We have been short YUM, which has been the wrong call, particularly into first quarter numbers, which came in better than both sales and earnings expectations. That being said, I continue to have my concerns, largely related to what I recognize

as overly aggressive unit growth in China and profitability issues in the U.S.

CHINA:

The most surprising upside came in China with same-store sales up 4% in the quarter, accelerating 400 bps sequentially from the fourth quarter on a 2-year average basis. Management commented that it benefited from a very strong Chinese New Year during the first quarter on top of trends that point to an improving consumer; though it would not yet call it a recovery. The company guided to a similar magnitude of same-store sales growth in 2Q10 as reported in 1Q10. Relative to YUM’s full year +2% same-store sales outlook issued in December, this implied +3% to +4% 2Q guidance points to upside in the full-year numbers as the company’s same-store sales comparisons get easier for the remainder of the year (management did not revise its full-year guidance).

This 2Q guidance, though it may be conservative, also implies a sequential slowdown in 2-year average trends as YUM is lapping its easiest comparison from 2009. A +4% number in 2Q10 would represent a 300 bp sequential deceleration from the first quarter on a 2-year average basis. Maybe management is concerned that the strong holiday drove a lot of the momentum during the first quarter, which is obviously not sustainable for the remainder of the year, in addition to its concern that the consumer has not yet fully recovered.

Despite the strong first quarter performance, the +14% new unit growth, combined with 4% same-store sales growth, should add up to approximately 18% system sales growth. YUM China reported 15% system sales growth which highlights a decline in new unit AUVs. In response to a question during the earnings call, management stated that there is a $300K gap between new unit AUVs and the rest of the system, which it attributes to the fact that the company is opening in smaller cities which generate lower sales but also require a lower cost structure. This will be an important trend, although not new, to monitor because lower new unit AUVs is typically a sign of growing too fast and cannibalized sales.

U.S.:

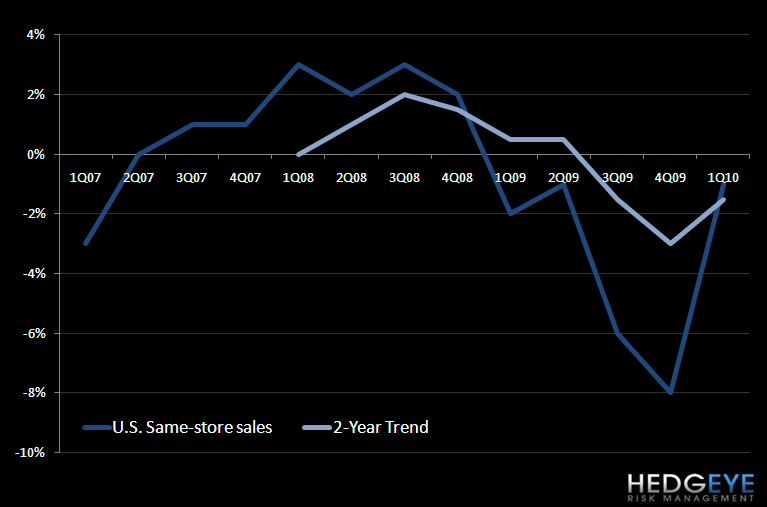

U.S. same-store sales of -1% showed marked improvement from the -8% in the fourth quarter. Pizza Hut led the charge with same-store sales up 5%. Management attributed the strong sequential recovery at Pizza Hut to its “$10 Any Way You Want It” pizza promotion. This promotion hurt average check, which was down 10%, but more than offset it with increased transaction growth, according to management.

Although we knew trends had improved at Pizza Hut, as reported earlier by NPD, the 750 bp sequential improvement in the 2-year average trend was impressive. Despite this better top-line performance and $5 million in commodity deflation, operating profit declined 9% in the quarter. Although same-store sales comparisons get easier in the back half of the year after lapping the Kentucky Grilled Chicken launch from 2Q09, the commodity benefit is expected to go away and turn inflationary as we trend through the year as management is expecting costs to be relatively flat for the full year. In addition, the operating profit growth compares get more difficult for the next two quarters as the company benefited last year from implementing a $65 million reduction in its U.S. G&A cost structure.

It is also concerning that more consumers at Taco Bell, YUM’s most profitable U.S. concept, are buying from the “Why Pay More” menu. This, combined with the need for promotions at Pizza Hut that drive average check lower by 10%, will put increased pressure on U.S. profitability. Despite easier same-store sales comparisons in 2H10, I do not find much comfort in management’s comment that it is comfortable with its full-year 5% U.S. operating profit growth outlook as the company consistently misses its U.S. operating profit targets. To recall, YUM’s initial 2009 U.S. operating profit target was 15% and it came in at +1%.

All in, the first quarter was a strong start to the year for YUM. To that end, I think it will be difficult for the company to maintain this momentum for the following reasons:

- China’s margin performance of 1Q won’t continue - Expect moderate year-over-year improvement over China’s 21% margins in Mainland China last year

- Commodity inflation is expected in the back half of the year (reported commodity deflation of $15 million in 1Q10)

- YUM is facing increased wage inflation in 2H10 after facing lower than usual wage growth rates in 1Q10

- YUM is facing its most difficult U.S. SSS comparison in 2Q10 as it laps the Kentucky Grilled Chicken launch, which drove KFC comps positive for one quarter

- U.S. operating profit growth comparisons get more difficult for the next 2 quarters and commodity deflation with likely turn inflationary

- After tax results will be challenged in the second quarter as the company laps the favorable 16.4% effective tax rate from 2Q09

NOTES FROM THE YUM 1Q10 CALL:

On the way to achieving 9th straight year of double-digit EPS growth

- Worldwide 1Q operating profit grew 17%, EPS grew

- China division’s profit grew 37%

- SSS growth and unit growth

- U.S. sales improved also, particularly PH

- U.S. profits down 9%, SSS declined 1%

- YRI system sales increased 1% and profits increased 2% prior to FX

- Driven by new unit development

Overall, pleased with the start to 2010.

CHINA

Continue to build leading brands

- SSS grew by 4%

- Units grew by 14%

- Rest margins at 27%

- Profit growth of 37%

- Lapping 30% profit growth in 1Q09

New Unit development is the major driver of growth

- 96 units opened in 1Q

- Surpassed 3,500 units

- Leading position in China

KFC

- 1.4m dollars AUV per year

- Delivery is now available in over 110 cities

- Developing sales layer now over 3% of sales

- Breakfast represents 7% of transactions and continues to grow

- Nearly 3,000 KFC units in over 650 Chinese cities

Pizza Hut

- Leading western casual dining concept in China

- Double-digit SSS growth

- Menu appeals to Chinese consumers

- Updating 25% of menu every six months

- PH has 467 units in 122 Chinese cities

Other minor brands also gaining traction

YRI

Strategy is to aggressively expand

- New unit development is a key driver

- 109 openings in more than 40 countries during 1Q

- Network of 1,000 franchisees

- Goal of 900 for year

- SSS declined 1%

- 2% op profit growth excl FX

KFC

- Expanding value menu to more markets using proven strategies

- Incremental sales layers

- KFC breakfast – KFC AM continues to grow

Pizza Hut

- Everyday affordable prices

- Weaker transaction trends due to check but menu is being changed

France, India and Russia delivered 14% system sales growth prior to FX in 1Q10

- KFC expanding aggressively in these markets

- Provincial cities

- In Russia, 150 KFC units in 22 cities

- In India there are 74 KFCs in 14 cities and 159 Pizza Huts in 33 cities

- KFC is leveraging television advertising to build brand awareness

Two new Taco Bells opening in London

UNITED STATES

Strategy is to improve brand and returns

- Pleased with improvement from 4Q09

Pizza Hut

- Promotion has helped bring people back

- Check was too high

- Going from Pizza to Pizza, Pasta, and Wings

- Turned corner on sales trends

Taco Bell

- Disappointed with -2% decline in SSS as people increasingly traded down

- Pipeline of products is strong for the rest of the year

KFC’s performance improved sequentially

- Balanced options – fried and grilled chicken

- Portable options – double down

- Improved operations

- Performance has improved from 4Q and company expects this to continue

Took a non-cash charge that basically reflects the beginning of refranchising KFC to 5% company ownership. That is also our goal for Pizza Hut, where we’ve already begun the journey and are well on our way.

Chief Financial Officer

1Q results

- Strong Chinese holiday

- SSS of 4%, system sales growth of 15%

- Consumer confidence in China has improved yoy the past three months

- Benefitted significantly from chicken cost inflation vs prior year and lower-than-usual wage inflation

YRI

- Sales results weak in developed markets like Japan and Canada

- Dampened overall results for YRI’s quarter

- Only 2% profit growth prior FX

- Post FX growth was 13%

United States

- Unemployment and discounting environment is difficult

- Taco Bell experienced higher Why Pay More mix and had lower drink incidence

- Reduced G&A by 6m dollars

Outlook for 2010

- Expect moderate SSS growth in China in the second quarter

- For the U.S. expected that positive sales growth will come in 2H10

- Comps easier in 2H

- China’s margin performance of 1Q won’t continue

- Commodity inflation in back half and a bigger impact from wage inflation

- Expect moderate year-over-year improvement over China’s 21% margins in Mainland China last year

- After tax results will be challenged in the second quarter as a favorable 16.4% effective tax rate before special items is rolled over

- Confident that 10% EPS objective will be met

Strategy for emerging markets

- Significant growth opportunity

Emerging markets – China, Indonesia, Malaysia, India, Brazil… collectively there markets are growing at a fast rate. Long runway for restaurant growth in those countries. Further, in top ten emerging markets, YUM has 1.5 units per 1m people.

- 10,000 units in emerging markets. 55% of YRI + China units. Larger than peers in these markets and growing fastest.

- 2x MCD’s emerging markets presence. Most of YUM’s competitors aren’t even opening in emerging markets.

In upcoming calls and investor meetings, YUM will provide more color on these emerging market strategies.

Q&A

Q:

Pizza Hut value…what is the impact on mix from the $10 promotion. How are you thinking about sustaining value there going forward?

A:

Posted strong sales in 1Q of 5%. Addressed the biggest problem, which was value. Comparable margins have held steady. Flow through has offset the drop in price. Brand is improving as a result of the initiative. Working hard with franchisees on sustaining compelling value.

Check was down about 10% but transactions increased at a much faster rate.

Q:

How are you responding to the consumer’s reaction to shrimp taco?

A:

People like it. We have some product supply issues because the shrimp tacos flew off the shelves. Made a lot of sense to have it during lent.

Q:

Detail on consumer environment in China…your results were strong, what is giving you pause in calling for the recovery in the Chinese consumer?

A:

Consumer confidence has gone up the last three months but still below where it was a year, year-and-a-half ago….(but they are up year-over-year?). Other metrics are positive. We are focusing more development on the stronger regions (coastal regions are not recovering as fast).

Q:

Seen anything from 1Q to suggest that low-to-mid single digit comp is unsustainable for the rest of year?

A:

No significant change from 1Q levels as yet.

Q:

The profit for 1Q was down domestically, food costs aren’t going to help going forward, how do you feel about the U.S. business, profit-wise for the year?

A:

Overlaps get easier in the second half of the year. Not assuming a great economic recovery for domestic business to get better. Things are better than they were in 3Q, 4Q last year. On the commodity side, there was some deflation in 1Q. Current guess is that it will be flat for the full year. Value, product, and managing costs are the three key focuses at our domestic brands.

Still comfortable with 5% growth in U.S. outlook

Q:

Pizza category in the U.S., who are you taking share from? Is it sustainable?

A:

More competitive on the pricing front. Usually when YUM grows like it is right now, it comes from overall category and the “mom and pops”.

Q:

You have been running without menu pricing in China for at least six months, what’s the new opportunity in coming quarters, especially if there is inflation in 2H10?

A:

Labor and costs were unusually low but we’re studying what we want to do now for the back half in terms of costs.

Q:

Update on KFC U.S. business. Last quarter some of the franchisees were behind in royalty payments – has there been improvement there?

A:

Bad debt did a little better in 1Q. Hopefully we get in to a better seasonal time now.

Regarding refranchising, we’re on a three year refranchising program that really started in ’08. In the first two years of that,

Long John Silver was fully refranchised.

KFC continues to be the biggest challenge in the US. Likely will be negative in 2Q as grilled chicken is lapped.

More innovation around “balanced” and “high-end” opportunities.

Q:

YRI, why have sales remained soft in key markets like Australia and the U.K.?

A:

Australia has had a strong run of consistency. Pipeline and innovation has fallen behind. Expect that business to perform better. The brand is strong there. In the U.K., pleased with the progress of KFC which had a great year in 2009. Pizza Hut is big challenge there, not affordable. In the early days of making a substantial change there.

Q:

What kind of comp do you need to offset coming increases in fixed costs?

A:

In 2H09 the government didn’t take up minimum wages. In 1H10 Yum is benefitting from that. In 2H the company will be impacted by that. For the full year there will be a moderate increase. A modest comp is required to offset that.

Normally wages in China are in the 8% to 10% level. Rates were lower than that in the first half of the year but will be higher for the balance. Should average 10% for the full year.

Q:

All of the publicly traded pizza players saw big improvement in comps. Is there any other place you can get market growth from? One of your competitors said that market has been declining but it now ticking up?

A:

There’s nothing like the power of having the leading brand. When you’re value competitive, your odds are better. We’re trying to have a two-fold strategy. One is to compete better in the pizza market value-wise. The other is to leverage variety – pasta and wings being added into the equation and marketing them primarily during the week.

Q:

China, new unit volumes. Are we still looking at 200k difference in new unit volumes? What is the ramp for new units?

A:

AUVs are 1.4m and new units come in at 1 or 1.1m. That trend has been intact for a while. As you get to the smaller cities, margins are similar despite lower sales because cost structures are lower there.

Q:

U.S. Taco Bell business. Can you talk about the -2% comp and the lower level of drink incidence?

A:

Lower average guest check. Less drinks and combo meals. Most media spend was on the value side. The “why pay more” usage was a higher portion of mix. More and more people are at the low end. We did have positive transactions and we can build off that strength.

Biggest challenge is to get SSS going. Easier to build off positive transactions. Also extremely enthusiastic about results from longer term initiatives. Optimistic about the future of the brand and TB can get modest SSS growth for the balance of the year. Sales layers being added will help TB become a net new unit developer.

Q:

SBUX, MCD, DPZ results seem much better internationally. If there’s anything that’s going to change from a management perspective, remodels…can you give color on that? Can you also comment on company store margins in the YRI division?

A:

No question that YRI has problems that need to be addressed. Focused on value. Looking at value menus that have been successful in South Africa and expanding into U.K.

Rolling out incremental sales layers. Frozen beverages….

Hoping for a better second half in 2010.

Q:

Any benefit from New Year being in February as opposed to January?

A:

No dramatic shift between Jan and Feb. Was check flat and transaction up 4?

Q:

Internet coupon deal that went awry in China?

A:

Couponing error caused some concern among customers, short term issue.

Q:

Cost for YUM in terms of healthcare? Any push back in refranchising?

A:

Small impact this year but the major impact of the legislation will be in 2014. We’re going to 5% ownership of KFC and PH. Lots of legislative details to be ironed out. Will cost $15k per store starting in 2014. Plenty of time to deal with the issue.

Q:

With comps up 4% in the first quarter that was versus a +2%. In 2Q last year it was down…can you drill down deeper and tell us why the trends won’t accelerate. Anything in 1Q that isn’t flowing through?

A:

Looking at it in terms of 3, 2, or 1 years is not the point. We expect moderate growth from 2Q last year.

Q:

Corporate expenses were down this quarter…is this $30m per quarter run rate to be expected going forward or was it unusual?

A:

U.S. saw a reduction in G&A. Goal is to offset refranchising costs with G&A savings.

Q:

Is the $10 price point important to keep for PH? Even with a change in toppings…or is the variability of getting whatever you want more important? Separate occasions for pasta and chicken or bundling?

A:

Relative value is the real key here. More into separate occasions than bundling.

Howard Penney

Managing Director