“For Beijing strategists the prize of gaining a Western seaboard is the stuff of dreams.”

-Tom Miller

For those of you who haven’t yet read China’s Asian Dream by Tom Miller, I’m still recommending you add it to your learning library. The book provides non-US-centric and long-term Global Macro Themes to consider.

As Miller goes on to explain about China’s longer-term economic plans (vs. a 1-month bump in PMI or what Trump is focused on in order to get his “deal” done):

“China’s port at Maday Island is part of a broader plan to develop transport links to China from the Bay of Bengal. Efficiency transport links from Kyaukphyu would enable China to import other raw materials directly, saving a journey of thousands of kilometers.” (pg 150)

Back to the Global Macro Grind…

Welcome to Macro Monday! On the first day of every week I review the week-over-week moves in Global Macro markets within the context of @Hedgeye TREND market signals and research views.

As usual, let’s start with the Global Currency market:

- US Dollar Index was up +0.7% last week to +1.2% YTD and is currently signaling NEUTRAL TREND @Hedgeye

- EUR/USD was down another -0.7% last week to -2.2% YTD and continues to signal Bearish TREND @Hedgeye

- Yen was down -0.8% vs. USD last week to -1.1% YTD and remains Bullish TREND @Hedgeye

- British Pound was down -1.3% vs. USD last week to +2.2% YTD and remains Bullish TREND @Hedgeye

- Argentine Peso was down -3.3% vs. USD last week to -13.2% YTD and remains Bearish TREND @Hedgeye

- Mexican Peso was down -1.7% vs. USD last week to +1.1% YTD and is currently Neutral TREND @Hedgeye

With former “King Dollar” conservative Kudlow begging for the Fed to go dovish for the 4th time in less than 3 months, you might think USD would go down on that. European and Latin American economic data continues to slow though.

Sovereign Bond Yields, globally, obviously get that (or they wouldn’t be crashing to the downside):

- UST 2yr Yield was down another -6 basis points last week to 2.26% and remains Bearish TREND @Hedgeye

- UST 10yr Yield was down another -3 basis points last week to 2.41% and remains Bearish TREND @Hedgeye

- German 10yr Yield was down -6 basis points last week to -0.07% and remains Bearish TREND @Hedgeye

- Danish 10yr Yield was down -7 basis points last week to 0.00% and remains Bearish TREND @Hedgeye

Danish? Yep. I just threw that in there because I doubt anyone else will this morning. I also like the symmetry of a 10yr Sovereign Bond Yield trading at 0.00%. For Treasuries that was the 16th down week (in yields) in the last 21 weeks.

But, no worries, according to another epic bounce in Chinese Equities this morning (Shanghai up another +2.6% overnight), the “bottom is in” for Global #GrowthSlowing despite the USA going into #Quad3 for the next 3 quarters.

Maybe that’s what Kudlow is trying to get ahead of? At any rate, one of the best ways to front-run the Fed going Triple Dovish is to buy both Oil and Energy Stocks:

A) OIL (WTI) was up another +1.9% last week to an eye-popping +29.3% YTD and remains Bullish TREND @Hedgeye

B) Energy Stocks (XLE) were up another +1.0% last week to +15.3% YTD and remain Bullish TREND @Hedgeye

Since “stocks” were bouncing off immediate-term #oversold lows that we signaled at the end of the week prior, the biggest bounces came in Factor Exposures that sold off the most in March:

A) HIGH BETA stocks were +2.0% last week and are down -1.2% in the last month

B) SMALL CAP stocks were +2.4% last week and are down -0.8% in the last month

*Mean performance of Top Quartile vs. Bottom Quartile, SP500 companies

That meant Industrials (XLI) were the best performing US Equity Sector Style at +2.9% on the week, despite losing -1.7% for the month of March. The only Sector Style worse than that was Financials (XLF) at -3.1% for March of 2019.

The other Global #Divergence callout in macro last week came in the performance of Asian and EM Equities relative to the +1.2% week-over-week bounce in the SP500:

- EM (MSCI Index) Equities were down -0.1% last week to +9.6% YTD but remain Bullish TREND @Hedgeye

- Chinese Stocks (Shanghai Comp) were down -0.4% last week to +23.9% YTD and remain Bullish TREND @Hedgeye

- Turkish Stocks were down -6.1% last week to +2.8% YTD and remain Bearish TREND @Hedgeye

- South Korea’s KOSPI dropped -2.6% last week to +6.4% YTD and remains Bearish TREND @Hedgeye

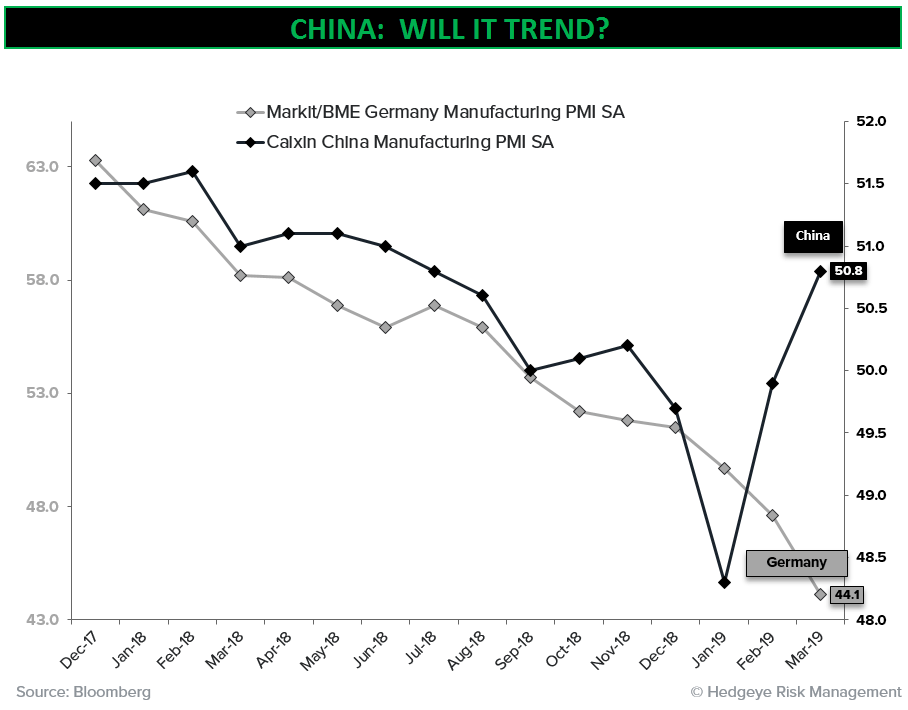

China’s Bullish @Hedgeye TREND signal A) isn’t new and B) hasn’t been confirmed yet by a TRENDING acceleration in China’s economic data. That said, our GIP Model has China going from Quad 4 (for the last 2 quarters) into Quad 2 in Q2.

Is that why China’s PMI #accelerating from its Quad 4 cycle lows to 50.5 in MAR is generating so much excitement this morning. Will it trend? We’ll have to see. As always, we’ll remain data dependent instead of dreaming on that front.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signals in brackets) are now:

UST 10yr Yield 2.31-2.55% (bearish)

UST 2yr Yield 2.13-2.39% (bearish)

SPX 2 (bullish)

RUT 1 (bearish)

Energy (XLE) 64.77-67.59 (bullish)

Financials (XLF) 24.67-26.65 (bearish)

Shanghai Comp 2 (bullish)

VIX 12.93-16.88 (neutral)

USD 95.25-97.38 (neutral)

EUR/USD 1.11-1.13 (bearish)

USD/YEN 109.51-111.21 (bearish)

GBP/USD 1.30-1.33 (bullish)

Oil (WTI) 58.21-60.84 (bullish)

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer