how much sales the initiative will drive. Perhaps management doesn’t want to say it to deter other entrants into the Amazon return market. However, we think the company legitimately struggles with how much incremental sales it would drive nationally, and whether that sales amount was worth the cost/investment.

Sales vs Inventory Management

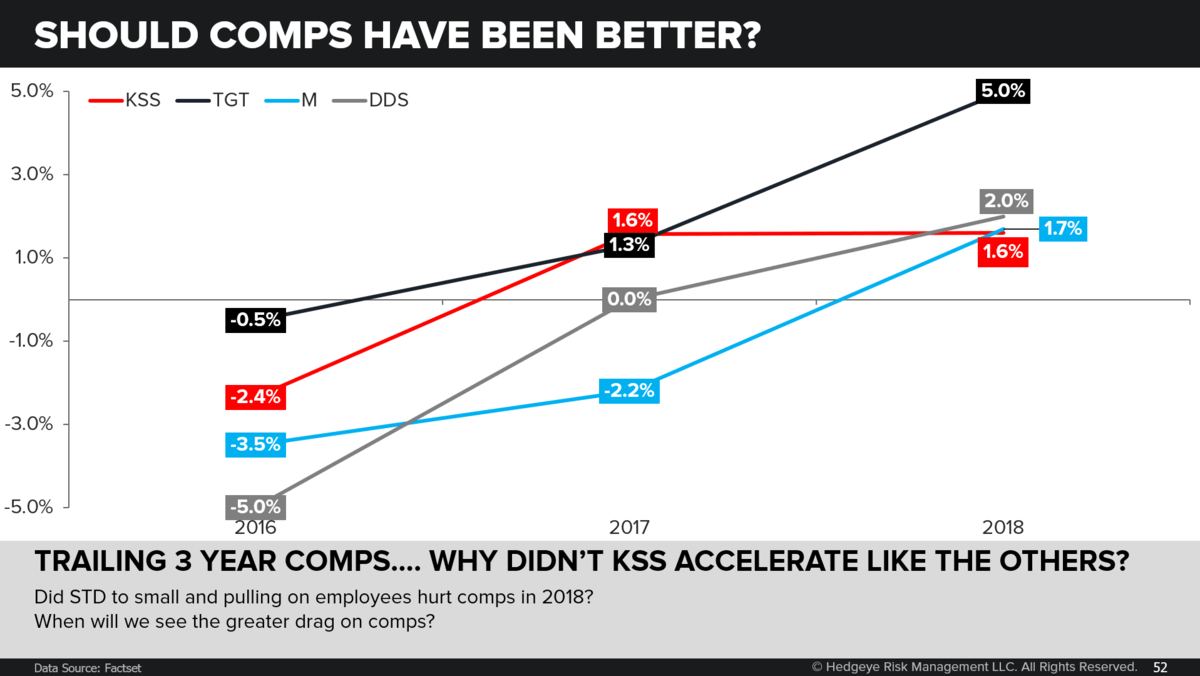

This quarter the company admitted that inventory management may have hurt sales with fall product being in higher demand, but not as well stocked. In our black book last month, we question whether standard to small and employee reductions have been hurting sales for several quarters. It just didn’t seem important since comps were positive. Reducing inventory and service levels has to be some kind of drag on comps. Note that last year we did not see KSS accelerate sales growth similarly to peers (chart below). Now that the selling environment has weakened, we think we are seeing the comp drag on those initiatives created. Keep in mind the company said the Midwest was aided by competitor departures this Q, something that likely was a help nearly all of last year.

Credit

The company said nothing about credit earnings this Q. Other revenue was up 4.3% YY implying credit EBIT grew. Shared EBIT from the company’s credit portfolio with COF represents ~35% of EBIT and 42% of EPS, yet it gets no attention on the call. We think we are at an inflection point for the credit portfolio as delinquency rates at COF and SYF get weaker on the margin, and senior loan officers signal continued tightening in credit card lending standards. KSS will surely be pushing the credit card hard to any incremental shopper that enters the store for an Amazon return. Maybe that means growing the customer/cardholder base slightly after 5 years of gradual decline, but we don’t think that will be enough to offset the bad debt risk when the economy goes from peak sentiment and trough unemployment to something worse in the coming 12 months.

Athletic/Active

Active grew MSD, similar to last quarter, and much lower than the 15-30% growth rates we were seeing a about a year and a half ago. Perhaps this comp driver is running out of steam, as this is the first time we’ve heard KSS sound bearish on Nike & UnderArmour (notably in footwear) saying “we were kind of lapping some newness from some of our key brand partners, like Nike and Under Armour, so we're a little softer in the first quarter.” The company was bullish on Adidas growth near term. If active is running at only a MSD comp, at 20% of the store that means only ~100bps of comp, while the rest of the store obviously remains significantly pressured. Re-accelerating this category will be a key for KSS to get back to positive comps.

Digital

Digital slowed to HSD growth, the lowest ever reported for KSS, unimpressive to say the least. We previously called out an issue with the Kohl’s App update that happened intra-quarter, but the company told us this was not impacting a material portion of customers, and was fixed relatively quickly. It was also not called out on the call, so we'll assume it was not a one-time contributor. This quarter was the toughest digital comp of the year for KSS (up 19% 1Q18) so we expect growth in digital could get slightly better for the remainder of the year.