“Sometimes when I try to understand a person’s motives I play a little game. I assume the worst. What’s the worst reason they could possibly have for saying what they say and doing what they do?”

-Lord Petyr Baelish

When trying to risk manage the motives and machinations of complex systems like markets, assume the worst: Expect her to dispassionately inflict the most damage on the most of amount of people at the same time.

Of course, real-life macro-political dynamics are inherently and eminently amenable to metaphorical Game of Thrones musings.

With cycles & seasons, aspiring autocrats & rogue actors, perennial powers & flagrant inequality, power struggles & anti-establishment uprisings, corrupt ambition & prodigious selflessness, the real and fictional casts are not so easily distinguishable and network audiences and market observers remain similarly transfixed.

Daryl “Joffrey” Jones offered the obligatory GoT mention yesterday but did the courtesy of leaving the heavy metaphorical abstraction to the domestic Macro Maester.

Let’s begin, shall we…

Back to the Global Macro Grind…

A Song of Ice & Fire: Desynchronization characterized 2018 as organic strength and late-cycle stimulus drove the growth and policy divergence that kindled the fire of American Exceptionalism and buttressed the global growth cycle against the conspicuous cooling apparent across EM/China and the balance of global DM. Global Divergences gave way to harmonized deceleration into year-end as the more discrete emergence of global quad 4 conspired with a crescendo in Trade Policy/Fed Policy error concerns and market structure fragilities to push global equites through the Moon Door.

A Feast for Crows (& Doves): The cratering in market prices, an acute deterioration in the forward outlook and the proliferation of geopolitical greyscale forced the Fed to call in its banners in the interest of engineering a globally coordinated Pivot designed to broadside tightening financial conditions and re-suppress cross-asset volatility as part of a larger strategic campaign to reinstate the central bank put and thus reinvigorate the Reflation Trade.

The Small Council: Goldilocks policy is a fickle temptress and marshalling support from all the Great (Central Banking) Houses to push the reflationary agenda requires walking the knifes edge of hero and villain: Too much accommodation risks overheating and an abrupt policy reversal. Too much negative rhetoric around economic weakness (i.e. the reason for the policy pivot) risks the market anchoring on the signaling effect of the message and not the (market friendly) pivot itself.

Moreover, the accommodation cycle is subject to homeostatic constraints. The post-crisis policy regime is one characterized by forward guidance acting as volatility warden with the express purpose of cultivating a self-optimizing, low vol, long carry dynamic to drive asset market reflation. While this dynamic is self-reinforcing and reflexive, it also self-regulates as higher prices and any lagged flow through to confidence and the real economy dampen expectations around further, incremental accommodation.

Thus the ‘bad news is good news’ phenomenon inherently carries a sell-by date and eventually forces a transition and hope for goldilocks conditions to prevail such that ‘good news is good news’ and growth and asset prices remain investible on their own merits.

That remains a tenuous proposition, particularly after the initial, lift-all-boats reflationary impulse has played out. Take China, for example, where we are seeing that push-pull dynamic manifest again currently as strong equity performance and ‘better’ growth data has investors debating whether that means less stimulus and whether that is/isn’t a good thing.

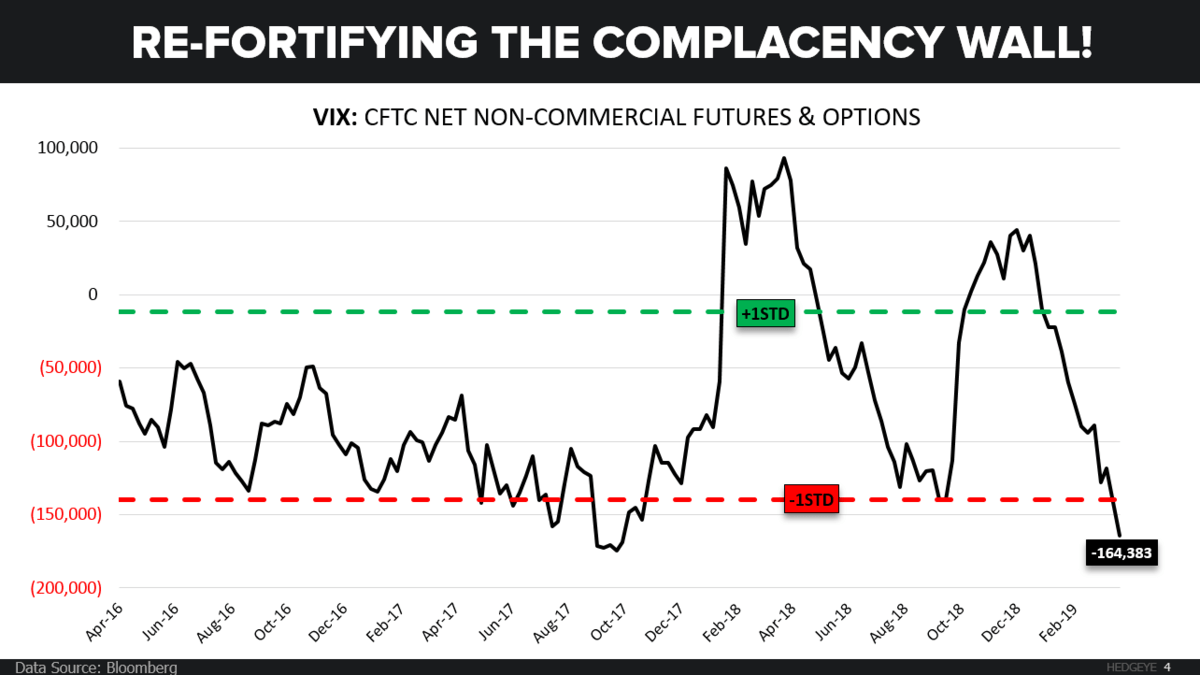

The 7-Pointed (sentiment) Star: With rates and cross-asset vol collapsing, spreads re-approaching all-time tights, implied volatility discounts beginning to pile up across equity benchmarks and the speculative net short position in the VIX again approaching record levels the sentiment vigilantes have re-organized and are again set to march on the complacency wall.

Hodor: YTD domestic equity flows have been underwhelming, hedge fund/CTA equity beta still relatively benign and Powell’s Iron bank is clearly backing House Carry. To the extent investors are inclined to broad stroke the preponderance of high frequency global macro data with the green shoot brush, it carries a distinct probability of further fomenting the FOMO trade, Holding the Participation Door open and last legging equity ebullience a bit higher. This week’s Retail Sales data may offer some green shoot fodder as the notable sequential increase in Auto Sales and gas prices in March (both supportive of nominal spending/headline Retail Sales) and the shift in tax refunds towards March relative to last year/prior years will probably buttress any further deterioration in reported domestic consumerism.

House Stark: Our expectation for Europe & China (& select EM) bottoming in 2019 stands in ‘Stark’ contrast to our view over the past year+. This morning’s acceleration in Eurozone/German Confidence and Construction Activity offer some positive confirmation of the improvement in the March PMI data and provide more evidence of emergent “less bad”.

Eurozone developments parallel the evolution of the Chinese Macro data where the rebound in March PMI’s, the meaningful acceleration in credit growth and progressively easier base effects all support our expectation for a transition to growth accelerating (Quads 1/2) over the balance of the year.

Recall, China bottoming sits as a primary pillar in the stabilization/reflation narrative as it further supports a 2nd derivative stabilization of the Eurozone Industrial/Export economy while also playing the role of soft landing facilitator, cushioning any downside stemming from a deceleration domestically.

The 3-Headed Dragon: Central Banks have pledged their allegiance to Reflationary policy and Quad 4-to-Quad 3 rotations for generations. Remember, the GIP model stands for Growth, Inflation and Policy and none of those factors exist in a vacuum. The “G” and “I” influence the “P” which in turn feeds back and influences the path of both “G” & “I” in a kind of self-regulating, co-dependent system.

In the present instance, policy will not be enough to overcome base effect gravity and stave off a deceleration in growth, but it will succeed in reflating asset and commodity prices, which leads to the rotation from Quad 4 to Quad 3 and a predictable procession of Quad 3 dynamics. The residual drag of dollar strength and oil disinflation from 2018 that continue to flow through the reported inflation data will give way to the converse. And to the extent global divergences re-emerge – with the 2019 iteration being prospective positive divergences out of China/EU – and cultivate dollar weakness, the price effects stand to be amplified further.

The Three Eyed Raven: Gazing across the macro-scape, our expectation remains for a multi-quarter stretch of Quad 3 domestically and, nested with it, an expectation for a more conspicuous emergence of (asset, factor level and sector level) performance dispersion. A protracted period of domestic Quad 3, emergent stabilization in China/EU, and a prospective return to Quads 1 & 2 for the global economy in 2H19 suggest the next large-scale move in the EUR/USD is down … and stretched speculative short positioning in the EUR may serve as wildfire once the rotation gets in motion. Growth, policy and Fx inflections domestically inherently carry derivative implications for EM assets and unlike at the start of last year when we authored the broad-based bearish view on emerging market equity, credit, and currency risk, our current EM call is more nuanced with our GIP model projecting investible divergences across select EM economies. China, Hong Kong and Taiwan being notables.

So that’s where we are both actually and thematically/metaphorically and the discerning among you will have noted the strategic 8 point (season) summary.

The High Sparrow is on vacation this week but our little (process) birds continue to deliver their global macro data whisperings. And we’ll continue to sing their risk management songs, daily.

We swear it by the old market gods & the new.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signals in brackets) are now:

UST 10yr Yield 2.43-2.57% (bearish)

UST 2yr Yield 2.27-2.42% (bearish)

SPX 2 (bullish)

RUT 1 (bearish)

NASDAQ 7 (bullish)

Utilities (XLU) 57.24-58.54 (bullish)

REITS (VNQ) 86.19-88.28 (bullish)

Energy (XLE) 65.35-68.42 (bullish)

Financials (XLF) 26.02-27.27 (bearish)

Shanghai Comp 3099-3292 (bullish)

Nikkei 210 (neutral)

DAX 111 (bullish)

VIX 11.71-15.98 (bearish)

USD 95.70-97.35 (neutral)

EUR/USD 1.11-1.13 (bearish)

Oil (WTI) 60.96-65.19 (bullish)

Gold 1 (bullish)

Copper 2.88-2.96 (neutral)

Christian B. Drake

U.S. Macro Analyst