Below are analyst updates on our seventeen current high-conviction long and short ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

GTBIF

Click here to read our analyst's original report.

We were at the Hall of Flowers conference last week in California to learn more about the branded product landscape in the most important market. There were roughly 275 cannabis companies (mostly branded products) that had booths at the conference. It was clear there were many strong brands in attendance, and that California will certainly be the creative hub of the cannabis industry. But what was also very clear is that there are a lot of subpar brands as well. I would bet at least 30% of the companies in attendance won’t be around in a few years.

Illinois Legalization: The legalization in Illinois is one of the most important upcoming state level events for cannabis companies such as Green Thumb (GTBIF). Illinois lawmakers released marijuana legalization details late last week (article HERE) in an effort to legalize cannabis for January 1, 2020.

AMN

Click here to read our analyst's original report.

We have been optimistic that trends are improving for Health Care Employment, particularly at General Medical and Surgical Hospitals, and even more so for the Women cohort within this time series. It appears Health Care employment continues to accelerate offering indirect evidence that utilization is improving as well. If true, AMN's positive commentary will continue to accelerate and the negative revision cycle will turn positive.

We have been iterating a forecast method for AMN Healthcare (AMN) using machine learning. The 1Q19 result and 2Q19 guidance indicate we are on the right track.

CNQ

Click here to read our analyst's original report.

Though Canadian Natural Resources (CNQ) is light on fundamental catalysts, we continue see it as one of the most compelling opportunities on the long side in energy today. The business is on the back-end of a 10 year CapEx cycle, retains high FCF margins due to low operational costs and bitumen upgrading operations, has a repeatable, low decline asset base, and is shareholder focused. All in all, a rarity in North American E&P. Additionally, we see it as an interesting way to play our Macro Team’s call that Quad 3 and Long Energy will be a persistent theme over the coming quarters.

We value CNQ on a DCF methodology and arrive at a fair value of C$45 – C$50 per share based on a commodity price range of $50 - $60 WTI and normalized WCS differentials of 25 – 30%.

ITHUF

Click here to read our analyst's original report.

According to a Gallup poll, 66% of Americans now support the legalization of cannabis. The growth in support continues to swell across party lines, showing clear momentum for legalization. As more states legalize both medical and adult-use, the U.S. is reaching a tipping point at which the federal government can no longer ignore the massive industry that is forming underneath their nose. We think this will lead to positive federal language being put in writing following the 2020 election.

We believe the U.S. MSOs represent one of the best opportunities to make money in the cannabis space. There are a number of regulatory catalysts on both the Federal and State level that will provide tailwinds for them throughout 2019. As one of the premier MSO’s, we believe 2019 will be a great year of transformation for iAnthus Capital (ITHUF).

WTRH

Click here to read our analyst's original report.

The global delivery market is dominated by a handful of participants, with a few dozen smaller competitors trying to nip at their heels. Over the next few years, we believe there will be a global shakeout, as certain players combine to create more scale and synergies, while smaller players die off as the cost to compete gets too expensive.

Delivery is the biggest disruptor to the restaurant industry we have seen in decades, and we really don’t know yet what it will turn into longer-term. We do however estimate that the U.S. market will become a $200B opportunity, and the global opportunity will be a multiple of that.

There are many competitors in the space providing a myriad of different options for both the consumer and restaurants alike, utilizing different fulfillment methodologies to complete each transaction. We believe in the still early stages it is best to be focused and concentrated on core regions, solidifying strong #1 positions, versus spreading your assets too thin.

Consistent with that view, when we look at the future of chain and independent restaurant operators, it will be important for delivery providers to be a single vertically integrated service that can fulfill all the needs of its restaurant partners. Waitr Holdings (WTRH) has a strong start with a tablet in every restaurant and local teams on the ground to focus on the convergence of services.

THC

Click here to read our analyst's original report.

The labor reports on Health Care last week, from both ADP and BLS, continue to point to accelerating demand. For Tenet Healthcare (THC), now that we've been through a live test of the same facility adjusted admissions forecast algorithm.

While sentiment has fixated on #M4A, we think the real shift happened at the end of February with Congressional attention and action on drug prices that begged the question "if Pharma's not safe, who is?" While we think fundamentals eventually bury the #M4A meme, it's not clear when the iron grip of illogical thinking will finally be broken.

DLTR

Last month activist investor Starboard Value removed its nominees for directors on Dollar Tree’s board. The fund said in light of the constructive conversations with management and the promises made to test shareholder value enhancing initiatives including raising the $1 price point that new directors were no longer needed.

The Trump administration announced further tariff increases this past week. For Dollar Tree the tariff change is a headwind, but it is already in guidance. Management noted on the 4Q call “The outlook Kevin will share is based on tariffs going to 25% as was the expectation when we built our annual business plan in both product through the back half of the year. If tariffs do not increase, we could see margin opportunity, primarily in the back half.” There could be a positive outcome from tariffs for Dollar Tree in that it may create greater urgency to break the dollar price point. Tariffs would also provide the company an external factor to point to when introducing the price point that customers would understand.

We estimate Dollar Tree can add another $2-3 per share in EPS from adding multiple price points. It represents the largest EPS opportunity for the company with the lowest associated risk. If management can also turnaround its Family Dollar banner it could put a $230 stock in play in the out years.

SNE

Below is a note from Hedgeye CEO Keith McCullough sent to Investing Ideas subscribers about why we added Sony (SNE) to the long side of Investing Ideas this week:

|

During Day 4 of a US market smack-down who wants to "buy stocks"? Probably not the people who were chasing charts at the all-time SPY highs last Friday... but we dip buyers of Bullish @Hedgeye TRENDs will gladly start to engage here. One of our Tech analyst Ami Joseph's favorite names on the long side of our Institutional Research product remains Sony (SNE). Here's a summary excerpt from one of his recent notes: If this were OLD SONY, we would be dealing with the disaster of tough comps, weakening profits, bad balance sheet, weak CF characteristics, and a host of lame excuses from management. Instead, today NEW SONY reports continuous improvement across almost the entire business. Sony products and segments continue to show revitalization, a path to winning, and a roadmap of improving profits. The stock is ~11x trailing FCF...with cash flow rising, revenue improving, balance sheet increasingly richer, and overall group quality moving higher. |

EXP

Below is a note from Hedgeye CEO Keith McCullough sent to Investing Ideas subscribers about why we added Eagle Materials (EXP) to the long side of Investing Ideas this week:

|

Now that we're Day 5 into Trump's US stock market correction, we can start to broaden our long exposure (which we didn't do at the all-time highs last week because our #process never has us buy at the top-end of the @Hedgeye Risk Range). My Independent Research Team (read: no conflicts of interest like Old Wallbrokered and banked "research") and I have plenty of ideas. Timing matters though. The SP500 is not only at the low-end of its @Hedgeye Risk Range right now, but the implied volatility PREMIUM on SPY has blown up to a new cycle high. Eagle Materials (EXP) is currently an activist name that Jay Van Sciver pitched pre activists going activist! Here's a summary excerpt from Jay's Institutional Research note with his $120/share sum of the parts valuation: "We pitched the activist thesis earlier and see Eagle Materials as an excellent activist target. We expect others to join in to Sachem Head’s reasonable efforts to improve value creation. As we noted in our presentation, management felt embattled on both the money-losing proppant business & market valuation. The break-up could easily be worth north of $120/share, as we see it." |

TSLA

Click here to read our analyst's original report.

Over time, we think Tesla (TSLA) is a business that can't become competitive in a capital intensive low-margin business as an already sub-scale manufacturer.

On this sub-scale point, if you look at the slide below, you'll see that even though Tesla sold more cars in the first quarter than they usually did, gross profit per vehicle is down. The reason they had profitability in the second half of 2018 was because of SG&A per vehicle. Reminder, they closed all their stores in the first quarter.

The reality is the whole bull thesis is not playing out. Tesla is not making higher gross profit at higher production levels and now they're trying to switch the narrative to autonomy.

ROL

Click here to read our analyst's original report.

The current share price of Rollins (ROL) makes little sense to us, and we expect a significant downward revaluation by the market.

Margin gains have stalled amid increasing competitive intensity in a mature, slow growing market. Attractive markets for growth and acquisitions present less runway and higher transaction prices.

Wages Up, ROL Margins Mostly Down: Profitability is influenced by labor costs. Wage inflation is likely to impact ROL profitability. Low pay can result in increased employee churn, which can end up more costly than just paying the technicians to increase retention.

DVA

Click here to read our analyst's original report.

The DaVita (DVA) quarter was slightly better and guidance was reiterated. Our timelines are moving out, but we don't see a good reason to exit the short.

Patient volume was lower than consensus and management expectations. A key driver of our short thesis is our patient and mix model that calls for 2-3% market growth largely coming from growth in the Medicare population, volume that carries a negative margin.

In other news, CVS was featured in an article on Bloomberg earlier this week ("CVS Plans Final Home Dialysis Study in `Not-Too-Distant Future’"). The dialysis facility roll up is over after more than a decade of consolidation. With Telemedicine, a device, and home care agents, CVS can chip away at DVA patient share. Home dialysis is far more likely to be a younger, healthier, working, and commercially insured patient, making small shifts to CVS home dialysis extremely painful for DVA. The effort by CVS is not new, but this update is new.

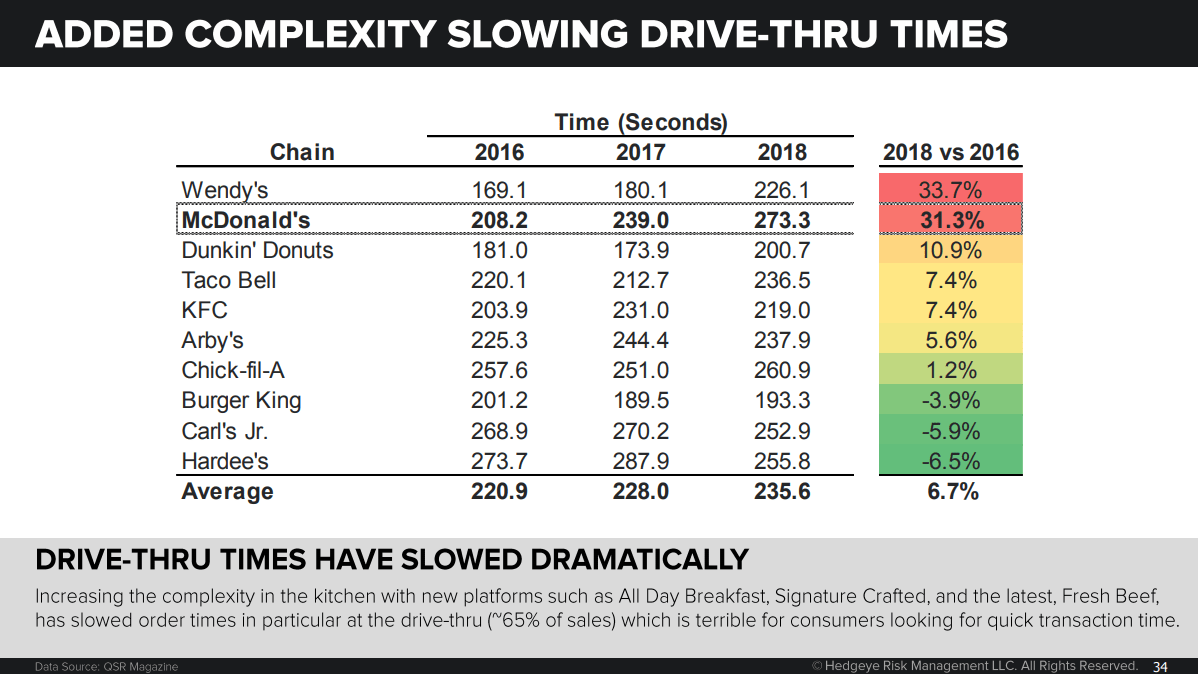

MCD

Click here to read our analyst's original report.

I (Restaurant analyst Howard Penney) was a big fan of the changes McDonald's (MCD) CEO Steve Easterbrook was making in the early days of his tenure as CEO. In the nearly 4 years he has been CEO there have been a significant amount of positive changes at the company. There have also been some changes that have sent the company down the wrong path, leading to significant disappointments.

The most obvious disappointment was the hiring of Chris Kempczinski, the head of MCD USA. Chris’s inability to understand how important the franchisees are to the company has led to the formation of the National Owners Association. An organization the company has never needed in its 50 year history. Over the years there have been issues with the franchisees, but nothing like what we are seeing today.

These are extraordinary times for the company, and it appears the current CEO is in denial of the realities of the business. Until changes are made at the top, MCD’s operating performance will continue to disappoint.

Case in point, drive thru times have slowed dramatically. Increasing the complexity in the kitchen with new platforms such as All Day Breakfast, Signature Crafted, and the latest, Fresh Beef, has slowed order times in particular at the drive-thru (~65% of sales) which is terrible for consumers looking for quick transaction time.

TXRH

Click here to read our analyst's original report.

With Texas Roadhouse (TXRH) having to narrow the value gap, by raising menu prices, what is going to happen to the brands industry leading traffic trends? Our belief was that sales trends were going to slow regardless, so the increased prices add a new level of uncertainty to the trajectory of sales.

Capital Spending – One of the biggest negatives coming in 2019 is the increase in capital spending. Capital spending going up by $45 million or 25% to $200 million.

Pricing – TXRH will be running 3.2% pricing in 2019 vs 1.3% in 2018. The million-dollar question is, can they maintain traffic growth in 2019 with all this pricing? After the company raised prices aggressively in late 2011 and 2012, traffic slowed meaningfully for the next two years. (see the charts below)

EAT

Click here to read our analyst's original report.

Restaurants SSS for the month of April as tracked by Black Box went negative for the second time this year to -0.4%, resulting in a 2-year average of 0.5%, down 50bps sequentially. Same-store traffic was down -3.5% in April, for a 2-year average of -2.5%, down 50bps sequentially as well.

The Easter shift from March to April this year meant a negative hit for many restaurants (black box noted SSS growth during Easter week approached -2.0%), but the negative trend continues for the space as we navigate the early innings of 2019.

The strongest region was the West, with SSS of +1.1% and SST of -2.3%, while the weakest region was the Southwest, with SSS of -1.9% and SST of -4.9%. Employment and labor issues remain a top concern for operators, on a broad basis operators continue to be impacted by MSD labor rate inflation and an inability to properly staff their restaurants.

As we have been noting, Black Box noted the continual increase in menu prices as a primary driver for a slowdown in traffic. Restaurants have increasingly difficult comps as they navigate CY19, we believe the weakness in comps is only beginning.

With challenging Restaurant industry trends persisting, we reiterate our short call on Brinker International (EAT).

PENN

Click here to read our analyst's original report.

Sports betting is driving Mississippi to higher growth this year but Penn National Gaming (PENN) isn’t participating. Meanwhile, the sell-side had been modeling 3-5% revenue growth for PENN’s Mississippi segment this year, which is far too high. The Tunica closing will pare those Street expectations down but the fact is PENN’s losing market share in one of the few bright spots in regional gaming land. We don’t see PENN MS boosting EBITDA in the South segment this year which puts more pressure on the other properties in that region to grow as well as anticipated PNK/PENN synergies to be realized.

UNH

Click here to read our analyst's original report.

Click here to watch the entire webcast replay from Healthcare analyst Tom Tobin reviewing his sector's current Position Monitor and more!

AGENDA:

- Position Monitor: Updates to best investing ideas

- U.S. Medical Economy: Positive trends in the face of deteriorating sentiment

- UnitedHealth Group Inc (UNH): Unlikely to break the fever anytime soon

- AMN Healthcare Services, Inc.(AMN): Good 2Q19 guidance, entering a positive commodity cycle

- Teladoc Health Inc (TDOC): Telemedicine trends in active users

- Davita Inc (DVA): Earnings next week, still waiting on DMG sale, wage inflation as the biggest threat

- Q&A

CLICK HERE to access the associated slides.