“There are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.”

-John Kenneth Galbraith

There are plenty of famous one liners about people not being able to forecast either the economy or markets. When it comes to the Old Wall’s complacent consensus forecasts at critical turns in cycles, you better believe those quotes.

When I got fired by Carlyle for being too bearish at the end of 2007, making The Cycle #Slowing call on the US economy wasn’t as easy as it was by the time I did one of my first “public” Macro Themes presentations in Q2 of 2008.

Since the stock market was in bounce mode (ultimately making its final obvious lower-high in May of 2008), at least 90% of the new Institutional clients we were prospecting thought the “charts looked good”, “don’t fight the Fed”, etc.

Many thought I was crazy and/or wrong. Some got really mad at me (I can’t imagine why). Thankfully, some listened to me too. Ultimately, that’s when our story of building this apolitical and independent research firm began.

Back to the Global Macro Grind…

Eleven years later, it’s once again Q2 Macro Themes Day @Hedgeye!

With all the sincerity that you might believe I’m capable of having, I want to thank you for reading my rants every morning and, most importantly, for taking the time to understand our Global Macro Risk Management #process.

No, I’m not going to make the 2008 call this morning. And no, this isn’t about me making the call I did back then either. The people, data, and processes we have on our team now are far more robust than I ever could have been back then.

The biggest thing in common between now and then is that it’s always been about the rate of change of The Cycle.

What we do isn’t about “forecasting” in the linear and deterministic econ way Galbraith appropriately called out. What we do is about now-casting with a non-linear Bayesian inference #process.

It’s all about probability weighing the future. Every day we have an opportunity to change our minds and positions.

Stephen Hawking said: “There is no way that we can predict the weather 6 months ahead beyond giving the seasonal average.” Indeed, Sir Hawking, that is true.

It’s also true that economic TRENDs (The Cycle) have to trend against the prior TREND. That means that:

A) If the base effects of the prior are steepening and the incoming data is #slowing, the probability rises that the economy slows further…

B) If the base effects of the prior are easing and the incoming data is #accelerating, the probability rises that the economy accelerates further

If you want our “white papers” on base effects and why they matter now more than ever, see slides 18 and 19 in the Q2 Macro Themes deck that we’ll publish this morning.

The reason why I’m not ashamed to say that I’ve actually been on the right side of every US economic slow-down in the last 19 years of my career is this basic modeling premise of combining base effects with incoming cycle data.

The easiest cycle call to make in all of Global Macro right now … and I mean all, as in across the 50 countries we measure and map using modern predictive tracking algos (Galbraith and his boys didn’t have those either) is:

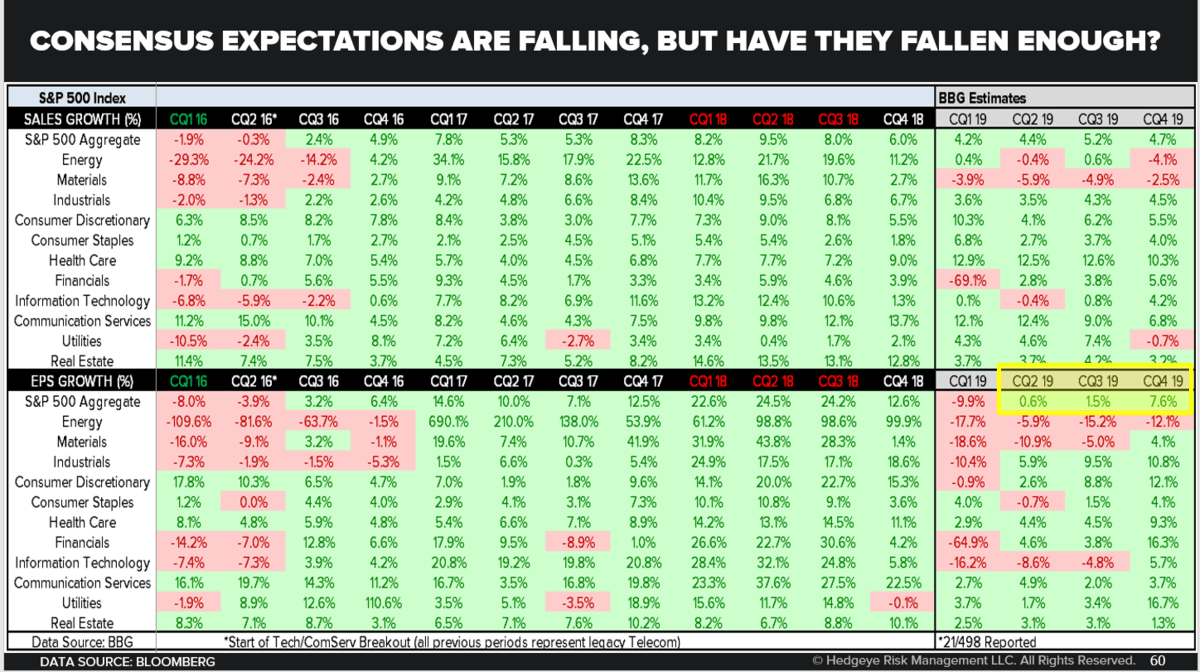

Q2 Macro Theme #2: US #ProfitCycle Slowing

In order to make a bigger “call” (fully loaded with cartoons, eh) we’re going to officially call the Profit Cycle call #ProfitRecession. And that’s mainly because the probability continues to rise that the USA is about to have one.

We define a profit recession as 2 consecutive quarters of NEGATIVE year-over-year profit growth. If you have Perma Bull friends who don’t like that definition, too bad for them. They said they would never subscribe to me in 08 anyway.

Ask them what they’d expect a company’s stock price and/or credit spread to do when that company goes from PEAK year-over-year PROFITS #accelerating to negative year-over-year profits, and they’ll ultimately agree that’s not good.

Don’t worry, as always, every Economic Quad provides the Perma Bulls many things to be long of inasmuch as it provides the Perma Bears many things to be short of. I’ll go through some new Long Ideas on the call as well.

Without further “forecasting” fodder, here’s our brief summary of our Top 3 Macro Themes for Q2 of 2019:

- USA: Three Quad 3’s | In the wake of a harrowing entry into Quad 4 in Q4 and the associated, proactively predictable monetary policy pivot, the multi-quarter rotation into domestic stagflationary conditions is set to begin. While Quad 4 and Quad 3 are both defined by slowing growth, a discrete and extended move into Quad 3 carries specific cross-asset and factor exposure implications. We’ll detail how to risk manage the traversal into Quad 3 and how to best be positioned for a protracted run in that particular regime.

- Profit #Recession │ The confluence of accelerating, late-cycle wage inflation, ongoing deceleration economic growth both globally and domestically, as well as a fading fiscal impulse into peak earnings cycle comps and further, negative strong dollar translation effects are all set to conspire against peak corporate profitability as we move through 2019. We’ll discuss the implications for both equities and credit in the context of an investor consensus that has still not sufficiently discounted the increasingly acute risk to corporate profits in the US.

- Long Ideas: Energy, EM, etc. | New Quad, Same Process. We’ll detail the factor-level, sector-level and global, cross-asset playbook for effectively risk managing local Quad 3 conditions amidst a prospective re-emergence of global divergences in 2H19.

While Bert Lance (Jimmy Carter’s OMB Director in 1977) isn’t remembered as an accurate economic forecaster, he coined another famous quote that applies to my Hedgeye Macro team this morning: “If it ain’t broke, don’t fix it.”

Thanks again for considering our dynamic, data-dependent, and ever changing 4 Quadrant now-casting #process.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signals in brackets) are now:

UST 10yr Yield 2.33-2.54% (bearish)

UST 2yr Yield 2.18-2.39% (bearish)

SPX 2 (bullish)

RUT 1 (bearish)

NASDAQ 7 (bullish)

Utilities (XLU) 57.30-59.24 (bullish)

REITS (VNQ) 85.06-87.95 (bullish)

Energy (XLE) 64.22-67.25 (bullish)

Financials (XLF) 24.89-26.65 (bearish)

Shanghai Comp 3025-3251 (bullish)

Nikkei 206 (bearish)

DAX 117 (neutral)

VIX 12.44-16.93 (bearish)

USD 95.60-97.36 (neutral)

EUR/USD 1.11-1.13 (bearish)

Oil (WTI) 58.66-63.20 (bullish)

Nat Gas 2.55-2.85 (bearish)

Gold 1 (bullish)

Copper 2.81-2.96 (neutral)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer