“Simplicity is the ultimate sophistication.”

-Leonardo da Vinci

Dollar Down, Rates Down, Oil & Stocks Up. How simple is that? That’s what happened in US markets last week. Oil was up another +4.1% on the week taking its reflation ramp to +26.7% YTD.

Essentially, if you want the difference between Quad 4 and Quad 3, that’s it. Rather than a Dollar that goes straight up, deflating asset prices while growth is slowing, USD is sideways to down (making lower-highs), reflating asset prices with a Dovish Fed.

This Quad 3 stuff doesn’t happen without growth, inflation, and profit data #slowing… and the Fed going dovish in kind. The Question this week is will the Fed be Dovish Enough? Or will the Fed sound hawkish relative to Powell’s last 2 dovish pivots?

Back to the Global Macro Grind…

Welcome to Macro Monday @Hedgeye. To long-time subscribers to our risk management #process, welcome back. For those of you who are new to what we do, today is the day we review last week’s macro market moves within the context of @Hedgeye TRENDs.

As a reminder, @Hedgeye TRENDs are intermediate-term signals that are generated quantitatively with no fundamental research opinion. I use them to help me risk manage the timing and sizing of fundamental longs and shorts.

Signals don’t always agree with research views. When they do, it’s easier to have higher conviction (larger) positions. Here’s what currencies did last week within the lens of their respective @Hedgeye TREND signals:

- US Dollar Index corrected -0.8% last week to +0.4% YTD and remains Bullish TREND @Hedgeye

- EUR/USD was +0.8% last week to -1.2% YTD and remains Bearish TREND @Hedgeye

- Yen was -0.3% vs. USD last week to -1.7% YTD and remains Bearish TREND @Hedgeye

- Pound was +2.1% vs. USD last week to +4.2% YTD and remains Bullish TREND @Hedgeye

- Canadian Dollar was +0.4% vs. USD last week to +2.2% YTD and remains Bearish TREND @Hedgeye

So that was the Dollar Down part – and the Rates Down part looked like this:

- UST 2yr Yield down another -2 basis points to 2.44% remains Bearish TREND @Hedgeye

- UST 10yr Yield down another -4 basis points to 2.59% remains Bearish TREND @Hedgeye

- High Yield OAS Spread down another -18 basis points to 3.86% is back to Bearish TREND @Hedgeye

For whoever was looking for the UST 10yr Yield to “break-out above 4%” six months ago, they’ve been timestamped by US #GrowthSlowing with the UST 10yr Yield down for 14 of the last 19 weeks!

That’s obviously why Yield sensitive asset allocations like:

- Utilities (XLU) are up +7.2% in the last 6 months

- REITS (VNQ) are up +3.2% in the last 6 months

- Gold is up +7.4% in the last 6 months

Whereas those asset allocations that got crushed by Quad 4 for three to four of those 6 months like the Russell 2000 (IWM) and Energy Stocks (XLE) are still down -10% and -12%, respectively, in the last 6 months.

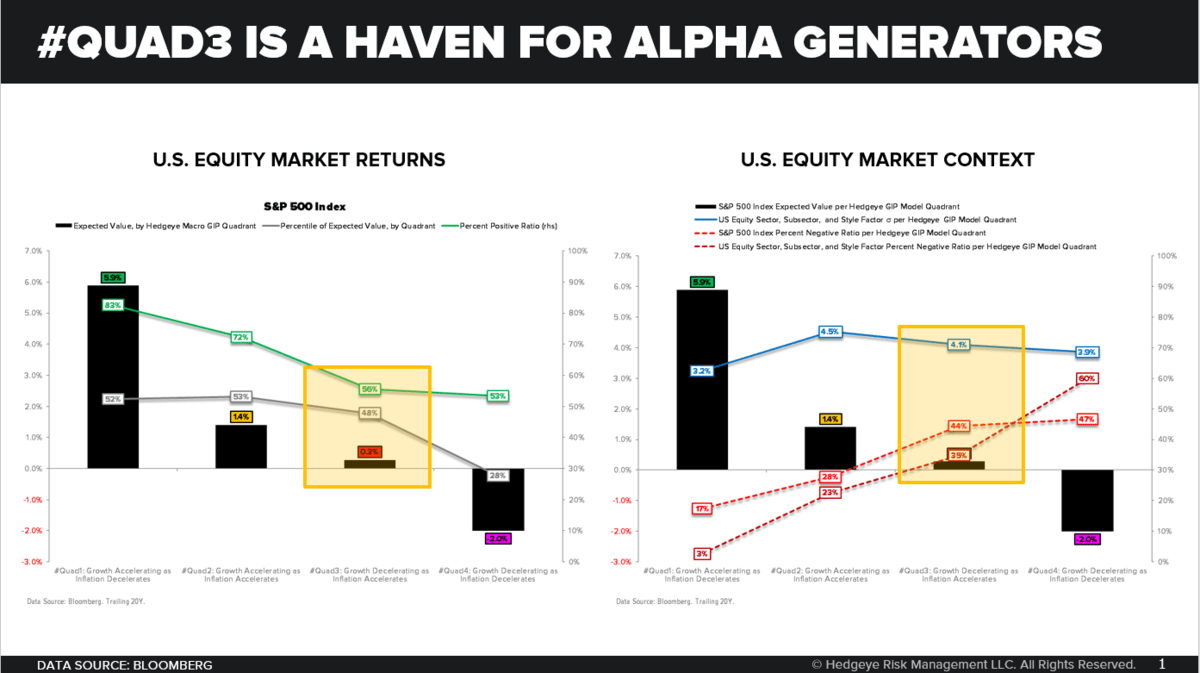

Our GIP (GROWTH, INFLATION, POLICY) Model likes Long Oil and Energy Stocks during Quad 3. With our GDP now-cast ticking at +1.22% headline US GDP for Q1 of 2019, we have the US economy heading into Quad 3 for the next 3 quarters.

As we outlined in our Q1 Macro Themes deck 2.5 months ago, some of the best shorts in Quad 4 are NOT shorts in Quad 3. Sector exposures with organic growth (like Tech and Biotech) aren’t Top 3 Sector Style longs, but they are longs.

Here’s what US Equity Sector Styles did last week:

- Tech (XLK) led the rally at +4.6% on the week to +17.8% YTD and remains Bullish TREND @Hedgeye

- Energy (XLE) was +2.5% on the week to +14.2% YTD and remains Bullish TREND @Hedgeye

- Industrials (XLI) lagged at -0.4% on the week to +14.9% YTD and remain Bullish TREND @Hedgeye

While the Russell (IWM) and the Financials (XLF) are still Neutral and Bearish @Hedgeye TRENDs (from a quantitative signaling perspective), respectively, the NASDAQ flipped to Bullish TREND @Hedgeye almost 4 weeks ago.

Interestingly, but not surprisingly, with the VIX crashing -20% last week, the SP500 signal is barely back to Bullish TREND @Hedgeye for now as well. That’s why I didn’t re-short it last week (after covering the short on red when it signaled #oversold in the week prior).

Risk management signals are risk management signals for a reason. They don’t have to rhyme with our research view. While it’s a great short in Quad 4, SPY was never a short in Quad 3 anyway. Financials, Consumer Staples, and Materials are.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signals in brackets) are now:

UST 10yr Yield 2.55-2.67% (bearish)

UST 2yr Yield 2.39-2.51% (bearish)

SPX 2 (bullish)

RUT 1 (bearish)

NASDAQ 7 (bullish)

Utilities (XLU) 56.40-58.77 (bullish)

REITS (VNQ) 83.05-86.84 (bullish)

Energy (XLE) 63.33-66.90 (bullish)

VIX 12.10-17.50 (bearish)

USD 95.70-97.70 (bullish)

EUR/USD 1.11-1.14 (bearish)

USD/YEN 110.86-112.11 (bullish)

GBP/USD 1.30-1.33 (bullish)

Oil (WTI) 55.29-59.17 (bullish)

Gold 1 (bullish)

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer