I’m more inclined to own RL on today’s selloff over a TREND duration. The 18% EPS growth was solid at face value – as was the biggest beat in 3-years, followed up by surprisingly bullish guidance (by RL standards) -- but the quality of earnings left much to be desired. Growth rolled in the core US, and e-commerce globally remained sub-par. All in, EPS growth because of SG&A reduction on a (-1.5%) top line is hardly worth a golf clap – especially with the US worsening on the margin. I can see why the stock is trading down today.

But on the flip side, in listening to management on the conference call, it was the most composed, collected, focused, and dare I say believable that I’ve heard this team in a while. I liked what I heard. The company is still taking up AUR in the US -- but is not out of the woods yet as it relates to repositioning the brand for a younger consumer – hence the negative brick & mortar traffic trends in the US. Unfortunately, that takes years to fix (if possible at all). Also unfortunately, it's going to be costly, which is the main reason I don’t have this name as a Best Idea Long as we have SG&A stepping up to 100-200bps ahead of its low-single digit TAIL revenue growth rate.

But the reality is that it just set up for a 12-15% beat in its FY that just started. I can’t find many names in Retail where I have that kind of confidence in my financial model. Over a TREND duration we’re looking at an accelerating top line, DD% EPS beat, and execution of $600mm in stock repo – all with the stock trading at 7.3x EBITDA. For a name like Ralph Lauren, I’ll take that and wouldn’t even try to talk anyone out of owning/renting it.

But for me to get big in this name, I need confidence that it can grow its top line in the high-single digits – and I’d peg the likelihood of that at less than 10% anytime over the next two years. That’d put $9-$10 in EPS in play (what the Street thought it would earn three years ago) – and would easily be worth a high teens multiple. THAT’s worth getting excited about over a TAIL duration. But there’s too much wood to chop at RL for me to make that call today. Closer to $100 I’d go long RL – but until then I get to better upside with less execution risk in other retail names.

-- McGough

Biolsi’s Review of the Quarter

Ralph Lauren reported FQ4 EPS of $1.07 vs. $.89, the largest percentage beat in three years. Yet shares are down 6% today and down 16% so far in May. The problem wasn’t guidance either. Management has a history of issuing overly conservative guidance, but the outlook for F2020 is in line with consensus expectations. The disappointment from where we sit is with the North American business. The combination of a pullback in off-price sales and Easter (both of which we all knew in advance of this print) were headwinds to results, among other factors. Adjusting for the headwinds brick and mortar comps are still tepid and e-commerce growth is not robust despite an easy comparison and strong industry growth.

North America decelerated sequentially

In FQ3 RL saw North American AUR increase 7% while wholesale declined 3% due to planned off-price reductions. Management considered inventories at full price wholesale customers to be below the prior year. In FQ4 North American AUR decelerated but was still positive, impacted by the Easter shift. Wholesale declined 10% in the quarter with half of the decline from lower off-price sales. Excluding off-price, wholesale declined LSD%. Given the inventory comments in the previous quarter wholesale was disappointing, but likely impacted by cool spring temperatures even if management didn’t mention weather as an excuse.

RL’s retail business comped down 4% in constant currencies driven by a 300bps negative impact from the Easter calendar shift. Brick and mortar stores comped down 7% while owned e-commerce increased 6%. Foreign tourist traffic declined 5% in the quarter against a +7% comparison last year. We have seen the foreign tourist trends follow currency movement across global retail this earnings season. Ralph Lauren has a more balanced global business (nearly half international) than most US brands and is therefore less impacted. The LSD% underlying deceleration could be attributed to the decline in foreign tourist traffic, but will continue as a headwind along with lower off-price sales.

E-commerce growth should be better?

RL’s global e-commerce business grew 11% in constant currencies for the year. North American e-commerce grew 10% for the year comparing against a 22% decline in the prior year. European e-commerce grew 6%. e-commerce growth is the best indicator of a brand’s demand creation. As such Ralph Lauren’s growth rate gives some concern.

International is the bright spot

International continues to be strong for Ralph Lauren. European revenues grew 4%, but in constant currencies grew 11%. Comps grew 5% with e-commerce up 6% and brick and mortar up 5%. Foreign tourist traffic increased 8% in Q4 benefiting from the weaker Euro. For the year foreign tourist traffic was still down 6%. RL continues to flow more inventory into outlets, but at a higher AUR. DTC’s AUR increased 8%. Wholesale grew 11% in constant currencies. European adjusted operating margins expanded 340bps. In Asia revenue grew 7%, but in constant currencies grew 10% with comps up 10%. China is only ~3% of overall revenues, but grew 30%. Asian operating margins contracted 90bps due to inventory reserves.

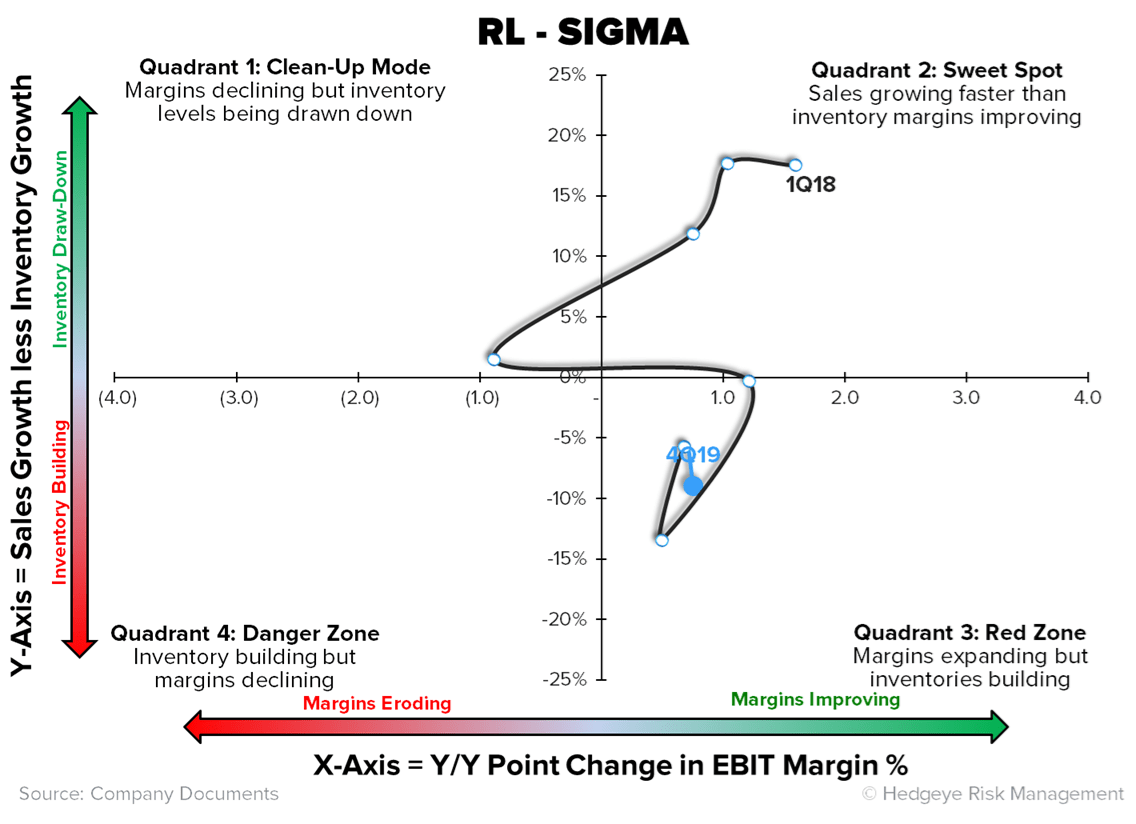

Inventory still elevated for strategic reasons for one more quarter

Inventory levels continue to improve from +15% YY in Q2 to 11% in Q3 and 7% in Q4. The inventory increases last year were due to earlier receipts, less air freight, comp growth, and returning to normalized levels in European outlets. Management stated that after the strategic increase is anniversaried in Q1 inventory growth will be aligned with sales growth. Strategic or not, I believe that inventories are returning to a better balance.

Guidance inline – not sandbagged

- No EPS guidance was provided, but the framework looks to be in line with consensus which should be seen as a positive given management’s practice of sandbagging.

- Q1 revenue growth of 3-5% w/ 30-50bps of EBIT margin expansion compares to consensus expectations of 2.4% growth and 50bps of margin expansion.

- The revenue growth of 2-3% w/ 40-60bps of EBIT margin expansion for the year compares to consensus expectations of 2.8% growth and 60bps of margin expansion.

- For 2020 management expects AUR growth to fall back to the long term outlook of MSD% growth. The pullback in promotions and reductions of off-price sales have driven higher AUR and gross margin expansion for the past three years, but will be a much smaller factor going forward.

- Management also announced plans to repurchase $600mm of shares this year.

Conclusion

I’m modeling F2020 EPS of $8.05, 12% ahead of consensus, so shares are trading below 14x forward EPS which is undemanding for RL shares historically. I’m comfortable with near term forecasts. My concern is centered around the lack of visibility in North American growth drivers. I think the brand needs to invest in demand drivers which suggests the brand is overearning domestically while being too tied to a secularly challenged wholesale channel.