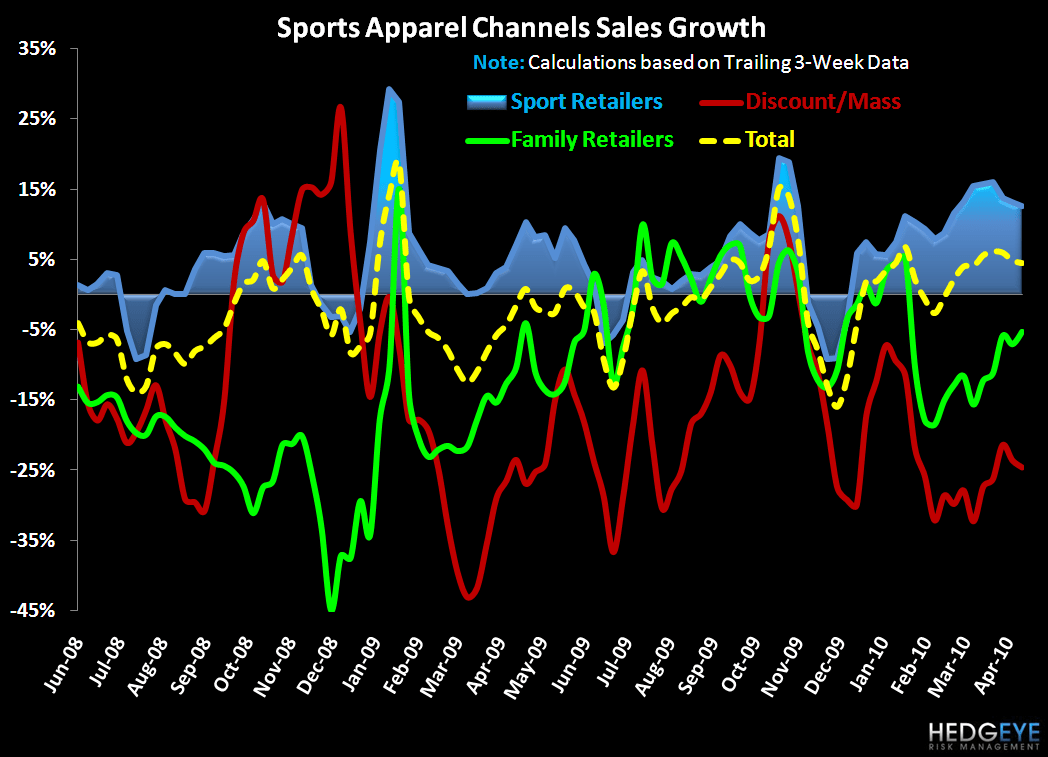

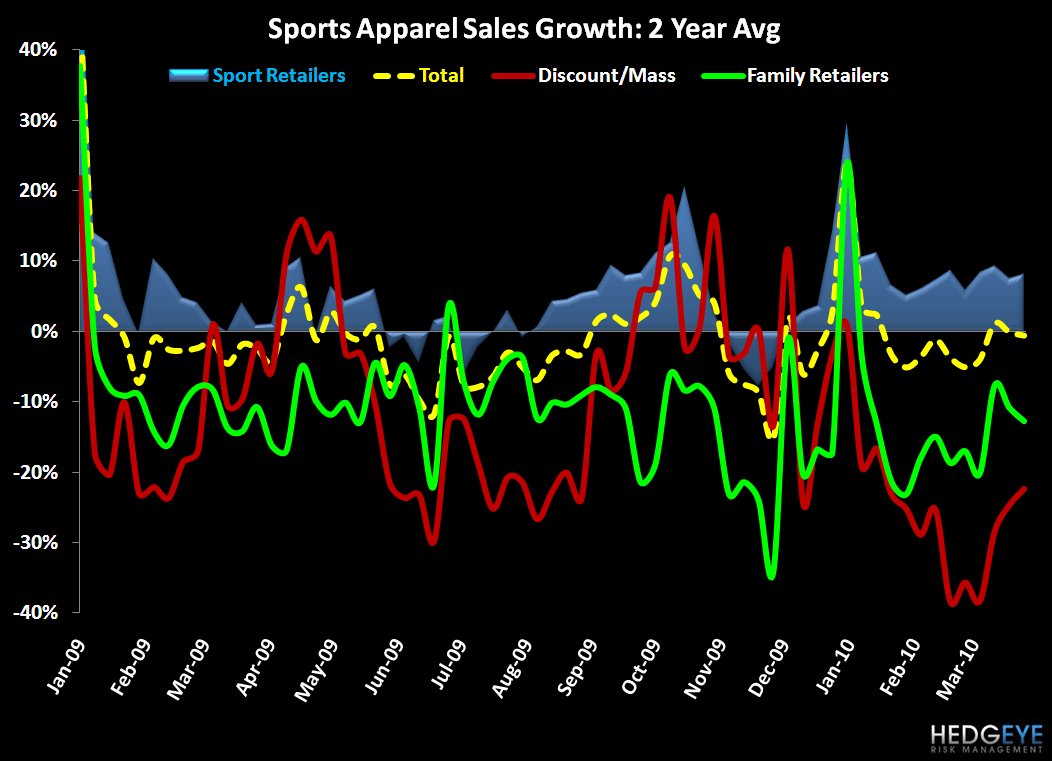

Nike Outperforms During Modest Slowdown in Sports Apparel Industry

Sports apparel sales slowed modestly after last week’s surge. NKE stands out as a clear outperformer as the only company that grew sales on a sequential basis.

This week’s industry data reflects a modest slowdown in sports apparel with total industry sales up 3.9% vs. the 5.7% increase last week. Weakness was driven by a deceleration in the Athletic Specialty channel, which slowed from 15.8% to 10.8% while both Discount/Mass and Family retailers improved on the margin. At the same time we continue to see a divergence of ASP trends in the athletic specialty and family channels. Both Mid-Atlantic and South-Atlantic regions had a strong week backed by warmer weather while portions of Mid-West experienced more precipitation than normal hampering sales.

Nike stands out as the clear outperformer for the week as the only company that grew sales sequentially accelerating share gains from 460 bps to 560 bps y/y driven by basketball and running. Outdoor and outerwear categories dropped off this week and significantly dropped Columbia and TNF’s sales growth rates.