ANTM - A better firewall in a changing industryPlease join us on: May 22 at 2PM ET when we will review our long thesis on ANTM Healthcare Subscribers: CLICK HERE for event details (includes video link, materials link and dial-in). http://app.hedgeye.com/feed_items/75347 Health Policy Subscribers: CLICK HERE for event details (includes video link, materials link and dial-in). |

OVERVIEW

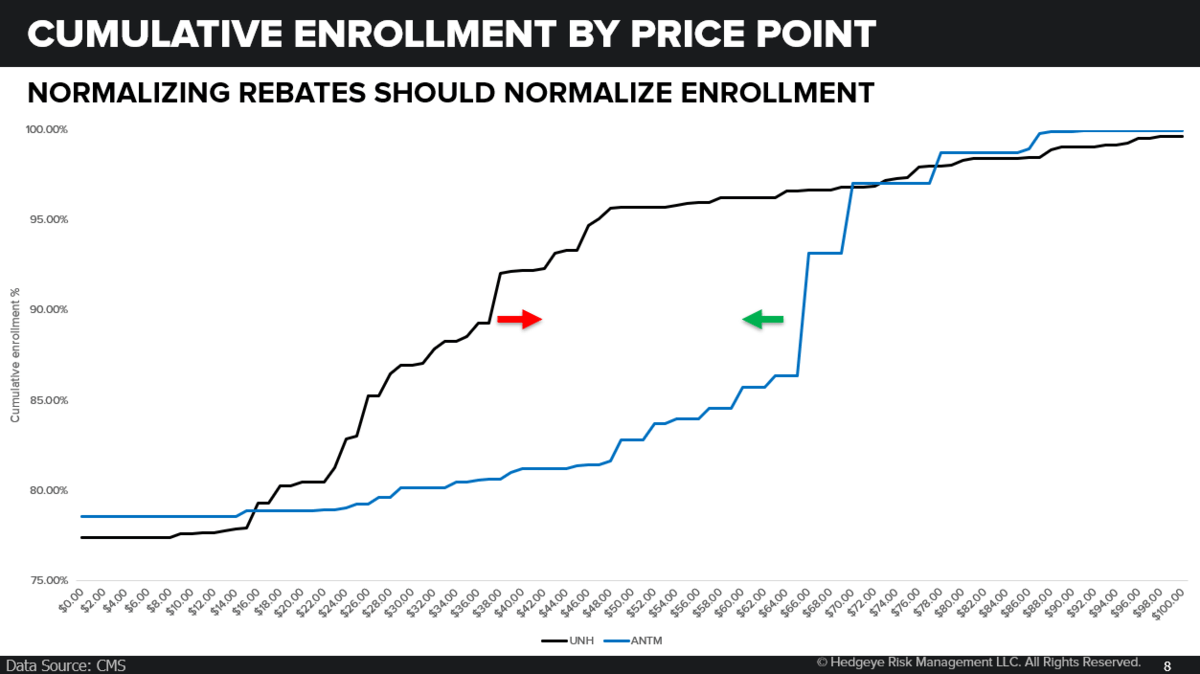

The volatility of the last several weeks surrounding #M4A and a host of other bipartisan attacks on the Health Care Industry have opened up an opportunity to get long the other side of our rebate trade and short in UNH. Anthem has long suffered at the hands of the large PBMs, whether it was their partner (supposedly) ESRX, or a competitor like UNH. Aggregating drug spending and extracting rebates was a never a core competency that ANTM developed, until now. With changes in policy that governs rebates coming in 2020, Anthem should finally be on a level playing field. Our view is less rebates for others will lead to greater market premium parity and incremental enrollment share gain for ANTM.

Looking back, ANTM enrollment has tread water while UNH accelerated. In our view, ANTM is starting IngenioRx, their new in house PBM, at exactly the right time. Assuming premium differences narrow and ANTM can take Medicare Advantage +/- PDP enrollment, every point of share is worth ~$1.00 to ANTM EPS.

Key thesis points:

- Anthem will take share in Medicare Advantage with the emergence of their in-house PBM in 2019, IngenioRX, and rebate policy rule changes beginning in 2020

- Incremental Medicare Advantage enrollment, with additional PDP revenue, is a significant tailwind to average per member premium growth

- In-house IngenioRx PBM being developed in new regulatory environment with the added benefit of risk corridors smoothing the launch

- The initial catalyst will be the release of Medicare Advantage and PDP bid data due during 3Q19

- Managed Care is a relative out performer in Quad3 and indiscriminate #M4A concerns have peaked

- Based on our estimates we believe ATHM 2023 EPS is likely to exceed $40.00 in 2023 with a share price well over $500, a double from current levels

We look forward to having you on the call.

Emily Evans

Managing Director – Health Policy

Twitter

LinkedIn