I rarely say this about an HBI earnings event…but this print should be relatively in-line. I don’t expect fireworks, but if I had to pick a stock reaction, I’d say odds are slightly higher of a negative event given retail commentary and Champion interest trends. We’re about 2% below on revenue and inline on EPS at $0.25, down 3% YY. Let’s put this in context – HBI caught lightning in a bottle with the strength of Champion, and EPS is still likely to be down for the quarter and the year. What happens when Champion cools (a process that appears to have recently begun)? HBI remains one of our top shorts, and we’re far more inclined to press it in the high teens after a staggering (Champion-infused) 50% bounce off the bottom. Over a TAIL duration, the company and brand is a survivor, but we think that the overwhelming majority of EV will accrue to bondholders. The downside/upside over a TAIL duration in shorting the equity is extremely compelling – especially with short interest sitting at a two-year low.

KEY ITEMS TO WATCH THIS QUARTER

Revenue

1Q

-The read from retail commentary and other large apparel brands (COLM & CRI saw big growth slowdowns) is decidedly bearish. Weather has been a drag as well as the late Easter pushing sales towards 2Q. The whole world knows this already, but HBI is the furthest from being immune. That should pressure innerwear growth.

-Yet there may be an offset with this odd Michael Jordan promotion. HBI released playing cards commemorating the great MJ Hanes ads. That in itself likely drives little incremental buying, except that apparently 10 cards have been autographed by Jordan. That has created a secondary market just for the card pack, and people may be buying and reselling the cards which otherwise have no interest in buying underwear. We don’t think the impact here is very large, but perhaps it’s a slight tailwind to innerwear growth in 1Q.

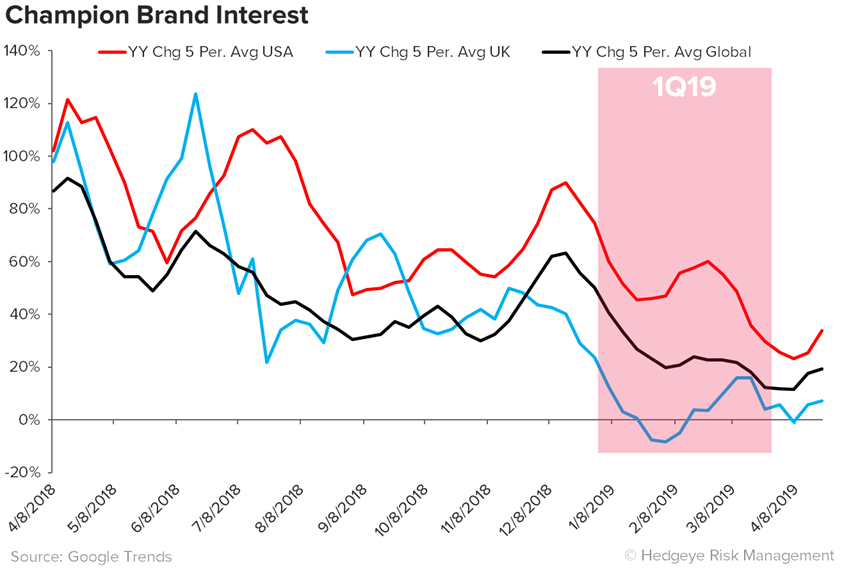

-Champion trends on google look to be weakening on the margin, we’re not sure that means we’ll see a huge slowdown, but think its unlikely the growth gets better vs 4Q. Anything beyond about a 500bps slowdown would like be viewed negatively.

-We lapped the closing of Bras N Things acquisitions in Feb. It should add about $22mm in inorganic revenue. After this we’re back to no acquisitions help. We would not be surprised to see the company do another deal before the year is out.

Looking at the Rest of 2019

-We think the GIL private label launch at WMT is a risk for Hanes. Even with share losses over the last few years the shelf space in WMT had not really changed. It appears with the private label intro Hanes space will be squeezed. Additionally this will be the first time WMT has a private label offering in men’s underwear. WMT will clearly want it to succeed, and that’s a risk for unit velocity of all the other players on the wall – most notably Hanes and Fruit of the Loom are increasingly running faster to stand still.

-Beyond WMT and Men’s underwear private label growth is still a risk, with both KSS and TGT launching new women’s plus sized private label brands, with TGT’s Auden being specifically in underwear.

-We continue to see weaker data points out of Australia on the housing and consumer environment. We think there is real risk of a continued slowdown in the region where HBI has ~13% of revs.

-FX hit is ~250bps to total top line in 1Q. For the year at current rates its 100-150bps.

-Store closures are an ongoing headwind and risk. We haven’t gotten a big bankruptcy announcement since Sears, but total door closures are already projected ahead of last year, and we expect the weakening environment to pressure that. Perhaps the most notable announcement so far for HBI is Family Dollar closing ~390 stores.

-The announcement that PVH is taking on a license to run Nike men’s underwear could be bearish for HBI. Nike’s presence in basic underwear (below the performance compression product) has been rather small. PVH likely tries to grow assortment and distribution for Nike underwear, which could mean some shelf space risk for HBI in stores like a Kohl’s or Macy’s. That might be more of a 2020 risk.

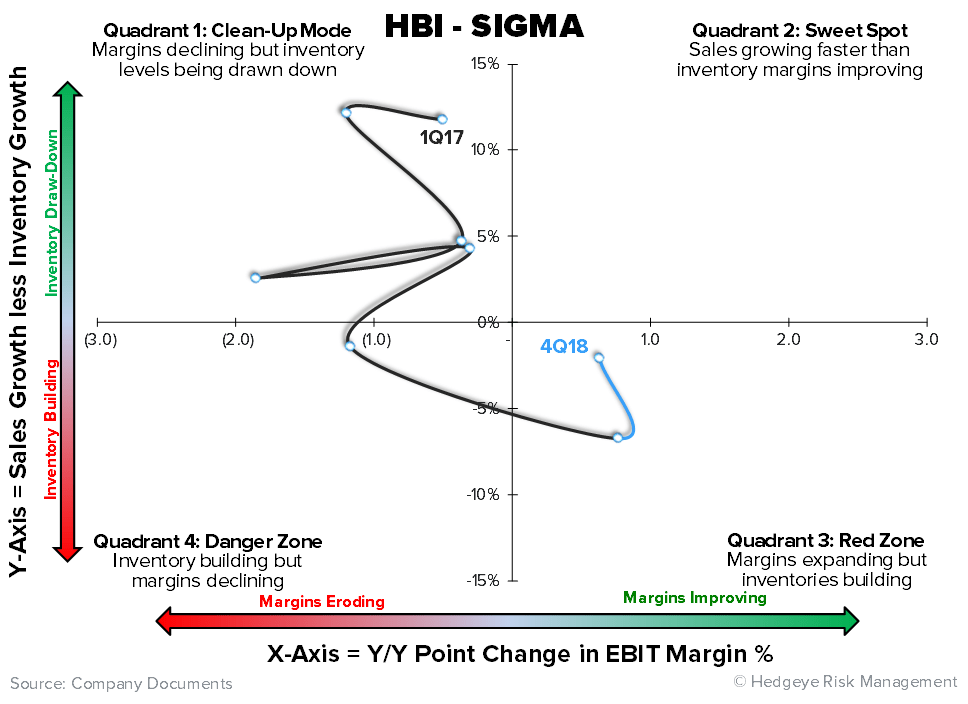

Margins

-As the growth profile looks again to be innerwear down, Champion up, a reminder that the Innerwear decremental margin was 65% last year; the incremental margin of Activewear was 2%. Any growth is coming in much lower margin businesses.

-Cotton is still a headwind this Q, likely 25-50bps. The company is taking some pricing to try to offset at least a portion of that. At current prices it’d be a drag until around start of 4Q.

-Lapping the Bras N Things acquisition is a drag as this business had an operating margin of 22.5% in 2018. So that was a mix margin help, particularly on gross margin, that is going away. Separately, how does that margin go anywhere but down? LB was 18% EBIT margin at the peak.

-The FX drag noted earlier will be a margin headwind as well.

C9 Thoughts

The focus on C9 should grow as the year goes on, as it should. We expect it to comp down more and more as TGT starts re-allocating some floor space before ending the partnership at end of Jan 2020. That’s $450mm at risk.

There is a lot of speculation around whether C9 will exist after the TGT deal ends. We think it’s unlikely another retailer wants a brand that carries as little relevance/differentiation as private label in a category with countless competition (athletic basics).

With that said, we think C9 could exist post TGT, however at a much smaller size (1/4 or less) as few can match the distribution of TGT.

We do not think DKS is interested in the brand (many people have asked us this). DKS is launching a new private label athletic brand this year. That new brand can’t be C9 because TGT has an exclusive license until Jan. It’s unlikely DKS would launch 2 “private label” brands in the same category in a 12 month time period.