Below are analyst updates on our fifteen current high-conviction long and short ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

GTBIF

Click here to read our analyst's original report.

We believe the U.S. MSOs represent one of the best opportunities to make money in the cannabis space. There are a number of regulatory catalysts on both the Federal and State level that will provide tailwinds for them throughout 2019.

We are focused on companies that have been executing on what they set out to achieve. We have done some unique analysis around unit level demographics for individual dispensaries and compared them both against competitors and the state/U.S. averages that we think will be useful and paint a more clear picture of the assets these companies have.

Brands, brands, brands. You hear it all the time in this industry, “we are going to build a national brand!” But who is actually doing it? Green Thumb (GTBIF) is focused on both a wholesale and retail model. They want to provide the best possible experience to the consumer, so supplying both their own, and third-party brands is critical.

Along those same lines, selling their top-notch brands such as rythm and Dogwalkers through the wholesale market to spread their distribution across more doors is core to their strategy. These are brands that have a consumer appeal and a use case that is very apparent, that’s how large CPG companies build brands, so we are confident this strategy will persevere in this industry. Another critical component to our diligence process is corporate governance and focus on shareholder value.

GTI executives are focused on long-term value of their equity, not on taking huge salaries, they are for the most part seasoned executives with secure financial positions. GTI also displayed a solid understanding and respect for four-wall economics, as traditional restaurant analysts this is music to our ears.

AMN | THC | DVA | UNH

Click here to read our analyst's original AMN report. Click here to read our analyst's original DVA report.

Healthcare analyst Tom Tobin was in the studio earlier this week reviewing his Position Monitor, providing key updates and discussing some recent events. As Tobin says:

"The conclusion that #MedicareforAll (#M4A) is the keystone to the Health Care #carnage is a stretch. I don't think we need to begin regressing prices versus Senator Sanders poll numbers quite yet, but a data narrative for the bottom is elusive. What may be more relevant is #M4A as a leading indication of deflationary policies from both the Democratic and Republican sides of government."

Click here to watch the entire webcast with Tobin.

As Tobin discusses in the webcast and we recounted in last week's Investing Ideas update, the Bureau of Labor's employment report recently provides support for our call that utilization continues an accelerating path from the post-ACA deceleration of 2017-2018, positive for significant elements of both our longs and shorts. Tenet Healthcare (THC) looks well positioned as does AMN Healthcare (AMN) on the long side, while the continued upward pressure on hourly earnings appear likely to present a labor cost problem for DaVita (DVA) relative to management guidance.

Ambulance, nursing homes, and free-standing ER continue to be under pressure, although we don't have a great stock to short against those trends. For Unitedhealth Group (UNH), utilization is unlikely to show up in the MLR given the rebate offsets and timing of expenses, but these charts present a credible risk to their "well controlled" cost trend.

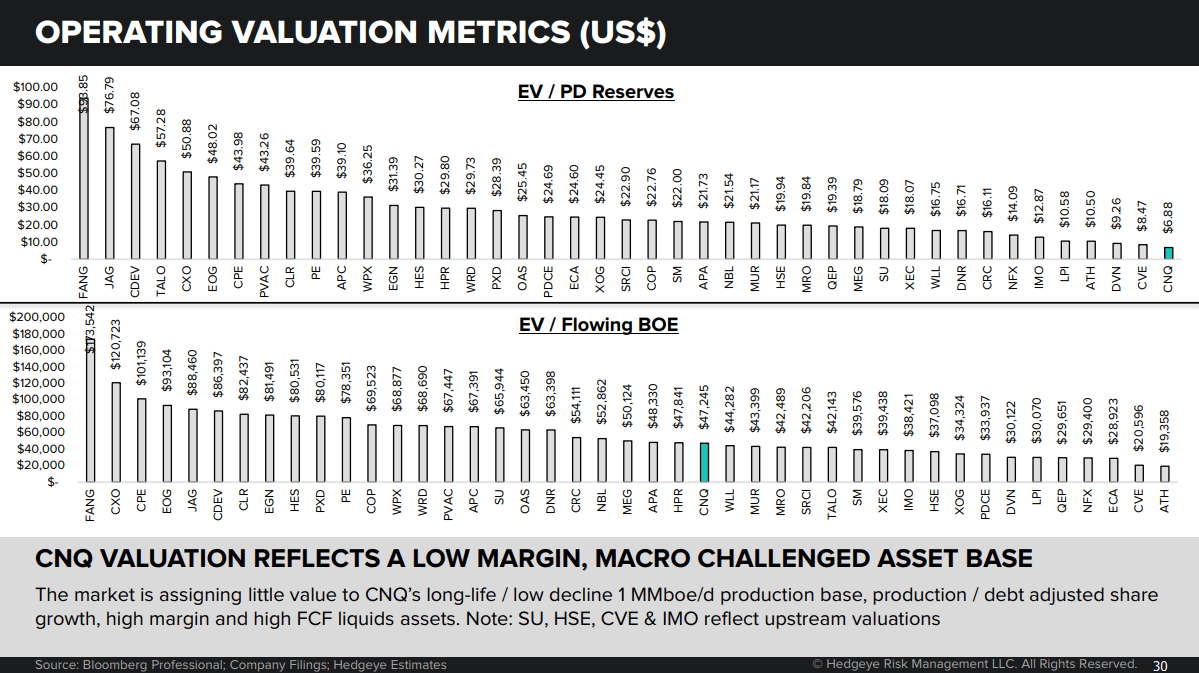

CNQ

Click here to read our analyst's original report.

On a full-cycle basis, after normalizing for each play’s differential environment, Canadian Natural Resources' (CNQ) mining operations are more profitable than many top shale operators. CNQ’s company level margins are better than average, but the company has the ability to flex high-cost capital spend.

CNQ's current valuation reflects a low margin, macro challenged asset base. The market is assigning little value to CNQ’s long-life / low decline 1 MMboe/d production base, production / debt adjusted share growth, high margin and high FCF liquids assets.

ITHUF

Click here to read our analyst's original report.

iAnthus Capital (ITHUF) recently completed the acquisition of MPX Bioceutical, which dramatically expanded their coverage into critical states across the U.S., and making iAnthus one of the premier MSO’s. The combined entity now has access to 11 states with rights to build 63 dispensaries; 20 are operational today, with plans to have 50 open by year end. The acquisition also expands their cultivation and processing square footage by 3x from ~210K to ~600K. MPX brings aboard an already strong Arizona business, which provides an immediate revenue gain. Focus states for iAnthus as they look to continue to expand are OH, MI, PA, MI, CA, IL and eventually TX once things open up there.

WTRH

Click here to read our analyst's original report.

We are bearish on the impact delivery will have on Casual Dining. According to a recent NPD survey, restaurant digital orders have grown at an average annual rate of 23 percent since 2013 and will triple in volume by the end of 2020. NPD says, digital orders have been a source of growth in a flat-traffic environment, yet traffic is negative for the restaurant industry. Here are some of the fun facts from the survey.

- Nearly 6 in 10 digital orders source to mobile apps.

- Restaurant apps dominate, accounting for 12 of the 20 most-used apps.

- More than 1/2 of restaurant visitors participate in a restaurant loyalty program.

- 52% said they would not use a delivery service again if their order arrived at the wrong temperature.

We like Just Eat and Takeaway.com, while in the USA, GRUB has a significant advantage over its rivals. We also like Waitr Holdings (WTRH) which has about 2.0 million active diners across Waitr and the newly acquired Bite Squad. WTRH has an EV of $800 million and revenue estimates of $250 million for 2019.

WTRH is off to a strong start and has a solid management team and backers to become a significantly bigger company.

TGT

Click here to read our analyst's original report.

The departing Target (TGT) CFO Cathy Smith sold $1.6mm in stock a week ago, which = 20k of 52k of common stock shares owned. She has about another 250k in unvested options/stock, though it’s unclear to what extent she gets to retain that in retirement. Selling prior to departure from a company is somewhat common, though we believe she also has low confidence in TGT’s ability to hit full year guidance, since during the analyst day this year she seemed to back away from blessing Cornell’s guidance for the back half of the year. Our read is that she’s uncomfortable with how aggressive he’s being on both the top and bottom line. We think numbers are aggressive as well and see an earnings miss for TGT this year.

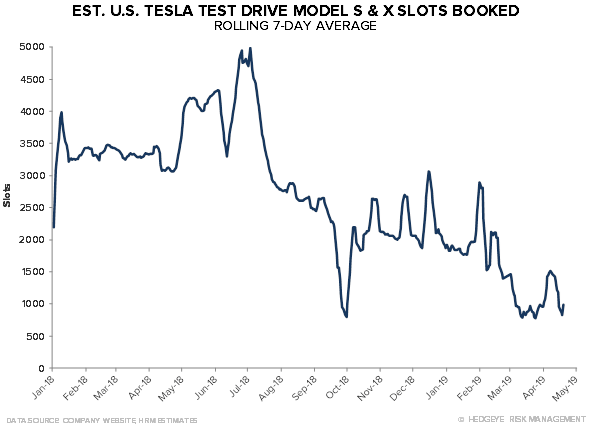

TSLA

Click here to read our analyst's original report.

Our Industrials analyst Jay Van Sciver made his Real Vision debut on “Trade Ideas” last week. In this clip, Van Sciver discusses his short Tesla (TSLA) thesis. Van Sciver examines both the bullish and bearish theses for the company, highlights the unraveling of the demand story in 2019 and reviews just how low he sees the share price falling, in this interview with Jake Merl.

Click here to watch.

No wonder Musk lashed out at the press recently. The emergence of ‘demand limitation’ as a new influence on production (e.g. Panasonic capacity investment) is directly opposed to many new bull theses. For those interested in the self-driving part of Tesla (an asset, we think), the Uber and Lyft IPOs are pushing Musk to get in on the action. We expect the Autonomy Investor Day to be another risky, hastily scheduled disappointment like the Model Y launch. The data say Tesla is desperate to generate some enthusiasm going.

ROL

Click here to read our analyst's original report.

Quality Bias, Or GDP-ish Grower? Rollins (ROL) acquisitions have filled in during periods of weaker organic growth. This is fine, as long as the acquisitions are reasonably priced and successfully integrated with costs accounted for. Pricing has been a key driver of the mid-single digit “organic” growth story. Not customer growth.

The current share price of Rollins makes little sense to us, and we expect a significant downward revaluation by the market.

Margin gains have stalled amid increasing competitive intensity in a mature, slow growing market. Attractive markets for growth and acquisitions present less runway and higher transaction prices.

MCD

Click here to read our analyst's original report.

Since 2010, there has been a clear shift in McDonald's (MCD) SSS away from traffic growth and toward price/mix. MCD average about 2% per year in absolute pricing. Moving the menu toward higher price point items is great for margins but bad for traffic! MCD is no longer the value leader. In the USA, MCD has lost 500 million transactions since 2012. Every percentage point decrease in guest count translates to about 4,500 fewer transaction a year in each store.

TXRH

Click here to read our analyst's original report.

Below are three reasons why we maintain our short call on Texas Roadhouse (TXRH) based on its most recent quarter:

- COGS Inflation – Inflation for the quarter was above expectation due to higher beef prices in 4Q18 and accelerating in the back-half of the quarter. The 2019 outlook is for 1-2% inflation versus deflation for most of 2018.

- Labor Inflation – Wage inflation is looking up 5% in 2019 and hourly turnover is rising YoY. This is one of the key reasons to be SHORT Casual Dining – accelerating labor inflation and slowing sales trends.

- Margins – In 4Q18, restaurant margin decreased 112bps to 15.9%. The change in margin was primarily driven by an increase of 23 basis points in COGS and an increase of 120bps in labor, partially offset by a decrease of 33bps in other operating costs. Coming into the quarter, the street consensus was for restaurant level margins of 17.4% and that is going to be difficult to achieve.

EAT

Click here to read our analyst's original report.

We have been saying for months now that the aggressive discounting at Applebee’s is disrupting the Casual Dining industry.

During the Brinker International (EAT) 2Q18 conference call, the word ‘value’ was mentioned 11 times, and 12-months later on the 2Q19 call ‘value’ was mentioned 38 times. Driving the value proposition for Chili’s is the 3 for $10 platform and we heard yesterday that the program “is a relevant and compelling offer that's sustainable into the foreseeable future.” If this is to be true, what will the margin structure of the company look like going forward?

The bad news for EAT is that all the focus on value is lowering marginal profitability. In 2Q18, on a trailing 12-month basis restaurant level margins were 15.4%, they are now 150bps lower, including the impact of the sales leaseback. We currently don’t see a pathway for margins to improve from current levels and some downside remains if the value promotions continue to gain preference.

PENN

Click here to read the short Penn National Gaming (PENN) stock report Gaming, Lodging & Leisure analyst Todd Jordan sent Investing Ideas subscribers earlier this week.