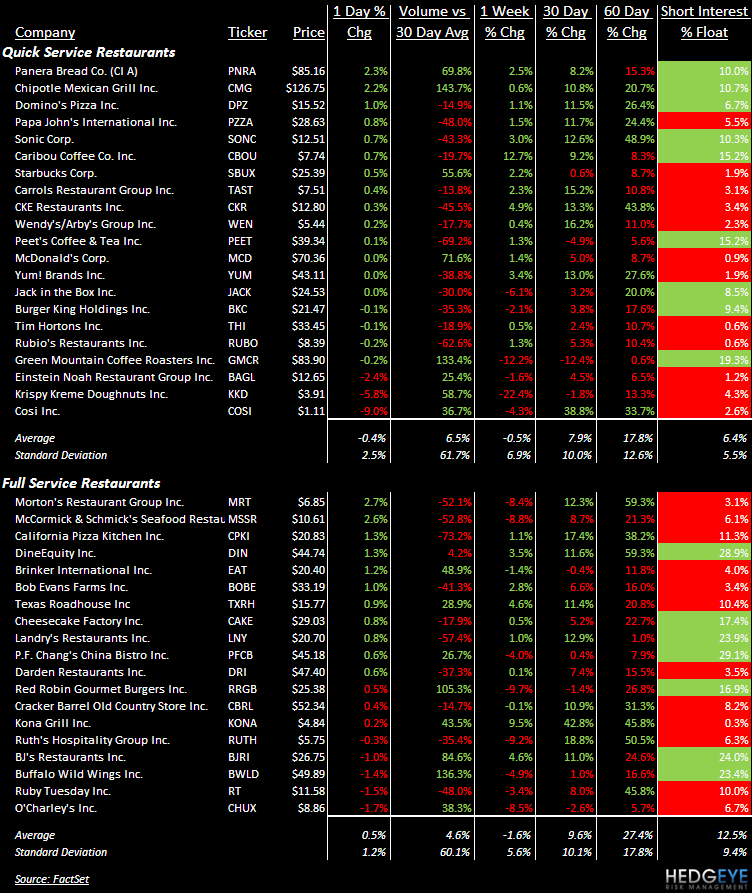

Outstanding earnings driving volume and price, overall market fears persist.

Looking at the table below, it is clear to see that the combination of positive momentum and an increase in the stock price was largely reserved for those companies that reported earnings. That is hardly surprising given the earnings/preannouncements that were released yesterday. The moves in price have been less pronounced than the moves in comps and earnings, certainly, and this is possibly due to the waning momentum seen in the market yesterday.

Yesterday morning, MCD’s earnings were strong and, although the stock only moved 3 bps on strong volume despite the noticeably positive tone evident in management’s commentary. Perhaps in anticipation of the 4.2% U.S. comparable sales number, perhaps not, the stock ran up 2% from Friday to yesterday morning before the release.

After the close, SBUX posted extremely strong numbers also, with comparable store sales increasing 7% during the past quarter, driven by healthy increases in both traffic (+3%) and average check (+5%) in the U.S. with the international division also posting a +7% comp. As you can see below, the positive move in price and volume followed but it was hardly a moon shot. SBUX is up 1.65% premarket. Interestingly, GMCR, which announces earnings next week, is also trading up 1.3% in premarket trading. It should be noted that Starbucks CEO, Howard Schultz said last night that he has a watchful eye on GMCR and its success with the Keurig... “Stay tuned”.

PNRA posted a +10% comparable sales number Tuesday and saw its stock outperform since then; yesterday the stock rose 2.3% on strong volume. With consensus estimates up 2.4% over the past week, expectations are for equally strong bottom line numbers being released on 4/27.

CMG beat the quarter handily on both top and bottom lines. The company’s margins and growth trajectory are some of the best in the industry. With same-store sales seemingly showing a healthy recovery, CMG joined PNRA as the strongest performer in QSR yesterday with a strong boost in price and volume ahead of the earnings release. The stock is up an additional 4.9% premarket.

It also should be note that EAT was up 1.2% on a 50% increase in average volume. The strong performance despite a 10.3% decline in consensus estimates for next fiscal year EPS - the worst in casual dining.

Howard Penney

Managing Director