Below are analyst updates on our sixteen current high-conviction long and short ideas. Please note we added Penn National Gaming (PENN) and Unitedhealth Group (UNH) to the short side of Investing Ideas this week. We also removed Carnival (CCL) from the short side. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

GTBIF

Click here to read our analyst's original report.

We are focusing our long calls on companies that want to build a portfolio of brands, and recognize growing cannabis indoors in northern states is not what they want to be in longer-term. Green Thumb (GTBIF) fits right in that thought process with the desire for their business to be roughly 70% wholesale and 30% retail longer-term (currently their makeup of revenue is flipped). In order to be in the position to dominate the wholesale market in the future, companies need to invest now to win the leading share. We think GTBIF’s prudent approach to capital allocation, while still achieving robust growth, will prove to be a winning strategy. They live by the mentality of: Enter, Open, Scale.

AMN

Click here to read our analyst's original report.

Trends in hospital employment, registered nurse unemployment, and wage inflation, among other data series, suggest we are in the midst of a late cycle acceleration in medical consumption. One of the more obvious ways to play this theme is through AMN Healthcare (AMN), the temporary nurse staffing company.

The U.S. Medical Economy has fully transitioned through the distortions created by the ACA, including the surge in insured medical consumers, followed by the subsequent #ACATaper that appears to have bottomed in 2017. With demand currently accelerating, registered nurse unemployment under 2%, and nurse wages accelerating, we believe upside for both volume and pricing is likely for AMN.

Click here for free access to a complimentary webcast hosted by Healthcare analyst Tom Tobin with insights on companies like AMN, THC, DVA and DXCM.

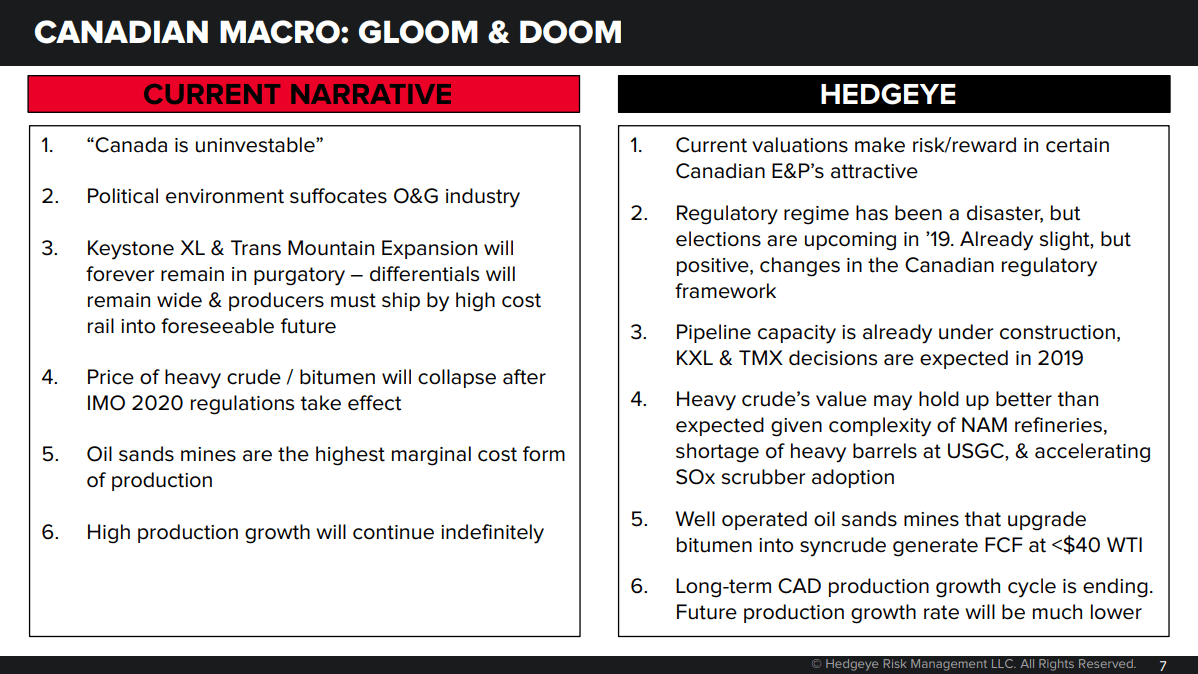

CNQ

Click here to read our analyst's original report.

The Canadian macro environment is becoming more constructive and that should benefit Canadian Natural Resources (CNQ) . Three serious problems have plagued Canadian E&Ps:

- Explosive production growth

- Tight pipeline capacity, and

- A hostile political environment. But there are signs of an inflection.

The last (ever?) oil sands mine is online. In-Situ production growth is stalling with wide differentials and minimal expansion CapEx. Near-term, differentials should ease. The odds of a longer term solution look improved as the regulatory environment becomes better than awful. The Canadian populace is showing signs of fatigue with the current administration.

ITHUF

Click here to read our analyst's original report.

Through their acquisition of MPX, iAnthus Capital (ITHUF) now has a considerable stake in core medical markets across the country, they are also working to continue to penetrate adult-use markets such as NV. iAnthus’ access to higher income households than the average will be helpful to basket size and pricing capabilities longer-term.

ITHUF will be more than doubling their unit count in 2019, with the majority of growth coming from expansion in Florida. Florida will be an interesting market to watch as many MSOs will be going from LSD unit counts to mid-teens/mid-20’s, how Trulieve and Curaleaf will handle the competition will be a good case study for other markets. ITHUF is one of the best positioned MSOs to ramp up their presence in Florida.

WTRH

Click here to read the long Waitr Holdings (WTRH) stock report Restaurants analyst Howard Penney sent Investing Ideas subscribers this week.

THC

The quality of Tenet Healthcare's (THC) assets has been suspect for years, and chronic mismanagement has caused some shareholders to turn activist.

Our THC long thesis continues to call for accelerating volume, in a macro environment that favors domestic health care services exposure. We also like the mix of Ambulatory, particularly USPI, given the positive policy tailwinds.

The company has since made significant progress unlocking shareholder value by improving their asset mix, with a particular focus on ambulatory/outpatient and deleveraging their balance sheet.

Click here for free access to a complimentary webcast hosted by Healthcare analyst Tom Tobin with insights on companies like AMN, THC, DVA and DXCM.

TGT

Click here to read our analyst's original report.

We’re now in calendar 2Q 2019 (1 more month of Target (TGT) fiscal 1Q19), and our Hedgeye Macro team outlined its quarterly themes this week noting we face 3 consecutive quarters of #Quad3 in the US (real growth slowing, and inflation accelerating). One of the worst places to be in Retail in Quad3 is a multiline retailer like TGT, as:

- Inflation pressures COGS

- Slowing growth means prices can’t be passed along to the consumer, and competition accelerates with promotional pressure rising as the retail pie doesn’t grow as fast.

As we progress further into Quad 3 throughout the year, we expect sales and earnings to continue to weaken, when street expectations are for comps improving without margin degradation. After the 1Q report we think there is high risk of EPS misses or guide downs for TGT.

TSLA

Click here to read our analyst's original report.

Tesla (TSLA) Demand Limited Is New, Getting Worse: Tesla’s weak first quarter delivery result is a critical inflection point. It is the first time the company has been clearly *demand* limited. Plans for a production ramp to 10,000 Model 3s a week have gone the way of the 420,000 Model 3s on order. If Tesla can only sell a few thousand Model 3s a week, the thread of the bull mass production story unravels. The logistics excuse provided in the press release doesn’t match the context. The “in transit” number was presumably modified to explicitly include orders; total demand in the quarter (deliveries + orders) was below total production. The “in transit” number also doesn’t disclose an estimate for vehicle returns, presumably a new option for buyers. The flailing on pricing, sales, and referrals fit well with slack demand, not challenged logistics.

ROL

Click here to read our analyst's original report.

Rollins (ROL) shares have strengthened back to near all-time highs following some favorable competitor earnings reports. Our work continues to show signs that the tailwinds behind the pest control industry are fading. Pricing trends in the industry suggests rates have been stretched and may now be facing competitive pressures based on our work. Customer counts have stalled, while revenue per customer has ramped significantly over the past five years following ROL’s pricing study.

Combined with other growth and competitive headwinds, we expect market recognition of pricing and ancillary service limitations to drive a revaluation in ROL shares. We see ROL shares again offering >50% downside.

DVA

Click here to read our analyst's original report.

Since we presented our short thesis in December on DaVita (DVA), things have gone from bad to worse. The 2019 guide included many of our assumptions about rising labor costs and their impact on patient care expense but surprised us to the downside with lower than expected organic patient volume of +0.5 percent. Meanwhile the federal government is looking to open up new channels of patient care and reduce its reliance on the duopoly of DVA and FMS. It all makes us wonder, how bad can it get.

Click here for free access to a complimentary webcast hosted by Healthcare analyst Tom Tobin with insights on companies like AMN, THC, DVA and DXCM.

MCD

Click here to read our analyst's original report.

McDonald's (MCD) just reported its worst traffic count since 2014. Traffic has now declined 5 of the last 6 years, and two of the three years under the current CEO! The stock is doing too well for Steve Easterbrook to get fired, but he is on a short leash.

Slowing top-line will lead to multiple compression. Management is telling the street not to worry about franchisee unrest or negative traffic, and they are listening word for word.

We believe material risk lies within both the U.S. and international markets, that could lead MCD to have negative EPS growth in 2019, that is something that is not contemplated in a peak multiple safety stock!

AMZN

Click here to read our analyst's original report.

Earlier this week Amazon (AMZN) announced plans to slash prices, about 20% on average, at Whole Foods with even deeper discounts being awarded to Prime Members. The news comes just 6 weeks after raising prices at Whole Foods to cover rising costs for packaging, ingredients and transportation.

AMZN likely faced consumer backlash and attrition in response to the initial price hike, forcing the company to compensate by offering even bigger discounts. There is no question, this was a mistake by AMZN, who will now face not only the rising cost pressures noted earlier but also higher customer acquisition costs in its attempt to lure back both new and lost customers.

The are many different angles on what Amazon is doing here, but our view is that it should not be cheapening the store experience and destroying the perceived exclusivity of the business model – but rather should utilize resources to figure out how to actually get same-day delivery right. Amazon reported Physical Stores (mainly Whole Foods) sales down 3% in 4Q18 – showing how AMZN has yet to figure out how to grow stores profitably in sync with its online offering.

TXRH

Click here to read the short Texas Roadhouse (TXRH) stock report Restaurants analyst Howard Penney sent Investing Ideas subscribers this week.

EAT

Click here to read the short Brinker International (EAT) stock report Restaurants analyst Howard Penney sent Investing Ideas subscribers this week.

PENN

Below is a note written by CEO Keith McCullough on why we added Penn National Gaming (PENN) to the to the short side of Investing Ideas earlier this week:

|

Looking for more high quality SELL ideas from my research team that have bounced to lower-highs on #decelerating volume? Todd Jordan remains The Bear on Penn Gaming (PENN) and it's green today. Here's an excerpt from the summary sell thesis (Institutional Research): "Even PENN's solid management team will likely struggle to create value in the current regional gaming environment. Beyond a few near term catalysts that could mobilize this beaten down stock, we see the exact wrong financial structure for a company facing as many secular, macro, and competitive threats as PENN. Many of these threats are unknown or underappreciated by the Street..." KM |

UNH

Below is a note written by CEO Keith McCullough on why we added Unitedhealth Group (UNH) to the short side of Investing Ideas earlier this week:

|

Inasmuch as you should have been looking to add to your favorite LONGS 7-8 trading days ago (when SPY was signaling #oversold), now you should be looking to lay out your favorite shorts. I know that's not how the consensus monkeys on Old Wall TV talk about it (they chase high and sell lower). That consensus is precisely why, over time, this risk management #process works. One of our Independent Research Team's best new ideas on the short side is Unitedhealth Group (UNH). It’s up on #decelerating volume today. Here's an excerpt from a deep dive Black Book presentation (Institutional Research) that Tom Tobin and Emily Evans produced recently: "Our thesis rests on a few simple and well-supported assumptions which produce a mid-single-digit grower at the operating margin line through 2022; materially lower than consensus expectations of low double digits." Sell the bounce, KM |