THE HEDGEYE EDGE

The Sony (SNE) Long is about multi-year improvement across a broad range of their businesses, both on product/content positioning in the market, but also about the company's improving ability to harness profits, its' newfound unwillingness to tolerate losses, and growing cash flow.

The wrong analysts were on the most recent earnings call. Instead of asking questions about content roadmaps in games + movies + music, content cost growth, pace of new content rollout, content seasonality, content monetization, or content distribution, analysts asked technology questions about 5G smartphones (who cares!) and TV (bleh).

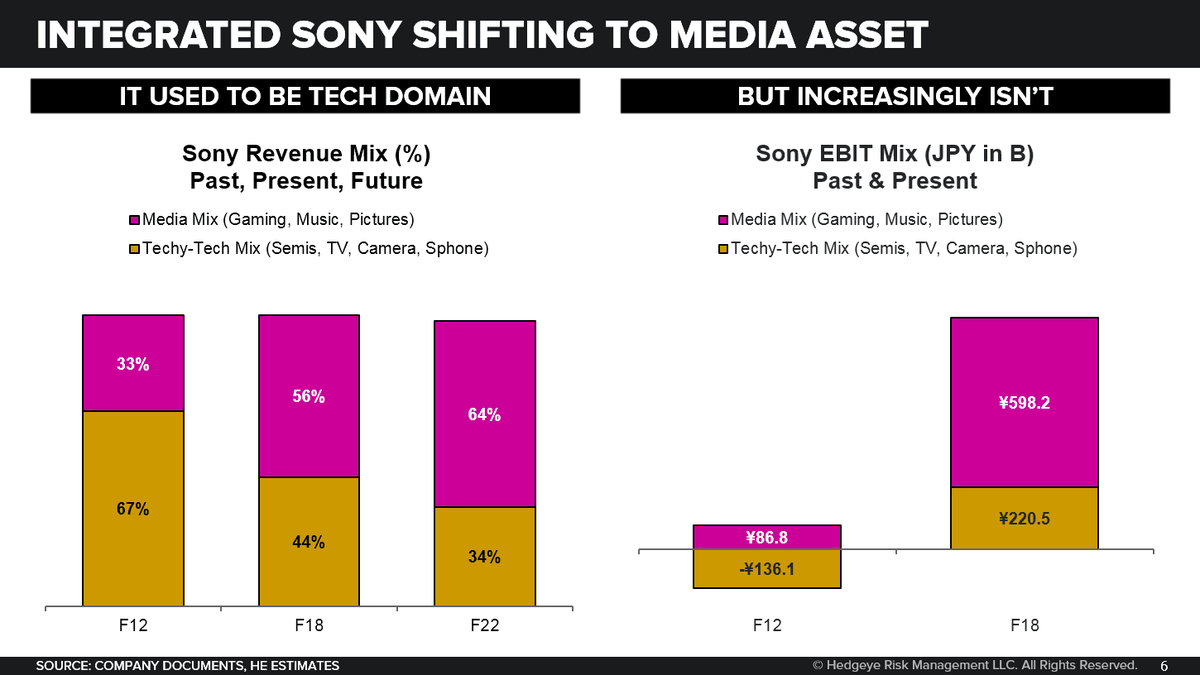

Sony is becoming more and more of a media asset, yet the analysts on the stock come to it from the technology side. The imbalance creates once of the best transition-story opportunities we have seen in large cap tech land in a long time. If you have the right approach to Sony, you can make boatloads. We see a case for opportunistic activist involvement with a combination of both product and fundamental/financial momentum.

Each quarter of OLD Sony invoked the struggle to figure out how segments X & Y [insert whichever segment it happens to be in that given quarter] could have imploded. NEW Sony finds a way to demonstrate ongoing continuous improvement despite a host of 'not as bad as expected' results. F4Q18 featured Gaming, Pictures and Semis all performing a bit better than expected.

FROM A COLLECTION OF LOSING PRODUCTS TO HANDFUL OF WINNERS

Camera, Movies, PlayStation, Music, & Semis have all basically converted from perennial product cycle losers and every-so-often major operating loss creators, to regular product cycle winners and improving profit generators. It is always worth worrying about regression to old Sony but each quarter progress is made. And, from an equity perspective, it really is incorrect at this point to group Sony with electronics hardware, but rather it should be viewed in the context of media equities with 56% of revenue and over 70% of profits from media.

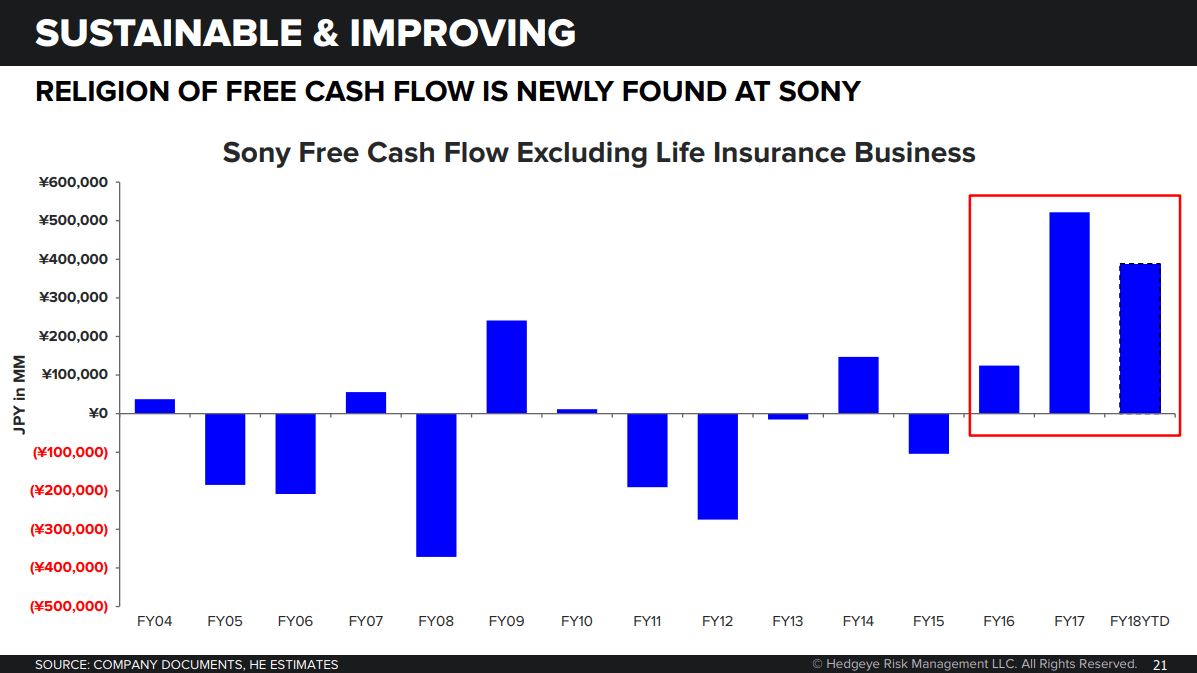

FROM MISMANAGED, CONSTANT LOSSES, TO RISING, CONSISTENT CASH FLOWS

Not that long ago, Sony’s standalone balance sheet (x-insurance) stood at ~$4.4b net debt (June 2011). Today, even after paying billions for EMI in November 2018, the balance sheet is $3.6B net cash. Being cash flow generative is new to Sony, but it is creating strategic reinvestment momentum. It also makes the valuation fundamentally ridiculous at 7x trailing FCF with OCF margins continuing to improve on a rolling basis. If we subtract Sony’s ownership in publicly traded assets from the current equity price ($9.5b), and assume the rumored sale of Pictures goes through at a normal EV/EBITDA rate, and we give Music similar valuation to its French peer, we get $4b of value left to cover Semis, PlayStation, and the Electronics businesses. See the problem?

SECULAR & CYCLICAL RISKS EXIST

Investors worry about game content & distribution disruption with the shift to streaming. I am not. A full blown reality is far away, streaming may add dollars of content revenue for SNE, Google hasn’t succeeded with side businesses, PS leaders know and are embracing it… I am more worried about near term comps in game software after a brilliant content launch period behind us. TV & Smartphone continue to be the main losers, in our view, although TV has not lost in a long time and has been putting up robust ROIC. Still, the next problem will surface there. But overall the electronics group continues to shrink as a portion of the business and matter increasingly less.

We see 30%-50%+ upside from current levels.

ONE-YEAR TRAILING CHART