THE HEDGEYE EDGE

We continue to see Eagle Materials (EXP) as one of the best longs in Materials (or Industrials for that matter).

Not only are the shares cheap relative to peers, transactions, and likely cash flows, but the company is exposed to several potential upside scenarios. These options include:

- An accretive sale to a competitor

- Substantial buyback, or

- Restructuring by shuttering/selling proppant business

Critically, activist Sachem Head is now involved and pursuing a break-up strategy to unlock value that we previously identified. We expect others to join in to Sachem Head’s reasonable efforts to improve value creation. Management felt embattled on both the money-losing proppant business and market valuation. The break-up value could easily be worth north of $120/share, as we see it.

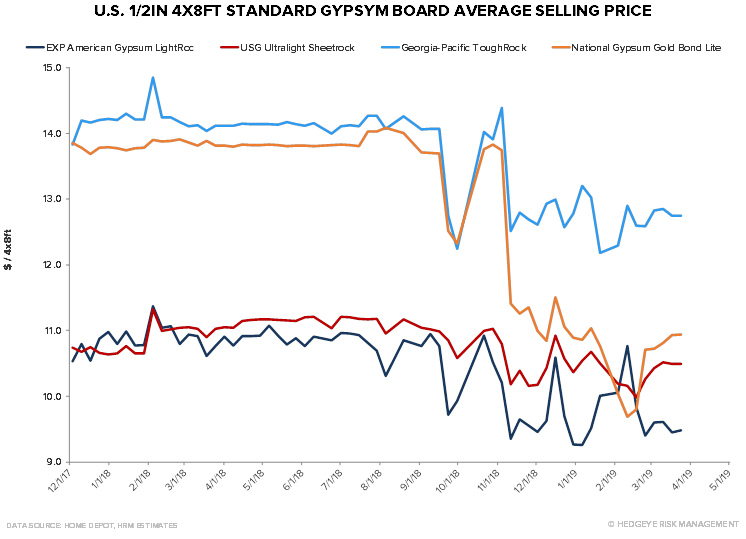

Wallboard capacity utilization is likely much tighter than it looks on nameplate capacity, while cement imports are likely to be needed to match demand growth. Infrastructure may hit investor screens again as the political season renews, a rare topic on which there is some bipartisan agreement. Additionally, wallboard prices are rebounding per our wallboard tracker suggesting a more favorable industry environment.

EXP also fits well within our firm Macro framework in which our team expects a slowing growth environment. We believe infrastructure spending – currently below replacement demand – needs to move up and that the cycle is underestimated with quite a way to rebound from Great Financial Crisis as we see it.

ONE-YEAR TRAILING CHART