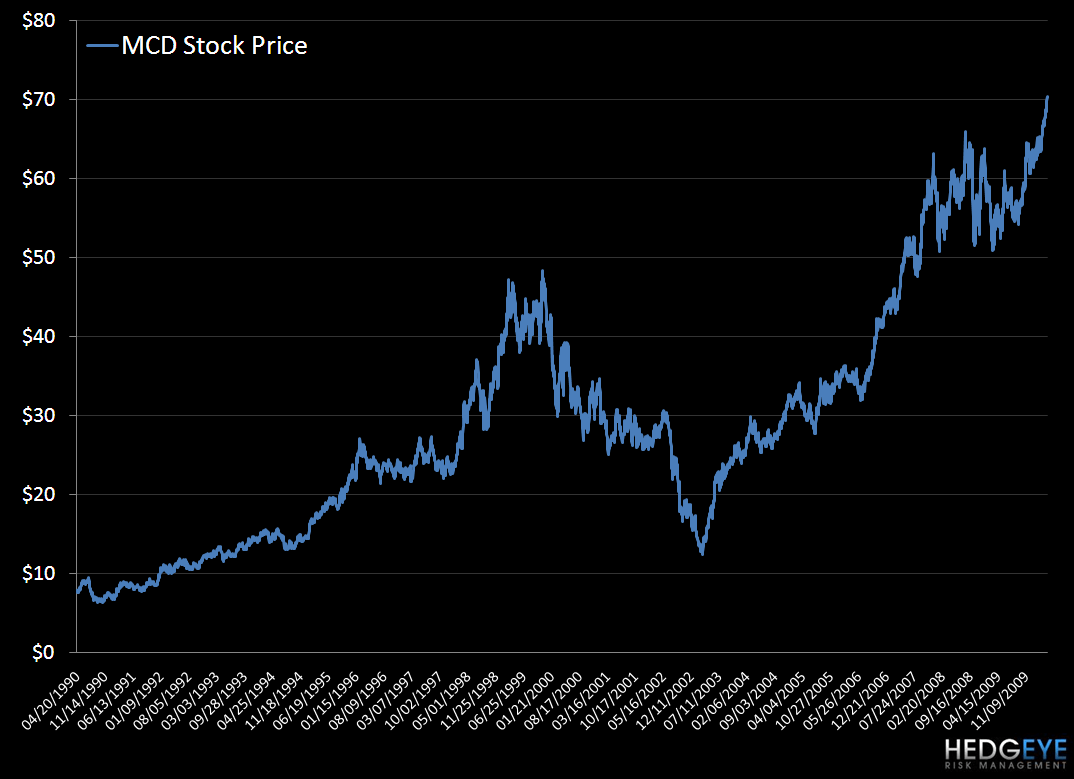

The stock’s performance today is somewhat surprising in light of MCD’s outstanding 1Q10 numbers.

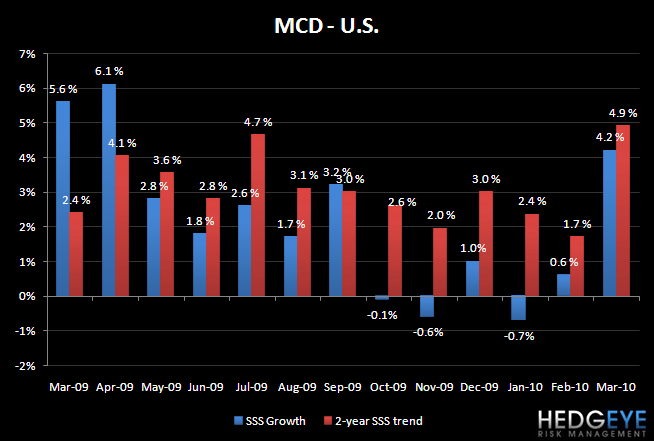

The 1Q10 results out of MCD today were nothing short of outstanding. Same-store sales in the U.S., which have struggle recently, came in strong in March, up 4.2% on top of a difficult 5.6% comparison last year. Management stated on its earnings call, more than once, that top-line momentum across all segments has continued in April. The stock’s performance today is somewhat surprising in light of these results.

Management sounded extremely positive on the call and the results warranted that optimism. Looking at MCD’s stock chart and considering MCD’s comment that the last time quarterly U.S. company operated restaurant margin exceeded 20.4% (the company reported 20.4% in 1Q10) was in the second quarter of 1994, nearly 16 years ago, investors may be concerned about where MCD goes from here.

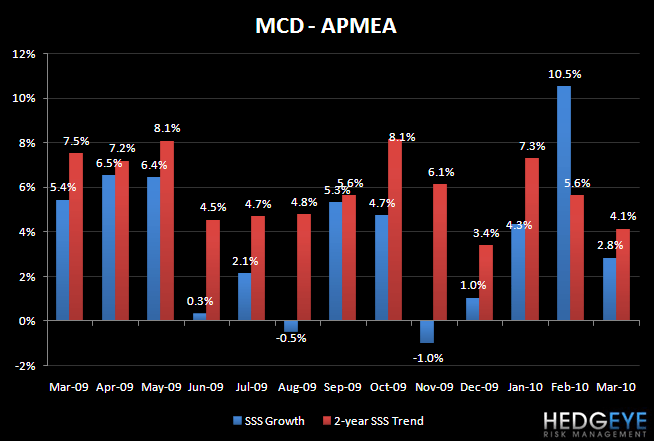

Comparable Store Sales charts:

NOTES FROM THE 1Q10 EARNINGS CALL:

The momentum seen in comparable sales trends in March is continuing across geographies in April with positive sales momentum maintained in all markets

Sharing ideas with franchisees and building the brand. Taking the business to the next level.

Comparable sales, op income, and EPS all showed strength.

US

- Later this summer launching smoothies, becoming more of a beverage destination

- Continuing expansion of McCafe

Europe

- Fourth tier

- Snack offerings in UK/GER doing well

- New sandwiches performing well across markets

- Strong increases in extra value meal growth

APMEA

- Launching ¼ lb in Singapore

- Value lunch driving TC and sales

Consumer relying on MCD to deliver affordability

- Driving traffic through new products and core products

- Convenience and look of new restaurants are driving this too

Remodels

- Australia and EU leading the way

- 400-500 in the US this year, interior and exterior

- China opening 150-175 new units this year

Improved perception across markets where critical mass exists

- Strength of the brand is also dependent on great service

- APMEA top customer satisfaction

- China and Japan leading the way

- US and EU also making progress in improving satisfaction scores

In the US more than 1/3 of restaurants are open 24 hrs

APMEA

- Convenience is a key driver of business

- Continued expansion of 24 hr service driving sales in Japan

- Breakfast available in 75% of APMEA stores

Momentum is continuing this year

- Value, experience, product are in line

- Keeping financial discipline

- Highest graded company in the space

- Returning FCF to shareholders – 1bn in 1Q

- Confident of achieving continued success

Chief Financial Officer

- Plan to win continues to drive sales, guest counts

- 1Q operating growth of 20% to nearly $1.7bn

- Combined operating margin increased 220 bps to nearly 30%

- Lower food and paper costs have allowed the continued expansion of margins

United States

- Lower food and paper costs (and refranchising) helped operating margins increase to 20.4%, by 210 bps

- Basket of goods decreased 5% in 1Q

- Commodity outlook for the U.S. is down 2%-3%

- “remain focused on building traffic”

Europe

- Company operating margins increased 200 basis points in 1Q, to 17.3%

- Strong comparable sales in France, Russia, the U.K.

- Lower commodity costs were partially offset by higher labor and occupancy costs

APMEA

- Company operated margins increased 200 bps

- Lower commodity costs, operating efficiencies, positive comparable store sales

- Benefitting from heavily franchised structure

- The mix of APMEA’s margin was adversely impacted by the Aussie dollar strengthening

G&A

- Improved as % of sales

- Still expect full year 2010 G&A to be up slightly

Closing underperforming stores

- Closing 430 stores in Japan

- Negatively impacted EPS by $0.03

- Expecting minimal charges for the remainder of the year

Reimaging

- Timing is ideal

- Investing on a scale that can’t be matched…

- Reimaging over 2k units this year

- Half in EU, 600 in APMEA, remainder in U.S.

- Only 20% of exteriors globally are up to date

- 40% of interiors

- Rebuilding over 150 restaurants this year

- Average sales lift above overall market performance of at least 6%-7%

- Coinvesting with owner-operators

- $150-200k

- Remaining $250-500k from operators depending on what they need done to the units

Debt

- 45% of total debt is in foreign denominated currency

- Hedge vs volatility

Performance over the past quarter is a testament to the alignment of the system in a challenging environment.

Q&A

Q: In Europe and US, how does check break down? Was traffic above SSS and check below? You think that check can improve in the year? Any pricing this year?

A: Has been a fall off in check, particularly breakfast, due to how menu is being presented. Still holding the line on pricing.

Seeing an even larger % of sales growth being attributable to guest counts, which are tremendous. That’s what the focus is. TC’s were 50% of the comp growth in Europe.

Q: US business and the acceleration in the comps in March, positive tone in April…is core consumer feeling better or is it MCD?

A: Consumer confidence scores getting better, more spending in the marketplace. Unemployment is in a tough spot and spending won’t pick up meaningfully until jobs come back. Results are because of strategies around value – which remains the most important thing to MCD guests. As much about strategies as it is the improved state of the consumer.

Q: Commodities?

A: Probably seen the best quarter in the year in terms of the first quarter. Expect it to continue to be favorable and that will allow us to wait to take price whereas others will be under pressure.

Q: Drive through in China? Outlook there?

A: Development in China…beginning to understand how to develop drive thru’s in out rings where you have less density but where you have car traffic. Tremendous opportunity to grow the business along with growth of free standing units.

Some of the best customer satisfaction scores in China and the structure of the organization there is performing well.

Q: How sustainable is the March pickup? On the smoothies, will they be ready in time for national advertising over the summer?

A: March was a good month. Growth in all day parts for the entire month. Momentum is continuing into April. Broad based across the items…frappes were a part of it.

Frappes are in 9k restaurants and the performance expectations are exceeding what we thought they would. Smoothies will be ready for national advertising. Already in 2k units. Hearing strong reports from operators.

Q: How do you guys manage the cost down so much with inflation in so many proteins…how does that give you a pricing advantage over time.

A: Great supply chain at MCD. Some fixed price contracts, some options, some forward buying…and we can negotiate good pricing with the relationships we have. Important for owner/operators to be clued into promotions coming in the next 6 months to mitigate impact on margins and be proactively prepared. The product mix can be helped by higher margin products/promotions that support the company relative to the overall food cost

Q: The cost of remodels…between 4 and 7 thousand?

A: This is the first time that MCD has given guidance on what the costs are going to be. Hard to come up with an average cost across 6k US units of varying sizes, ages, and owner/operator preferences. Doing interior and exterior gives a significant lift to sales. Even at higher end of range, we’re seeing returns in the low double digits in the first year, cash on cash. We feel confident in the level of investment and sales expectations will warrant that investment.

Q: April?

A: Won’t be lower than the quarter – so the floor is 4.2%

Q: On the U.S., breakfast dollar menu, can you give mix on that…impact to margins? Competition? Also, in terms of returning cash to shareholders? Refranchising?

A: We’re at 80% in terms of franchising. Optimizing portfolio around the world for how we perform. On the breakfast mix…we’re selling more coffee. $ menu is sausage biscuit, sausage muffin, hash brown, and coffee (then other menus that were already on there). Low cost food and paper in these products. All in all we’re really pleased and the goal was to recapture guest counts. Food at home down 2%, food away from home at 3%, we can’t take a lot of price. Happy with breakfast TC’s.

Q: Metrics on beverage mix? How coffee has performed? Where was the beverage mix 3 or 4 years ago, today, and where is it going? Healthcare reform on corp and franchisee level?

A: On healthcare, 2014 is implementation. Franchisees are a federation of small businesses. It will vary by number of fulltime employees? 90 day waiting time to enroll, allowance, that helps when operators are evaluating whether someone is going to be fulltime. $10-30k per store. TBD.

Corporate level won’t be impacted.

Q: On Japan, profitability of the stores that are being closed over the next year or so? Any guidance on how to think about contribution from Japan to equity income?

A: No real impact from the closures. 30 got closed so far. While they were lower volume and return, there was no significant impact. Not a significant drag. There will be some sales transfer, higher performing operations to being with.

The closures were restaurants that were size and logistically constrained. Inhibits menu innovation. April 25, reopening some stores in Tokyo and those stores will be very iconic in Japan. We will see that market begin to turn. Got to get rid of some older constraints within system.

Q: 150-200k total on reimages? Talk about return…as you coinvest how does that impact franchise margin versus how it worked for older reimaging programs? Anything noticing in speed of service? Discounting levels compared with 6/12 months ago? Why would you push franchisees to let up on discounting when it’s defending traffic when they have margin risk?

A: Investment…we had a fixed amount during the older programs – 85k – we thought it would be 170k each total. Franchisees ended up spending 250k because they saw other stuff they wanted. Now we’re looking at 40 percentile of the lease hold improvement. This time, there is a broad range; restaurants have different needs- inside, outside, signage…

Speed of service hindrances have not been observed. Drive through capacity has been adjusted and service is still as fast as it ever was. Doing well on that end.

Discounting level…we have consistent value across the year. That allows us to ingrain it in customer and talk about frappes or smoothies or angus, we’re not jumping in with promotions here and there, we are consistent.

And on the coinvesting, where you will see that show up will be in additional depreciation on the franchise margin line

Q: McCafe expansion in Europe still doing well?

A: Pretty much…sales performance is strong. Germany and France performing well. France is reimaging exteriors in 2010. In US, espresso drinks are given through drive thrus and over the counter…

Q: Plan to win has been a success…over the years we’ve heard about McGriddles, drinks…how do you guard against mistakes and increasing complexity in the back of the house with new promotions?

A: We stay focused on the future, focusing on food development protocols…innovation labs…very deliberate process. We don’t move forward with anything not completely tried and tested.

Investment in process and execution of operations has also picked up very much versus 8 years ago. Plan to win focus is what’s helping today and the reinvestment and infrastructure that has been established is the difference that is often missed

Howard Penney

Managing Director