Below are analyst updates on our fifteen current high-conviction long and short ideas. Please note we removed Amazon (AMZN) from the short side of Investing Ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

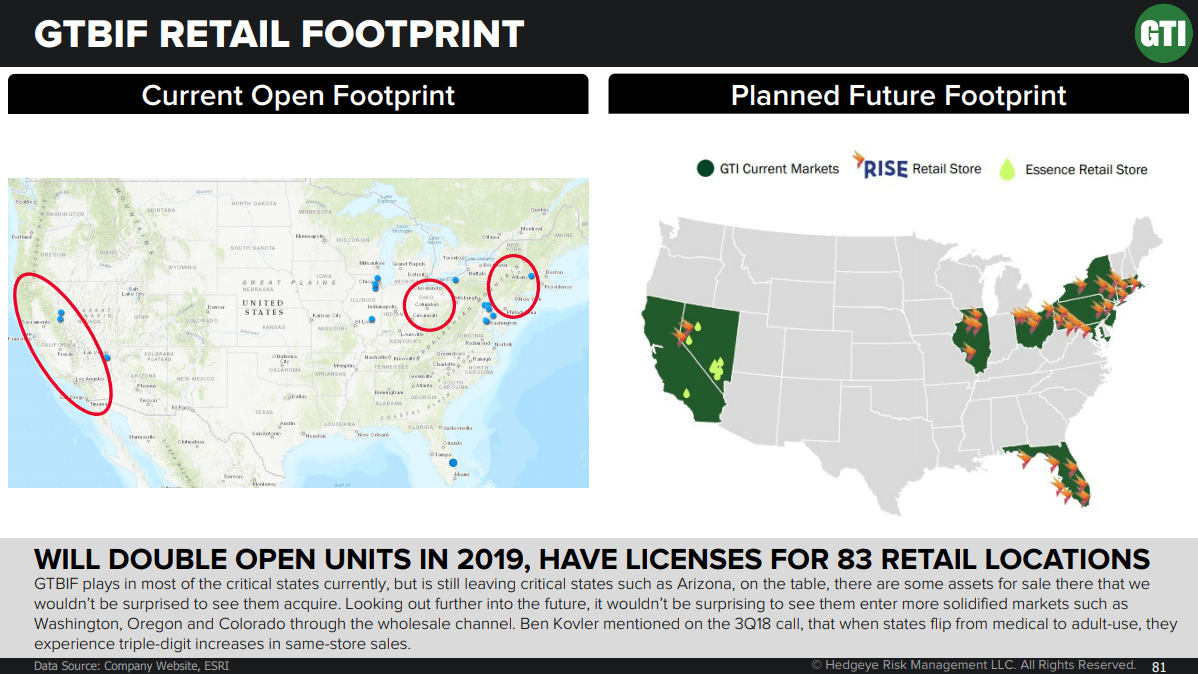

GTBIF

Click here to read our analyst's original report.

Green Thumb (GTBIF) plays in most of the critical states currently, but is still leaving critical states such as Arizona, on the table, there are some assets for sale there that we wouldn’t be surprised to see them acquire. Looking out further into the future, it wouldn’t be surprising to see them enter more solidified markets such as Washington, Oregon and Colorado through the wholesale channel. Ben Kovler mentioned on the 3Q18 call, that when states flip from medical to adult-use, they experience triple-digit increases in same-store sales.

AMN | THC | DVA | UNH

Click here to read our analyst's original AMN report. Click here to read our analyst's original DVA report.

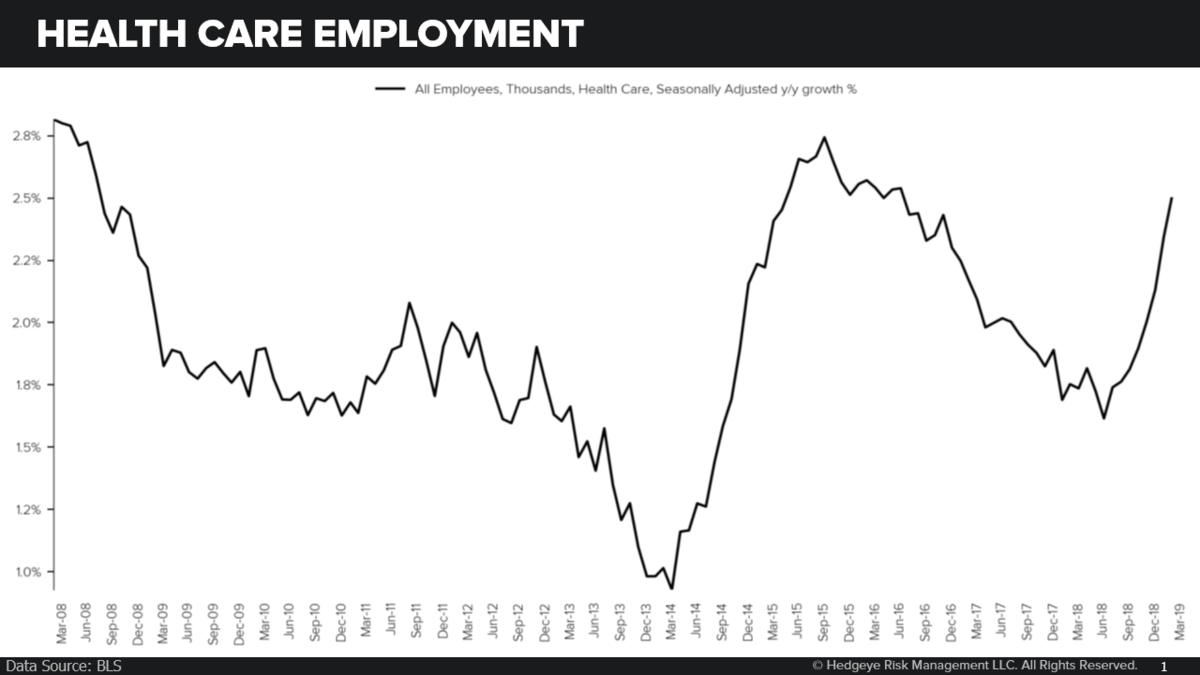

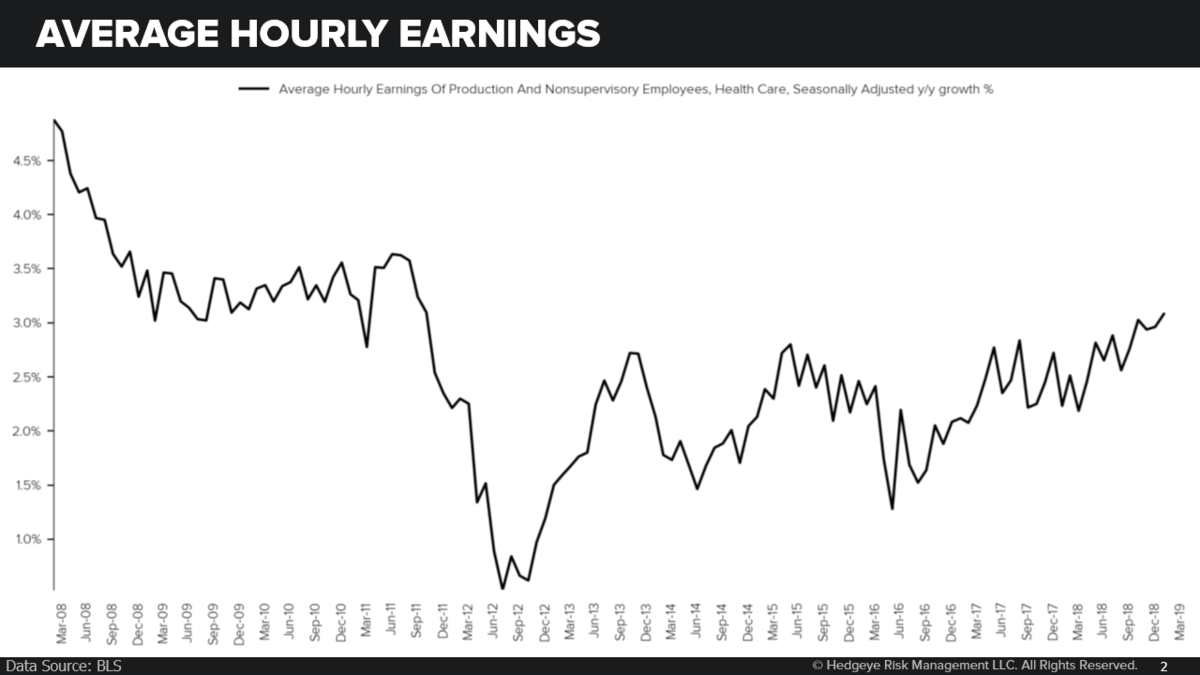

The Bureau of Labor's employment report last week provides support for our call that utilization continues an accelerating path from the post-ACA deceleration of 2017-2018, positive for significant elements of both our longs and shorts. Tenet Healthcare (THC) looks well positioned as does AMN Healthcare (AMN) on the long side, while the continued upward pressure on hourly earnings appear likely to present a labor cost problem for DaVita (DVA) relative to management guidance.

Ambulance, nursing homes, and free-standing ER continue to be under pressure, although we don't have a great stock to short against those trends. For Unitedhealth Group (UNH), utilization is unlikely to show up in the MLR given the rebate offsets and timing of expenses, but these charts present a credible risk to their "well controlled" cost trend.

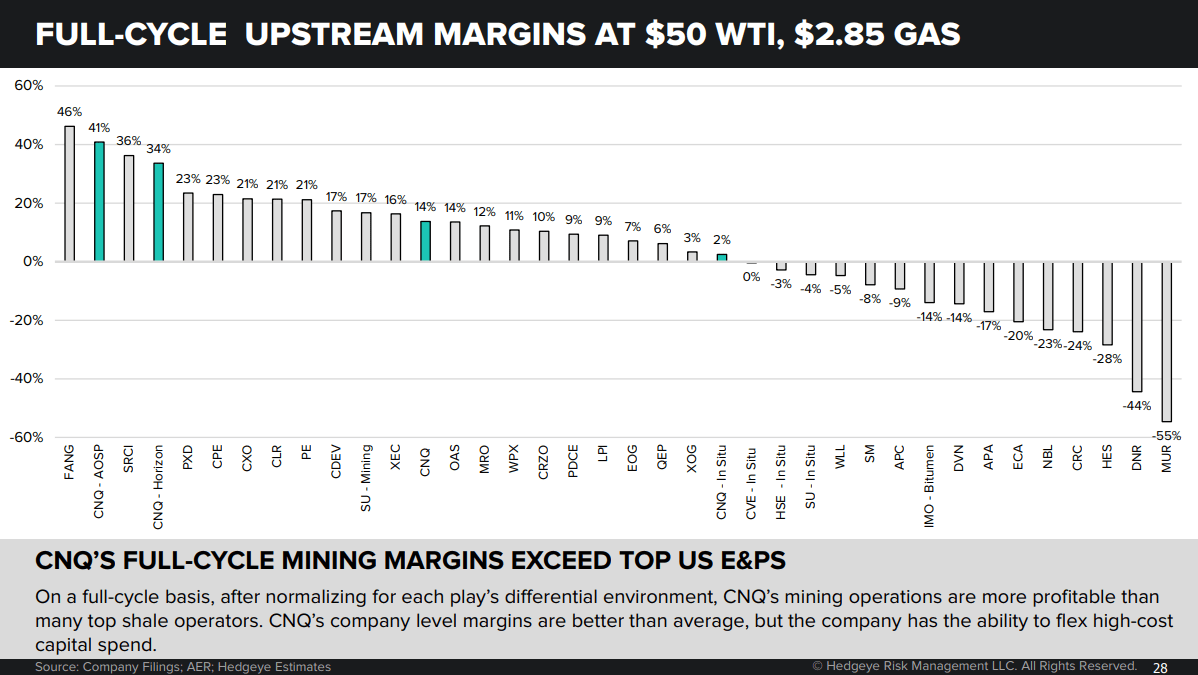

CNQ

Click here to read our analyst's original report.

On a full-cycle basis, after normalizing for each play’s differential environment, Canadian Natural Resources’ (CNQ) mining operations are more profitable than many top shale operators. CNQ’s company level margins are better than average, but the company has the ability to flex high-cost capital spend.

ITHUF

Click here to read our analyst's original report.

2019 is iAnthus Capital's (ITHUF) year to get on track and push forward under one brand. Actual sales have been minimal to date, so their ability to execute will be put to the test in 2019, we are a lot more confident in that ability now that MPX is part of the team, they have done it before! ITHUF CEO Hadley Ford speaks with a focus on ROI and expense control which drives us to believe once they get sales they will be able to ramp up the margin quickly.

WTRH

Click here to read our analyst's original report.

We continue to believe that Restaurant Delivery is going to reshape the restaurant industry in a meaningful way. What that looks like exactly is still to be determined, while some changes will take years to manifest. Nevertheless, massive change is coming to the restaurant industry.

My initial conclusion that delivery is going to be bad for casual dining is unchanged, but it could also make some operators stronger as they work through the issues of profitability on delivery orders. The shifting change will lead to significant growth in chains or companies where the delivery order is not incremental. Meaning, there will be a significant number of “purpose built” concepts that have delivery costs built in to the model. Said another way, this implies that there will be a significant shift away from concepts that were not “purpose built” for delivery.

Waitr Holdings (WTRH) has a strong start with a tablet in every restaurant and local teams on the ground to focus on the convergence of services. WTRH has about 2.0 million active diners across Waitr and the newly acquired Bite Squad. WTRH has an EV of $800 million and revenue estimates of $250 million for 2019.

TGT

Click here to read our analyst's original report.

It’s odd seeing how well some of these stocks have performed given the 1H retail bull case hasn’t come to fruition. That big bull case on retail heading into the year was a big tax refund season and lower gas prices with easy 1Q compares. Yet gas is about a dime from the peak prices of last summer, and this latest tax refund update still shows declines. Total refunds to date (as of 4/5) are down 2.6%, and the average refund is down 1.1%.

Admittedly, the low to mid consumer that shops at Target (TGT) is likely seeing a refund bump, but the aggregate number for total consumption has been a big disappointment so far. If we are following a similar cadence to last year, we should be over 2/3 of the way through refund season. With “weather” and a late Easter likely blamed for any 1Q weakness, management will probably sound bullish on recent trends and 2Q outlook. We might have to wait ‘til summer sales or 2Q misses before we start to see some gap downs in these large retailers, but we have high confidence in earnings misses by the time we hit 2H19.

TSLA

Click here to read our analyst's original report.

Tesla (TSLA) Delivery Miss Evolving Into… Another Miss?!?!

US test drive activity for both the Model 3 and S &X continue to slide, setting up a worse 2Q19 sales environment. How many buyers would purchase a car over the internet, without a test drive, on the hope that it can be returned after 7 or 8 days? How was Tesla’s delivery number adjusted for potential returns (we don’t think it was)? Our Tesla data look UGLY, and right on time.

Closing stores, discouraging sales staff, and obfuscating pricing has had a negative impact on demand, by our read. That the Autopilot/Full Self Driving investor Day was originally scheduled for Good Friday & the start of Passover, and now moved to the day after Easter and the middle of earnings season a week before Tesla’s own (guided down) report.

Most likely, this shows that the Investor Day isn’t a seriously planned, high profile launch. Proving a dubious piece of software, whose promise has been sold for years, is not great theater like a car in space or a next gen roadster popping out of the Semi prototype. Tesla may need to advertise or reduce production, as we see it.

ROL

Click here to read our analyst's original report.

Our Industrials analyst Jay Van Sciver made his Real Vision debut on “Trade Ideas” this week. In this clip, Van Sciver highlights one particular short idea: Rollins (ROL), the pest control company. He analyzes the bear case, notes the deteriorating fundamentals and discusses how to take advantage of the opportunity in this interview with Jake Merl.

Click here to watch.

MCD

Click here to read our analyst's original report.

Having too many points of purchase can overwhelm the employees throughout a system. McDonald's (MCD) is throwing a lot at the 4-walls at once and we believe the initiatives will continue to put serious strain on the operations. Using Starbucks (SBUX) as an example, they added Mobile Order & Pay, but all it did was shift the line to the waiting area because they didn't add capacity. MCD isn't adding capacity either!

TXRH

Click here to read our analyst's original report.

We continue to be broadly short the Casual Dining Industry, and that includes Texas Roadhouse (TXRH). TXRH will be running 3.2% pricing in 2019 vs 1.3% in 2018. The million-dollar question is, can they maintain traffic growth in 2019 with all this pricing? After the company raised prices aggressively in late 2011 and 2012, traffic slowed meaningfully for the next two years. (See the charts below.)

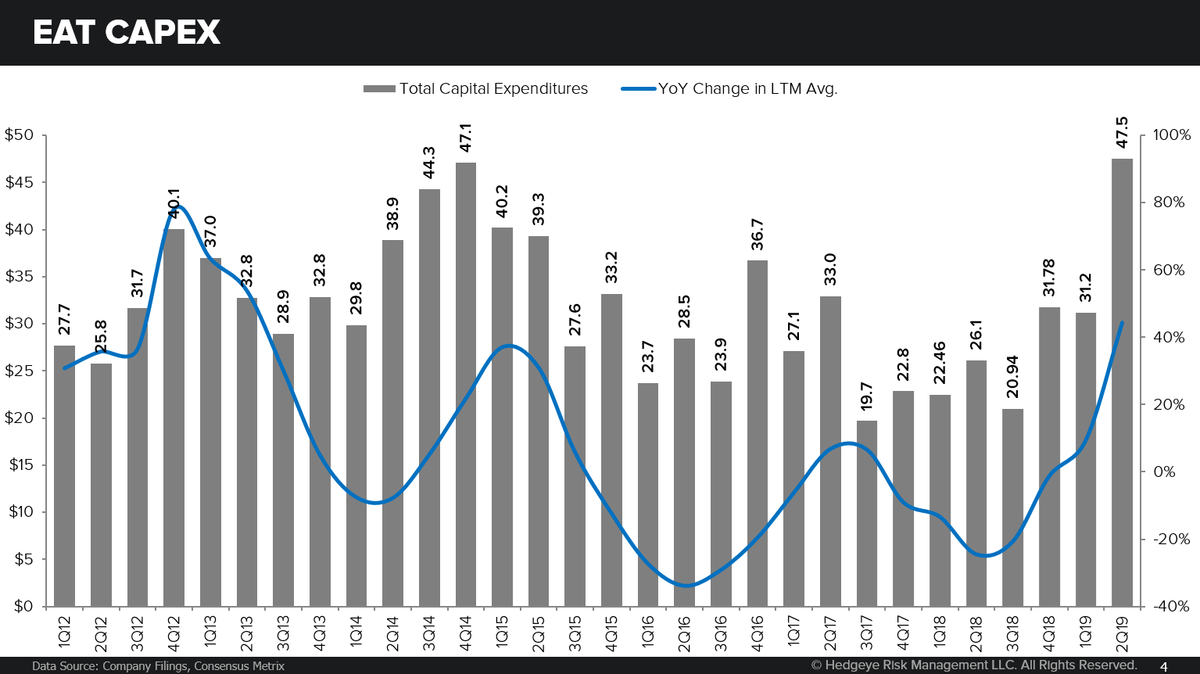

EAT

Click here to read our analyst's original report.

In FY19, Brinker International (EAT) is embarking on a 3-year remodel program, which has some negative implications for the P&L in FY19. In short, expenses are rising without the benefit to the top-line. It will not be until 18-24 months from now where the sales will be growing faster than expenses.

PENN

Even Penn National Gaming's (PENN) solid management team will likely struggle to create value in the current regional gaming environment. Beyond a few near term catalysts that could mobilize this beaten down stock, we see the exact wrong financial structure for a company facing as many secular, macro, and competitive threats as PENN. Many of these threats are unknown or underappreciated by the Street, in our opinion. Given the overwhelming leverage provided by its OpCo structure, significant multiple contraction is possible as investors come to appreciate the impact of flattish and even negative revenue growth.