|

MARKET WATCH: What’s Happening? Companies in low-growth industries are turning to the pet care market as their next big source of revenue. Why? Pet ownership and expenditures have recently been accelerating—and today’s pet owners are spending more per pet than ever before on everything from premium pet food to pet insurance. Our Take: The pet care boom won’t likely end anytime soon. Boomers were the first to humanize pets and take care of them like a member of the family—a new relationship with pets that has triggered a big recent rise in senior pet spending. With younger generations following in their footsteps, the industry will prosper. |

Last month, private confectionery company Mars purchased animal hospital operator Veterinary Centers of America. This is only the latest example of a CPG firm buying up a pet-related company. Back in 2014, Mars took over Procter & Gamble’s mainstay pet food brands (in all markets except Europe): Iams, Eukanuba, and Natura. In 2015, J.M. Smucker Company (SJM) bought Big Heart Pet Brands—maker of Meow Mix, Milk-Bone, and Kibbles ‘n Bits—from Del Monte Pacific Limited. And earlier this year, Archer Daniels Midland Company (ADM) acquired Crosswind Industries, a major supplier of pet food ingredients.

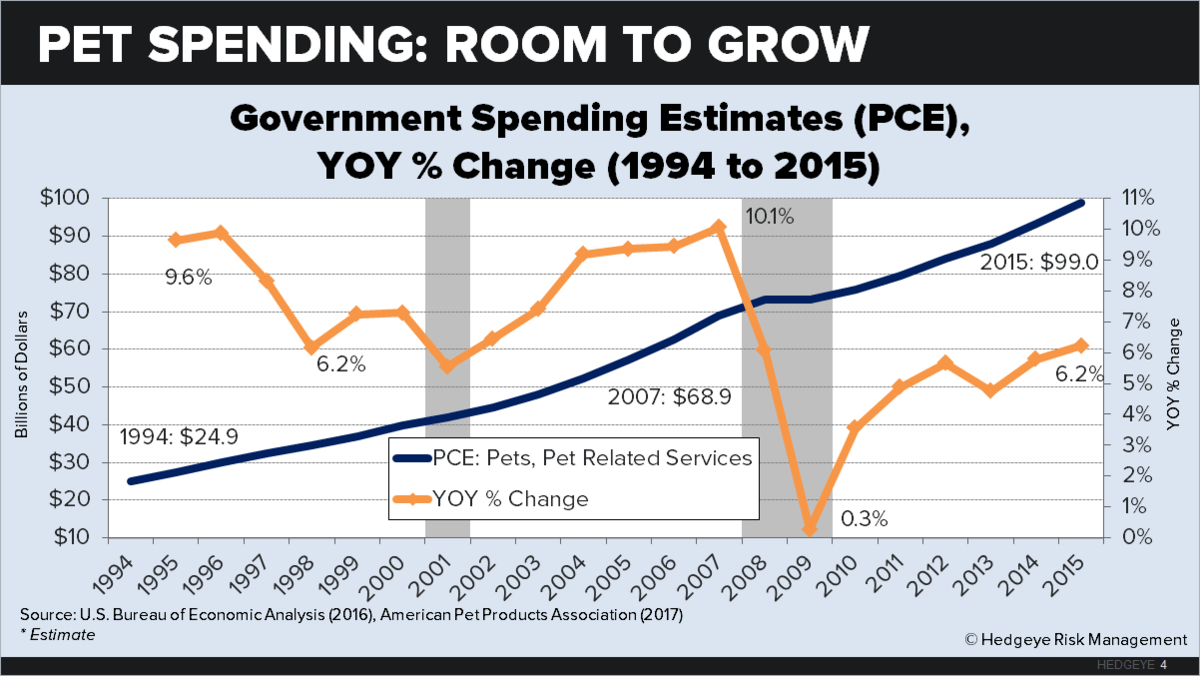

Considering the strong growth of the pet care industry, these ramp-up moves were practically no-brainers. Total spending on pets is soaring: U.S. PCE for pets, pet products, and related services hit $99 billion in 2015, up 26% from $73 billion in 2009. This growth may not match the pre-GFC decade, when pet care spending was surging at around 10% annually. But with a CAGR of 5.1%, pet care PCE is growing faster than total PCE and GDP since the Great Recession (both of which registered a CAGR of 3.8% from 2009 to 2015). Moreover, pet expenditures appear to be recession-proof, considering that YOY PCE growth has stayed positive throughout the past two downturns.

Very likely, 2016 will turn out to be another banner year for pet care, according to the industry. The American Pet Products Association estimates that pet expenditures hit $63 billion in 2016—up from $60 billion in 2015.

We’re seeing this spending increase play out across nearly every category of pet care. Sales from pet services (including things like grooming and boarding) have increased the fastest, registering a CAGR of 8.5% from 2011 to 2016. Spending on supplies and over-the-counter medicine is growing at 4.9%, while food and veterinary care are each growing by over 3% annually. The only category that’s not increasing, in fact, is the actual sale of animals.

What’s behind this growth? After a long period of relatively little change, we’re seeing a sharp rise in pet ownership. Between 1998 and 2009, the share of households that owned pets was stagnant, dropping slightly from 56% to 54%. But from 2009 to 2015, the rate shot up to 65%. While the rise in pet ownership boosts overall spending, owners are spending more per pet as well.

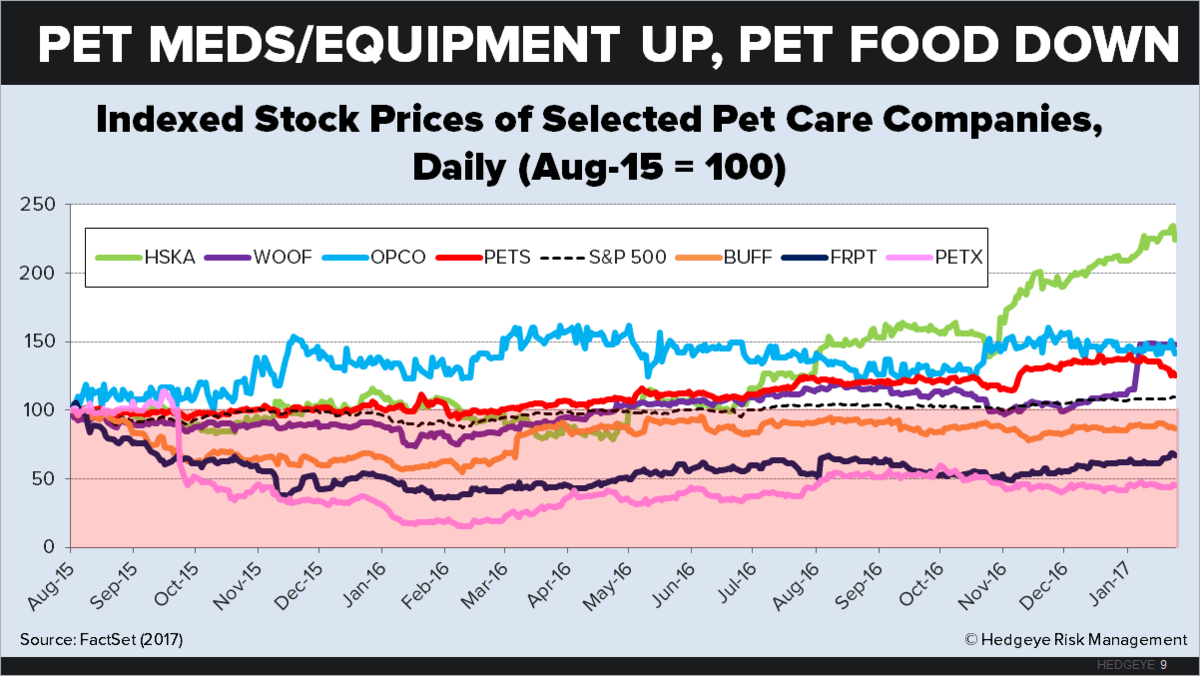

The rise in pet spending translates into healthy sales growth for companies primarily doing business in this industry. The five largest publicly traded companies that derive most of their sales from pet care include Freshpet (FRPT), Blue Buffalo (BUFF), Heska Corporation (HSKA), Veterinary Centers of America (WOOF), and OurPet’s Company (OPCO). Notice that even the lagging companies in this arena are experiencing sales growth of nearly 6% per year. The top company (FRPT) is growing at over 35% per year. Not only are their sales surging, but these companies are also ramping up their capital expenditures.

Even non-industry firms are increasing their exposure to the profitable pet care business. For multinational companies like Colgate-Palmolive (CL), Eli Lilly and Company (LLY), and SJM, pet care makes up a growing share of sales. Most notably, SJM reported that its pet brands accounted for 29% of the company’s sales in year-end April 2016—up sevenfold from 4% just one year earlier.

BREAKING DOWN THE PET CARE INDUSTRY SEGMENTS

What are the biggest revenue generators in the pet care industry?

Pet food. Pet food spending, the largest segment of the industry by dollar amount ($24 billion in sales last year), has been growing at 3.8% annually since 2011. According to Euromonitor data, this segment is expected to grow at a CAGR of 2.5% over the next five years. This growth rate is a bit slower than its recent CAGR, but certainly faster than other packaged foods—which are expected to grow at a CAGR of just 1.3% over the next five years.

What’s selling? Today’s pet owners splurge on high-quality, “premium” pet food. According to Mintel, 79% of U.S. pet owners say the quality of their pets’ food is as important as their own. This mentality is driving up sales of organic and grain-free “ancestral” blends—i.e., the Paleo diet for canines and felines.

Mars is the largest global player in this segment. With brands like Whiskas and Pedigree, the firm controlled roughly 25% of the global market in 2015. (The next closest competitor is Nestle, which is the leading pet food company in the United States.) Overall, the segment is heavily concentrated. Approximately 93% of mid-price dog and cat food revenue in North America goes to just three companies—SJM, Mars, and Nestle.

Health care: OTC medicine and supplies. Growth in health care spending has been robust in recent years—especially growth in OTC drugs, medical devices, and procedures, which have grown at a 4.9% clip since 2011. Note that this is faster than vet care delivered in clinics, which has grown at a slower 3.5% pace. It’s little wonder that stocks in this segment like HSKA have outperformed pet food stocks like FRPT.

The reality is that pet health care is becoming more like human health care. Advances in diagnostic testing for animals means that some pet owners are now shelling out as much as $400 to put Fido through an MRI machine. What’s more, these expensive tests often lead to more expensive treatments. Today, veterinarians can treat dogs for depression and prescribe underwater therapy for cats suffering from arthritis.

And like human health care, there is a growing emphasis on preventative care and wellness for pets: Banfield Pet Hospital (located in many PetSmart stores) now offers an “Optimum Wellness Plan,” which includes unlimited vet visits, routine vaccinations, and early screening for serious illnesses.

Thanks to Mars’ acquisition of VCA, it leads the pet health care segment as well. The company already owns Banfield and BluePearl Veterinary Partners.

Health care: pet insurance. The rapid expansion of pet health care is fueling the small but growing field of pet insurance. Although less than 1% of pets in the United States and Canada were covered by a plan in 2014, pet insurance premiums surged by 17% YOY in 2015.

Who provides pet health insurance? Top providers include the ASPCA, PetFirst, Petplan, and Trupanion (TRUP). Traditional insurance providers like Geico and Progressive also offer pet policies.

DRIVERS

The pet care boom is being driven by three mutually reinforcing trends. The first is the insistence that food and health care for pets be on par with food and health care for humans--meaning that owners today demand for their pets the same appearance and wellness benefits that they demand for themselves. The second is the rapidly rising quality bar for everything humans do demand for themselves. The third is the rising number of pets per human. All of these trends acting together are triply catapulting pet spending upwards.

Pet brands like Young Again Pet Food promise anti-aging benefits and others like Natural Balance offer vegetarian options that guarantee healthy skin and shiny coats. Do pets care about how they look or whether they consume all-natural ingredients? No. But their human owners do—and they’re buying.

Nobody is more willing to splurge on their pets than Boomers. In many ways, the success of the pet care industry is a generational story that started with Boomers, who grew up in the homes of older generations who regarded pets as, well, just animals. Young Boomers began the trend of “humanizing” pets—making them “part of the family.” They later changed the narrative from pet “ownership” to pet “companionship” and redefined civil rights to include animal rights. (PETA’s radical founders and leaders are all Boomers, now in their late 50s to early 70s.)

Today, Boomers have no qualms about spoiling their pets. In fact, 55- to 64-year-olds account for the largest share of total pet spending. And now that Boomers are aging in place and spending more time at home (often alone), their need for companionship will undoubtedly grow.

This humanization of pets has been passed down to Xers, who are second in spending to Boomers. For this generation, pets are the perfect way to enhance family togetherness—a top priority for Xers. And for parents concerned about the health and well-being of their kids, the “dirtiness” often associated with pets is now a plus—animal germ exposure being the perfect preventative against asthma and allergies.

WHAT’S IN STORE FOR PET CARE?

The future of the U.S. pet care industry will only get brighter in the coming years. One reason is population aging: A look around the globe reveals that pets are more commonplace in aging, high-income societies with low birthrates. Take Japan, for example, where pets have outnumbered children under age 16 since 2003. And Japanese cat ownership is rising—particularly among working couples and elderly households. As the U.S. population becomes top-heavy with senior Boomers, America could follow a similar path.

Quite simply, pets are the perfect antidote to loneliness—and long-term care communities in the United States are starting to take notice. Communities like The Green House Project and The Eden Alternative promise residents a “meaningful” environment—and pets and plants help furnish the meaning.

Moreover, as Millennials continue to age, they will likely adopt pet ownership habits of their own. It’s true that Millennials currently spend the least amount of any generation on pets. For today’s urban-dwelling and cash-strapped Millennials, pet ownership just isn’t feasible and (like parenthood) will be delayed. Plus, many are still living at home, where their parents’ pet is their pet as well.

But as I’ve mentioned elsewhere, as Millennials become parents, they’re spending big bucks on organic baby food and high-tech wearables for their children. It’s hardly a stretch that Millennials will project the same health and safety considerations onto their pets.

THE BOTTOM LINE

So who’s a good play in this industry? Most companies specializing in pet care (like the five mentioned earlier) are doing well. One strategy would be to cap-weight invest in all of these firms and thereby take advantage of the positive tailwinds across all segments of the pet care business.

Another strategy would be to focus on larger companies that are rapidly moving into the pet food arena. SJM is one. Through its acquisition of Big Heart Pet Brands, it has a strong foothold in the North American pet food market. The company is also doubling down on its premium brands. According to a recent earnings call, the company recently launched its Nature’s Recipe premium pet food brand in mainstream grocery stores. In addition, SJM is redesigning its protein-based snack brand, Milo’s Kitchen—which is sure to appeal to diet-conscious pet owners.

There is also ADM, though pets may not comprise a large share of its revenue. In addition to its recent M&A activity, ADM announced plans to build two state-of-the-art plants for its animal nutrition business. And LLY recently made headway in the pet health care field when it acquired Boehringer Ingelheim’s portfolio of Vetmedica pet vaccines.

Finally, if you want to take a flyer on a small company with high upside, TRUP could be worth a look. This is a small company which has yet to generate positive earnings, but which could be a big winner if the nascent pet insurance segment takes off.