The quarter was decent enough by Wayfair’s ‘will never turn a profit’ standards, but fell far short of what a nosebleed $165 stock needed to see. Rev beat, but it was the smallest in 6 quarters, with upcoming Q guided just ‘in-line’ with investors used to having the growth trajectory pushed higher. You are unlikely to hold a peaky EV/sales multiple doing that. Also, the profit miss this quarter was not expected – as the guide looked very beatable (particularly given management’s borderline cocky confidence on last quarter’s conference call). Oh yeah, W followed it up with a profit guide down for 2Q too. All this is right in line with our Best idea Short thesis that growth is slowing, competitive pressures are rapidly accelerating (Amazon just started an ad campaign touting free shipping on furniture), while management is building an increasingly expensive fixed cost infrastructure for a market that is simply not there – at least not if it wants to earn a red cent, which I do not think will ever happen at this growth trajectory. We see more slowing to come as our view is that throughout 2019, the steepening competitive landscape on top of a slowing Macro environment will take revenue growth expectations down, capital intensity up, and lead to 40-60% downside in the stock.

For our full W Black Book CLICK HERE

Revenue

- US Direct Revenue slowed 60bps from 4Q, that’s 100bps on the 2 year. Guidance at the top end is for another slight slowdown.

- International Direct Revenue slowed 800bps vs last Q, slowing 100bps on the 2 year. Management is blaming Canada for the International weakness saying “we believe there have been some external macro headwinds over the last few quarters in Canada, such as exchange rate and weaker consumer spending”. Management is expecting improvement in growth when it can leverage logistics investments into lower pricing, though we also expect Canadian macro to get better in the upcoming quarters.

- Revenue QTD is just slightly above 40% coming out of the extended Way Day and management’s tone on rev guidance was less bullish than normal.

- This may be the highest revenue bar in the US for W in a while. Guidance on the top end implies a rather large 3yr acceleration (~400bs), with the 2 year re accelerating and the 1 year essentially steady. Punchline, this is the first quarter in years where I don’t think W can easily top the rev target.

Margin

- Gross margins were better than expected up 114bps, though this was against the easiest compare of the year by far. It will be interesting to see if W can keep this trend up as the year progresses, or will margins give way to competitive pressures as we see tougher comparisons.

- Investments continue, with material deleverage on both Advertising and the “Selling, G&A, Ops and Tech” expense lines. CFO noted that ad expense as % of net revenue will decline sequentially. If that simply means the 2Q rate will be lower than the 1Q rate, that tells us very little at 2Q is always a lower rate, and could still mean a big up tick in ad spend growth.

- Castlegate investment continues as well, with the plan for doubling its SQFT this year. It is added cost that is supposed to help drive units and reduce shipping costs, and the margins improve when the units come. Yet keep in mind the value offering for suppliers is lower delivery times(cutting ~5 to ~2 days), while Amazon has already announced its plans to take Prime free shipping to 1 day. Wayfair might need a "KingdomGate" to keep up. It could be long time before we see leverage in logistics boosting the bottom line.

- International margin is still just ridiculous. -25.9% on adjusted EBITDA margin this Q, down 520bps YY. What is the bottom here? -30%? US margin was down 100bps as well.

Other

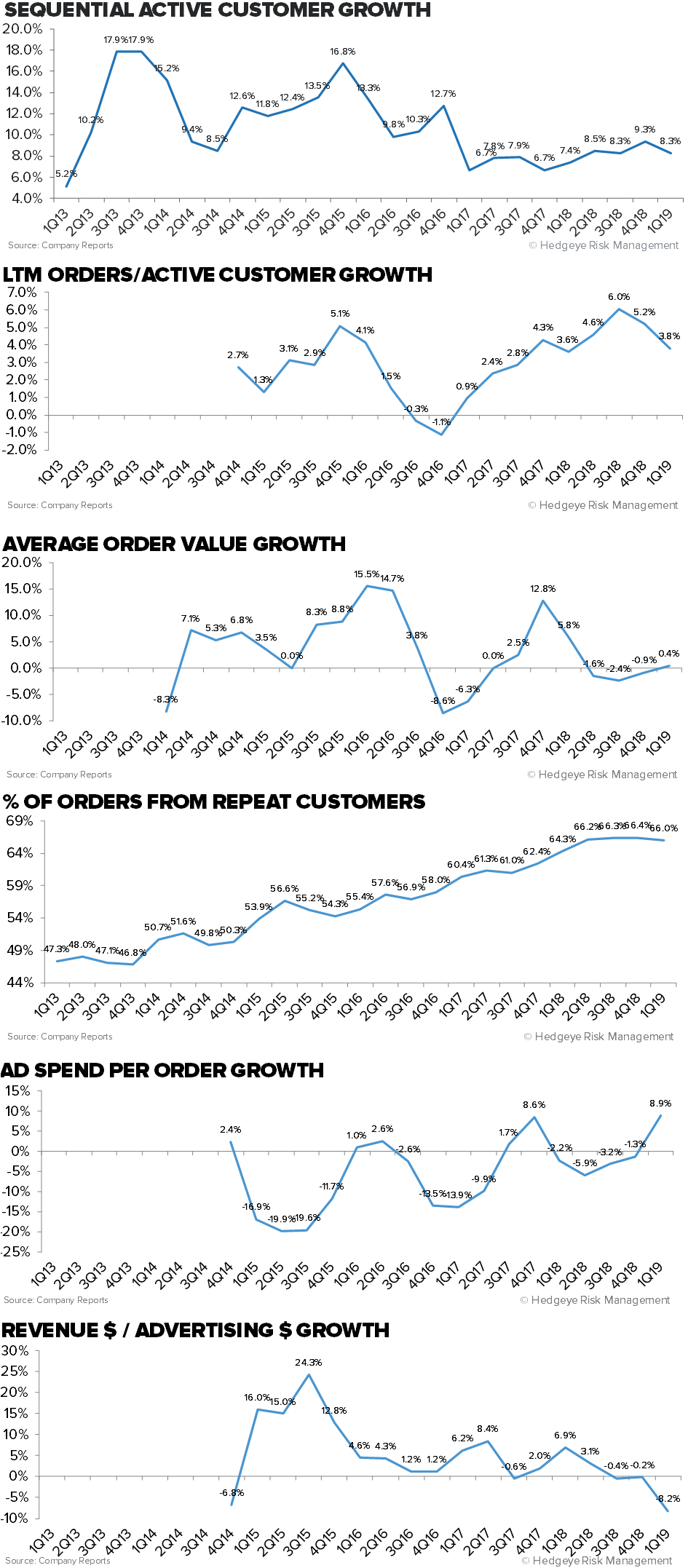

- Orders from repeat customers ticked down QoQ, that’s the first time we have seen that happen from 4Q to 1Q, its happened before but it’s usually 2Q to 3Q. We’re not sure if the read there is bullish or bearish yet, but something to keep an eye on since if the company wants to leverage advertising, we’d expect more repeat shopping over time with less required ad spend.

- With the stock down ~8%, one important thing to remember is that much of W’s business is reliant on a high/increasing stock price. It compensates and incentivizes its employees with shares, and it is how W will raise capital when it’s needed again, which we see as sooner than consensus thinks.