Below are analyst updates on our fourteen current high-conviction long and short ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

GTBIF

Click here to read our analyst's original report.

U.S. MSO’S REPRESENT GREAT OPPORTUNITY: But don’t count out brands/wholesalers either! There are roughly 330M people, with an estimated black market cannabis spend of $50B, that is ripe to be harvested through the new legal market. Through their brick and mortar locations, the U.S. MSO’s represent the entry point to legal cannabis, giving them a leg up from a sales and long-term branding perspective. We believe the need for an alternative to highly addictive and dangerous opioids, coupled with a general need for wellness and therapeutic uses, will lead to faster adoption of cannabis than previously expected. The U.S. is where brands are built, and we don’t expect cannabis to be any different.

Green Thumb (GTBIF) was our first best idea long in the US space as we feel they are one of the best positioned MSO's to capitalize on the growing market opportunity in the US. There is line of sight to GTI providing a 2-3x return over the next few years.

AMN

Click here to read our analyst's original report.

“Demand in travel nursing continued to strengthen as we exited the first quarter, and today it's at the highest level-we've seen in two years. In fact, Travel Nurse orders are currently up more than 25% compared to prior year.” - Susan Salka, CEO

AMN HEALTHCARE (AMN) POSITIVE 2Q19 GUIDANCE: You can accuse us of squinting a bit too hard at the 1Q19 earnings release and 2Q19 guidance that forecasts Nurse & Allied revenue of $319-$323 million versus consensus of $327 million and describing it as positive. In our defense, the relevant data point is the acceleration of growth to "4% to 5%" when legitimately excluding $25 million in labor disruption revenue from 2Q18 compare. In addition, there was positive commentary on MSP pipeline and recent contract wins; on Travel and Allied demand; on the acquisition of Advanced Medical; and on the stability/improvement in Locum and OWS/Search businesses.

CNQ

Click here to read our analyst's original report.

After a 10+ year investment cycle, Canadian Natural Resources' (CNQ) asset base is extremely efficient, high margin, and diversified with a solid balance sheet. It generates free cash flow in nearly any commodity price environment. At normalized differentials CNQ’s oil sands mines have better economics than nearly all shale oil-levered E&Ps. On a full-cycle basis, CNQ’s upgraded mining operations have one of the highest FCF profiles in North America.

The stressed pricing environment in 4Q18 illustrated the strength of CNQ’s upstream operations. The company was the only major Canadian producer to generate unlevered FCF from upstream operations, and it significantly outperformed peers on a levered basis as well.

We reiterate our long call on CNQ.

ITHUF

Click here to read our analyst's original report.

DESPITE LACK OF FEDERAL LEGALITY, USA IS A GLOBAL LEADER IN CANNABIS: The U.S. has roughly 330M people, of which roughly 73% (236M) of them are over the age of 21. California represents the largest opportunity in the country with 39M people, of which 29M people are over 21 years old (California > Canada). With the U.S. boasting a cannabis usage rate of 17%, it makes it an ideal market from an addressable population perspective to invest in as long as you are focused on the more advantageous states. A state such as California, and other more established states can operate a legal cannabis industry within their own border but not all states are capable of doing this. There are vastly varying wholesale prices across the country, so people building business models around a price of $2,500 to $3,000 will be in for a rude awakening if/when cross border trade opens up.

In the early innings of this industry having a sound management team and corporate governance is of the upmost importance, you are buying management teams and the promise of huge sales growth at this point, so you have to have faith in execution. We liked iAnthus Capital (ITHUF) before the MPX deal, but really like it after with addition of Beth to the team, she will likely prove invaluable over time. We think the Gotham Green investment speaks to a broader role that iAnthus could play in cannabis, and think this entity could become part of a cannabis conglomerate that operates across the global spectrum of cannabis.

WTRH

Click here to read our analyst's original report.

We like Waitr Holdings (WTRH) for three key reasons:

- The growth in the delivery industry

- A strong business model driving strong relationships with restaurants and consumers

- M&A – WTRH is looking to build out a strong restaurant/delivery ecosystem

When we look at the future of chain and independent restaurant operators, it will be important for delivery providers to be a single vertically integrated service that can fulfill all the needs of its restaurant partners. WTRH has a strong start with a tablet in every restaurant and local teams on the ground to focus on the convergence of services.

THC

Click here to read our analyst's original report.

The #MedicareforAll theme, economic growth concerns (Quad 3/4), rotation out of Health Care stocks, UHS's mixed results and commentary on 1Q19, have all been banging THC and the Health Care group around the last month. Heading into the earnings print expectations for Tenet Healthcare (THC) appeared low given an EV/EBITDA multiple of ~7.0X and a price that had fallen -26% from $31 and its YTD high on April 10th. THC's 1Q19 results should provide some relief. We continue to like the turnaround story of divestitures and cost controls in a secular backdrop of rising Outpatient/ASC mix.

TSLA

Click here to read our analyst's original report.

We measure Tesla's (TSLA) test drive slot utilization, and both the Model 3 and S&X show significantly reduced interest. Maybe closing stores and firing sales was bad... 1H19 is the catalyst period for our short, and we see every indication that the short is playing out quickly. In terms of the capital raise, we have suspected that a "death by dilution" scenario is likely.

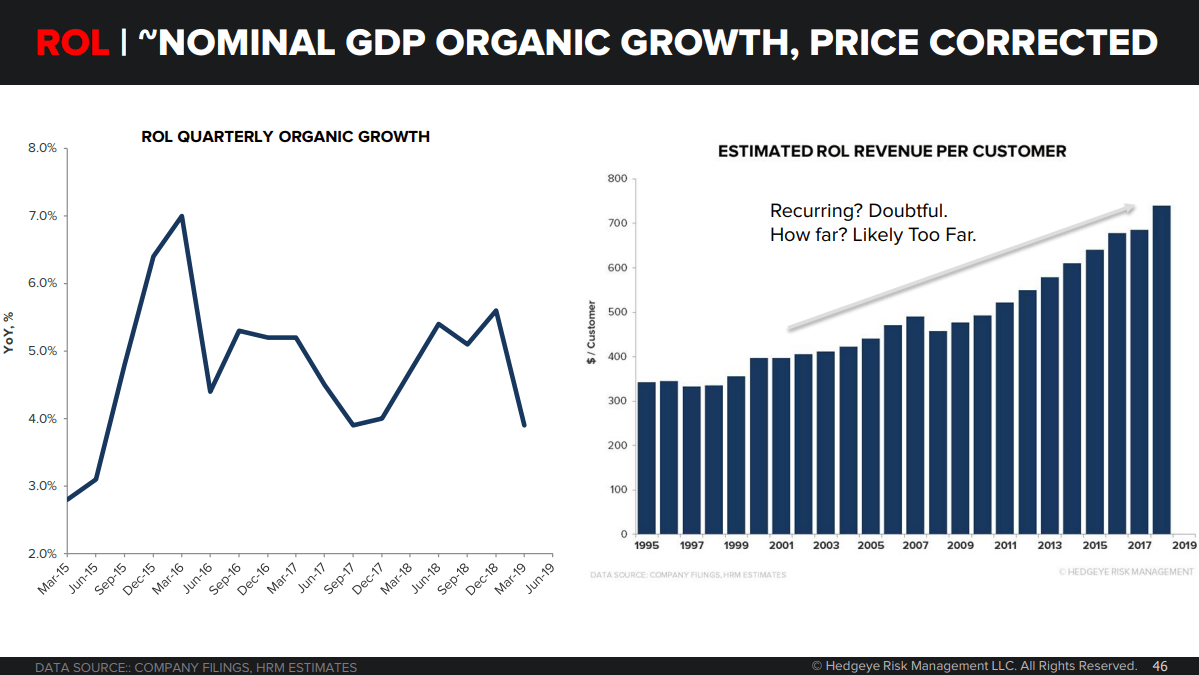

ROL

Click here to read our analyst's original report.

We are not saying Rollins (ROL) is bad, corrupt, or anything like that. We just see it as facing an organic growth deceleration and some aggressive competition. Aggressive foreign entrants like Rentokil and Anticimex are determined to take market share. Simply put, this is a low-barriers to entry business with GDP-ish growth.

Pest control is just not a 52x business, and increased market volatility accompanying Quad 4/3 scenario is likely to continue to reprice these names like ROL.

DVA

Click here to read our analyst's original report.

We continue to think DaVita (DVA) is a ~$40 stock. The sale of DMG and the consequential stock repurchases will not be sufficient to overcome the combined forces of accelerating labor costs, organic growth headwinds, little capacity for inorganic growth and a federal policy that aims to limit progression of kidney disease.

Furthermore, the Macro environment will continue to be unfavorable for the stock. Our Macro team thinks we're headed to a Quad 3 environment (i.e. Growth slowing and Inflation accelerating). This environment has historically not been positive for DVA. See the historical back-tests below.

We reiterate our short call on DVA.

MCD

Click here to read our analyst's original report.

New products and promotions are a sign of weakness in your base business. Business was great in 2016, so McDonald's (MCD) didn't have to do a lot of promotions, as they had to lap that strength (which included All Day Breakfast), MCD has to add promotions which increased complexity and had an impact on traffic over time.

TXRH

Click here to read our analyst's original report.

Texas Roadhouse (TXRH) is unique in the restaurant industry for its consistent growth in customer traffic. They have been able to achieve this by running great restaurants and keeping prices on the menu low. Unfortunately, there is a price to be paid for this strategy when sales trends slow and you are left holding the bag of higher inflation, profitability suffers.

We reiterate our short call on Texas Roadhouse.

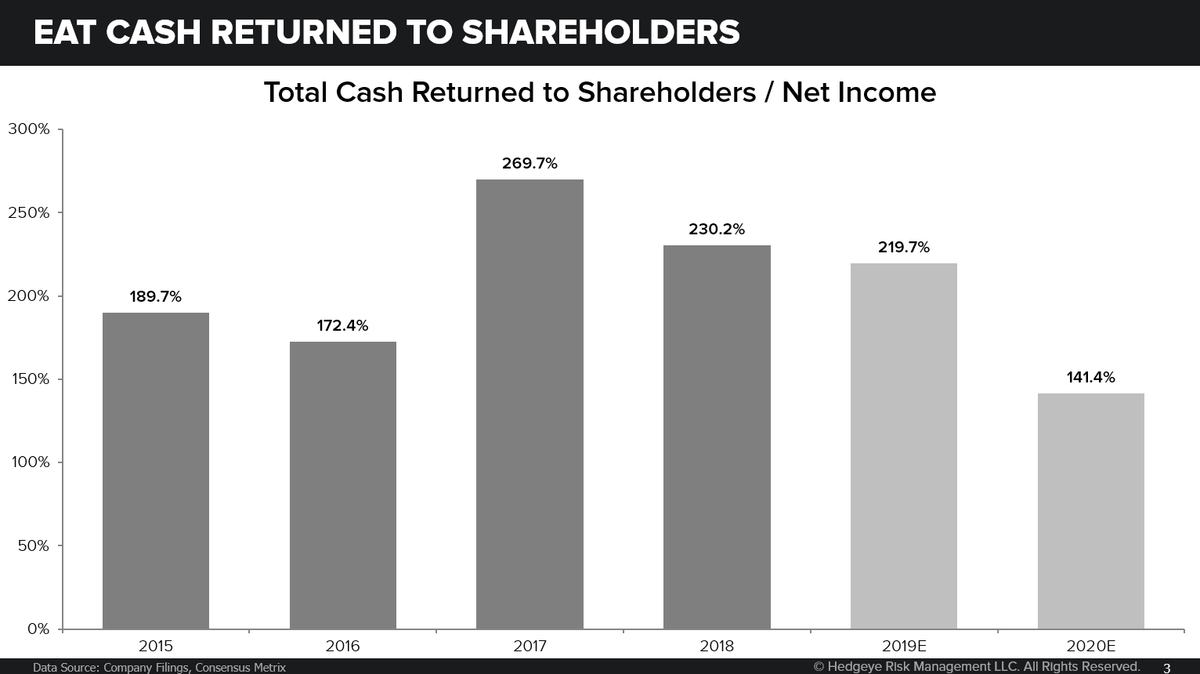

EAT

Click here to read our analyst's original report.

Brinker International (EAT) management has done what it can to return cash to shareholders over the past three years. The balance sheet has the appropriate amount of leverage, so it is unlikely that another big share repurchase program is in the immediate future.

We currently don’t see a pathway for margins to improve from current levels and some downside remains if value promotions continue to gain preference.

PENN

Click here to read our analyst's original report.

Penn National Gaming's (PENN) Q1 EBITDAR was generally a little better vs reduced expectations, despite revenues missing us and the Street by $8m and $10m, respectively. On the property level, the Northeast segment margins were 29.9%, 20bps better than we modeled. The South segment EBITDAR performed in-line with us but higher than the Street. Note that PENN had a $3.1m true-up of customer loyalty liabilities in Q1; excluding that adjustment, their adjusted EBITDAR would have been $395m which is unchanged from their previous guidance. As for 2019 guidance, PENN lowered EBITDAR by $3m which totaled the miss in Q1 2019. Hence, the company did not lower EBITDAR expectations for Q2-Q4 2019, despite a big reduction in the revenue forecast. A major reason is the hike in PNK synergies. Management hiked PNK cost synergies to $55m this year ($50m previously) and $60m in 2020 ($50m previously). We already anticipated this in our model while the Street probably did not model the increased synergies yet. As for revenue synergies, management left the $15-20m target unchanged. Furthermore, PENN is excluding $4.4m in pre-opening expenses and $5.7m in contingent purchase price from 2019 EBITDAR – both categories are materially higher than previous 2019 guidance. Obviously, it could be higher Margaritaville-related costs but this is seen as a low quality approach to boost EBITDAR.

While management may provide an optimistic view on April trends on the conference call, we still believe April GGR will decline for the mature markets. Revenue expectations (ex Greektown) may still be too high for the rest of 2019 for PENN. As a result, EBITDAR guidance may be cut again later this year despite higher PNK synergies.

UNH

Click here to read our analyst's original report.

The House Rules Committee held the first ever Medicare for All hearing, something promised by Speaker Nancy Pelosi as part of her campaign to secure her leadership position in January. House Ways and Means is scheduled to follow suit in the coming weeks. Republicans, banking on their belief that most Americans would prefer Washington put an end to meddling in the U.S. Medical Economy, are gleefully encouraging as many hearings as they can.

If the hearing had value it is this: work on health care, whether that be Medicare for All or changes to the ACA or drug price policy, solidifies Democrats position on those issues and keeps Republicans playing defense. The added value was in the Speaker keeping her word to the restless factions of her party.

What will persist in Washington for the next several months – until one presidential nominee pulls away from the pack – are two realities: the reality of pundits and hearings that makes Medicare for All look like a viable political idea and the reality of lobbyists and think tank members who know the outcome, if it occurs, will be much more benign.

Meanwhile don’t ignore that utilization is up at labs, hospitals and outpatient venues and that fact is immutable regardless of what happens in Washington’s many hearing rooms.

Our Healthcare team maintains its short call on UnitedHealth Group (UNH) with penetration peaking as growth in commercially insured individuals slows. With U.S. economic growth slowing, health care utilization is accelerating putting the inevitable pressure on MLR.