As we look at the macroeconomic environment ahead what’s certain is that investor fears associated with sovereign debt default (globally) will persist. Greece, a poster child of years of government budget mismanagement and excesses, has been the obsession of the media, yet even countries with historically top credit ratings (US, UK, and Japan) are beginning to feel the spotlight as they too are among the proverbial debt bloated “PIIGS”. We’d point you to Reinhart and Rogoff’s book “This Time is Different”, for a thorough analysis of eight centuries of global sovereign default, and note that the current cycle of sovereign default is just ramping up, and we believe will last far longer than most expect. What’s clear is that certain countries are “sitting” better than others from a fiscal balance sheet perspective, countries we’d also expect to outperform their deeper debt-laden peers as we look out to 2010, a theme we’ve named the Sovereign Debt Dichotomy.

With this dichotomy to play out across asset classes, in summation we’ve positioned ourselves in our model portfolio to take advantage of owning High Grade versus High Yield. We’ve represented this conviction through owning low beta sectors like Healthcare (XLV) to countries with more fiscally conservative balance sheets like Germany (EWG). Conversely we’ve shorted Municipal Bonds (MUB) and High Yield Corporate Bonds (HYG) - to take advantage of yields pushing higher as obligations mount- to shorting countries like Spain (EWP) with looming sovereign debt issues and glaring negative fundamentals that could stretch over the TAIL (3 years or less) duration. We’ve also seen carry-over to a weakness in the Euro versus the USD, which we’ve taken advantage of by shorting the Euro via the etf FXE.

As an example of our Sovereign Debt Dichotomy theme and the divergence of economic performance across countries, below we lay out our case for investing long in Germany and short in Spain.

GERMANY

Position: we initiated a long position in Germany via the etf EWG in our model portfolio on 4/7/10.

The anchor of our bullish case for Germany remains the fiscal conservatism of German Chancellor Angela Merkel and her government, and improving trends across fundamentals, especially exports.

Fiscal Conservatism

Germany’s budget deficit stands at 3.5% of GDP, a clear differentiating factor compared to the low double digit budget deficit figures witnessed in countries like Greece, Spain, Ireland, and the UK (chart). We see this as an extreme advantage, especially as the cost of capital looks to rise for European states over the medium term.

A recent example of Germany’s fiscal conservatism can be seen in Merkel’s initial decision to support a unilateral IMF-led campaign to aid Greece. Although the position was heavily chastised by the European community, it was really a pragmatic decision born out of her fiscally conservatism: not only did she not want to reach into German coffers to fund Greece’s debts, but also by suggesting that Greece continue to work to clean up its own “house” (budget deficit) before monies were placed on the table, Merkel attempted to not diminish the incentive of the Greek government to issue austerity measures to shave its imbalances.

As we now know, Europe has agreed to provide a three year €30 Billion loan to Greece at favorable rates (estimated at 5% or 200bps below current market prices for Greek debt) and the IMF guaranteed to kicked in an additional €15 Billion should Greece need (or request) the loan. In our opinion, we believe the loan is imminent. In any case, Germany’s position on Greece—which differed from her European colleagues such as French President Sarkozy and ECB President Trichet—is representative of a cultural aversion to debt, from personal consumption at the individual level up to spending at the governmental level. We believe it is this conservatism which will benefit the country’s growth prospects over this year and beyond.

First and foremost, the German economy offers competitive growth and safety. And as Germany differentiates itself from the sovereign debt crisis brewing across certain states in Europe, and globally, we believe Germany is in a favorable position as it will not have to sacrifice growth to correct a leveraged balance sheet (or default), as the credit market remains relatively stable despite Germany’s pending contribution to Greece. Below we offer some of the fundamentals we track that confirm an improving economic trend that we expect to continue.

Fundamental Strength

- Exports rose +5.1% in February month-over-month. The chart below shows an improving trend in exports, up +9.4% in February Y/Y, with favorable comparisons for the months ahead as global demand melts higher. Additionally, carry-over weakness in the Euro versus the USD should be a net positive for the export-led economy. We guide to trading the Euro between $1.33 - $1.35 with TREND (3 months or more) resistance at $1.39 and TAIL (3 years or less) resistance at $1.42.

- German Factory Orders rose +24.5% in Feb. Y/Y; while certainly a moonshot of a number, we note the comparison was off the trough a year earlier of -38.0%. January also saw a sizable annual improvement (+20.6%) versus -36.8% in Feb. ‘09. Orders are confirming an intermediate positive trend.

- A stable inflationary environment for consumers and producers continues with CPI at +1.1% in Mar. Y/Y and PPI at -1.5% in Mar. Y/Y. Additionally German Manufacturing and Services PMI surveys shows improvement over recent months.

- Unemployment currently stands at 8.0% and the unemployment rate has held steady for the last months. Despite the persistent fear of rising unemployment that we’re seeing across many European countries, the stability in the number has helped to boost consumer and business confidence; credit should be given to the successes of the short-term work agreements (Kurzarbeit) subsidized by Merkel’s government.

SPAIN

Position: we initiated a short position in Spain via the etf EWP on 4/9/10 and covered it on 4/21 for a trade. Our negative bias continues.

In contrast to Germany we see significant downside risk for Spain over the medium to longer term, including such structural and fundamental issues as: 1.) the aftermath of the housing bubble and high unemployment, 2.) the banking situation, especially its savings and loan banks, or Cajas, and 3.) its debt payment schedule ahead.

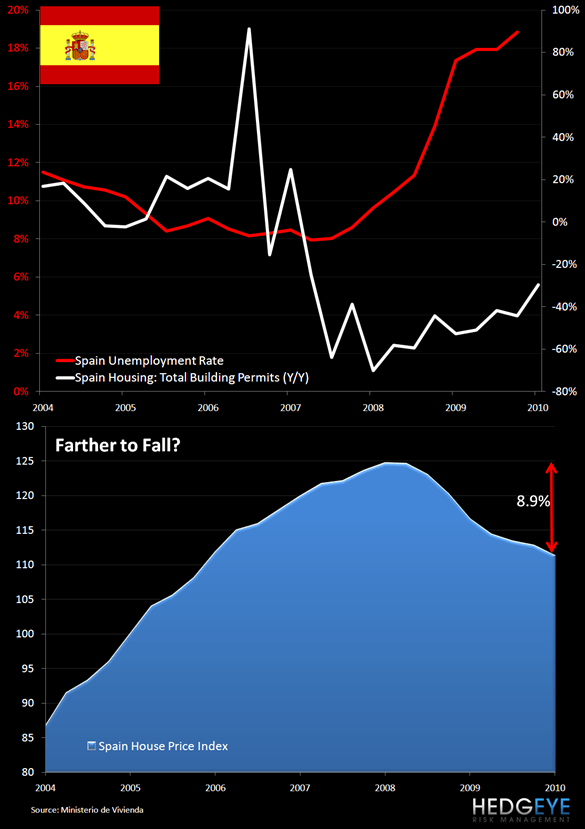

Housing: From Boom to Bust

Our bearish outlook on Spain is heavily underpinned by the structural weakness in the housing market and the rise in the country’s unemployment rate. With the bursting of a decade-long housing bubble beginning in 2007, Spain has lost a main driver of the country’s previous economic growth and sent many of the same people that were employed by the construction industry to fuel the housing boom into unemployment. At just shy of 20%, Spain’s unemployment rate alone is astronomical compared to the Eurozone average of 10%. The carry-over effects of a high unemployment rate (more generally) have and will lead to reduced government revenue and erosion of personal consumption, coupled with the severe wealth destruction caused by the depreciation of housing prices, are all factors we believe will provide a headwind to economic growth.

A recent report from Morgan Stanley suggests that housing prices have declined by 11% from their peak in 1Q08 and the construction sector is down 32% from its peak in 4Q07. Interestingly, the report cites that house prices fell some 20% peak to trough in the UK and -25% in Ireland, inferring that downside potential of another 10% from here remains, an assessment that we’d largely agree with. Further, it’s clear that inventory of unsold homes remains extraordinarily high. MS tags the number of unsold homes at 1.5 million (or half the number of homes built over the last 5 years) and Banco Santander notes that repossessed properties are currently selling at 20%- to-30% discount to market prices.

While an environment of low interest rates has push down mortgage rates and helped to alleviate the collapse in the housing market, and a weaker Euro (for now) has favored exports, we believe further downward pressure remains as Spain works through its high unemployment and negative drag of housing prices.

Banks: Hostage to the Cajas

The cajas, or the nearly 50 savings and loan banks across Spain, remain a critical puzzle piece to the future direction of Spain. You’ll note that the cajas, which control about half the deposits and loans in the Spanish banking system, were the main lenders to real-estate developers and the construction industry, contributing some €175 Billion to fuel the housing boom. Therefore with the pop of the bubble, the mainly municipally controlled cajas saw their bad loans rise at an unprecedented speed and level.

Now the Bank of Spain is pushing through measures to clean up these bad loans, a process in which some cajas will be recapitalized, merged, or allowed to fail. Morgan Stanley suggested that the cajas need “€43 Billion in new capital to plug the hole in their balance sheets from a quickly growing pool of defaults.” Further MS estimates that €76 Billion will be needed over the next 3 years.

If we take these numbers as in the area code of capital required, Spain will have to issue more debt this year. Already Spain has sold €28.2 Billion in bonds this year, one-third of its planned issuance according to the government. While Spain did set up a bailout fund last June, known as the Fund for Orderly Bank Restructuring (FROB), to prop up the banking sector, the FROB with reserves of €12 billion is set to expire in June when the restructuring of the banks was meant to be completed by the government. It’s worth note however, that due to the strict conditions set on the FROB by the EU, there have only been 11 mergers and only 1 caja has drawn on the FROB.

So the limitations of the FROB and the delay from the Spanish government to restructure its banks and cajas are a negative; the road ahead, which could possibly include working with the EU for assistance, is unclear and therefore will likely be interpreted negatively by the market. In any case, the success of the government’s bond issuances to fund the banks (and budget deficit) this year will be crucial. As debt obligations mount, and more attention is cast on the other PIIGS, we could foresee bond yields moving higher. (Note in the chart below that yields spiked for most of the PIIGS in January and February as uncertainty over Greece escalated).

Considering the headwinds for Spain’s financial industry, we’re comfortable on the short side of Spain via EWP, an etf composed 40% of financials. Of total holdings, 22% is composed of Banco Santander and 6% in Banco Bilbao Vizcaya Argenta, Spain’s largest and second largest banks, respectively.

Budget: Delaying Reality

While Spain’s government debt to GDP ratio of 55% looks healthy compared to Greece’s at over 100%, Spain’s hefty Federal budget deficit remains an outstanding risk. At 11.2% of GDP as of 2009, the government has said it plans to reduce its budget deficit to 9.5% this year and is on track to meet demands by the European Commission to reduce the deficit to 3% by 2013, a level stipulated for all members of the Eurozone according to the European Growth and Stability Pact.

While Spain is not an anomaly in violating the 3% threshold this year and last, it stands only in the company of Greece, Ireland, and the UK in reaching double digit budget deficit numbers. To reduce the deficit, Spain has called for belt tightening in the form of an increase to the value added tax of 200bps to 18% in July, the end to its €400 tax rebate to low-income households, and higher tax rates to dividend, interest and capital gains that began this year.

Still, the risk remains that while these measures are positive, Spain does not plan to issue its Austerity Package (that aims at cutting spending by more than 2.5% of GDP) until next year, which may be too late. Further, in the near term similar fears as those associated with Greece’s balance sheet problems could domino to Spain (and other peripheral countries) which would cause severe downward pressure on its capital markets.

Conclusions

As we look at potential investment risks of the Sovereign Debt Dichotomy in 2010, we want to own High Grade versus High Debt. We believe owning Germany and shorting Spain is one way to express this theme. While median predictions for Spain’s GDP is +0.4% this year and 1.1% next, we wouldn’t be surprised to see Spain underperform based on the structural and fundamental headwinds, the main being: further downward pressure in housing prices, high unemployment, the challenges of restructuring and capitalizing its banks, in particular the cajas, and debt risk associated with an extended budget balance.

Conversely, we believe the fiscal conservatism of the German balance sheet will help propel the economy as its exports gains steam from a weaker Euro and global demand picks up. The chart below shows our intermediate term TREND (3 months or more) lines for the German DAX and Spanish IBEX 35, and the dichotomy embedded therein.

Already we’ve seen Spanish GDP contract for the past 6 consecutive quarters (Q/Q), currently at -0.15% as of Q4 Q/Q or -3.1% Y/Y, and we expect to see it continue to underperform Germany, which like its neighbor France, officially exited its recession in Q209. YTD the DAX is outperforming the IBEX by almost 1,300bps.

With sovereign default risks in Greece still not in the rear view despite the loan guarantee from the Europeans and IMF (note the chart below of Greek 5YR CDS), we’re positioning ourselves to take advantage of the existing dichotomies we see among global economies.

Matthew Hedrick

Analyst