Oil prices jumped 3 percent today with Brent testing $75 after the US announced it will not extend Iran oil waivers in May attempting to remove another million barrels a day of Iran oil exports from global markets.

Last November the US granted eight countries waivers from US sanctions on Iranian crude purchases for 180 days. Three of the eight countries had already reduced imports to zero but the other five - China, India, Turkey, South Korea and Japan – were hoping to receive another waiver extension.

The waiver decision presents a conflict for two of Trump’s highest priorities: exerting maximum pressure on Iran by cutting oil export revenues and keeping oil prices in check.

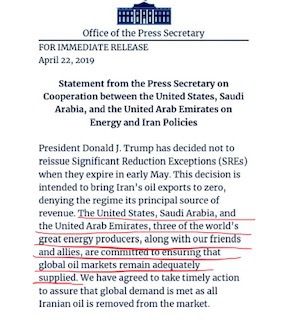

The White House statement today tries to resolve that conflict by relying on commitments from Saudi Arabia and the UAE as well as surging US production in “ensuring that global oil markets remain adequately supplied.” The statement continues “we have agreed to take timely action to assure that global demand is met as all Iranian oil is removed from the market.”

Trump also tweeted Monday morning that help from “Saudi Arabia and others in OPEC will more than make up the oil flow difference in our now full sanctions on Iranian oil.”

The move comes after President Trump spoke to Saudi Crown Prince Mohammed Bin Salman and UAE Crown Prince Mohammed Bin Zayed in the last few days. In addition, Trump was also under significant pressure from conservatives and Iran hawks in Congress to exert “maximum pressure” on Iran and not renew waivers.

However, the US decision will not only mean maximum pressure on Iran but also maximum pressure on oil markets, especially as we head into the high demand summer season. We believe the market had already priced in at least some waiver renewals so the decision is a surprise that is already resulting in a price spike.

The glass-half-full view for oil markets is there is certainly spare capacity with the Saudis and other Gulf allies, in addition to surging US production. But combined with declines global crude stocks and production in Venezuela as well as possible disruption in Libya, a zero-waivers Iran decision will present a challenge to keeping oil prices in check.

In addition, while it is good news there is spare capacity to deal with Iran shortages, the bad news is once the spare capacity is used we will be back to a market with no cushion to deal with other supply disruptions. So bearish spare capacity now will lead to a bullish scenario of little spare capacity later.

Saudi Arabia is already producing about 500,000 b/d less than it is allowed under the new OPEC production cut agreement so it can quickly add new supplies to the market without breaking a sweat.

However, Saudi Arabia made a cautious statement today about “closely monitoring the oil market developments” following the US decision on zero waivers and said it “will be consulting closely with other producing countries and key oil consuming nations to ensure a well-balanced and stable oil market.” It is hard to fault the Saudis for the wait-and-see approach but the market was likely hoping for a stronger statement on additional supply commitments.

China is the big $80-oil-barrel question and one that oil markets will be closely following. Their initial statement today hints on non-compliance but I suspect in practice it will be more nuanced. We think China will further reduce imports from Iran in a nod to US policy but will continue buying Iranian crude in defiance of US sanctions. All of the China issues are wrapped into the larger trade negotiations so we believe the US will give China a pass on sanctions enforcement in the near term.

India we think will largely comply with US sanctions as they arise in regard to both Iran and Venezuela.

The outcome of the Monday’s announcement and subsequent comments by Gulf producers may result in the end of the OPEC production cut agreement when it expires at the end of June. One month ago the Saudis were pushing Russia and others to agree to an early extension of the agreement through the rest of 2019 but Russia would not go along.

We think an extension of the OPEC cuts in June is now certainly in question. We could see a scenario similar to last June when OPEC’s Joint Ministerial Monitoring Committee (JMMC) said it would encourage a pull-back in over-compliance to meet demand after Trump announced sanctions would be re-imposed last May. But OPEC unity and cooperation will be tested in light of the zero waivers extension decision and the Saudi Arabia and UAE roles.

OPEC’s JMMC meets on May 19 in Jeddah, and the next full OPEC meeting is June 25 in Vienna.

As an aside, we note that the White House, for the first time, importantly acknowledges the role US production plays "to ensuring that global oil markets remain adequately supplied" along with Saudi Arabia and UAE, "three of the world's great energy producers." First, we believe it is correct because oil prices would easily be approaching $90 to $100 today if not for the 2 million b/d of crude the US has added since 2017. Second, we think the language is similar to the Saudi public statement about "taking timely action to assure that global demand is met" and will became useful in pushing back on future criticism of Saudi oil market management. Lastly, we think the statement provides the anecdote to the recent NOPEC rhetoric and should put to rest any move by some inside the Administration to support the bill.