THE HEDGEYE EDGE

Below is a note written by Retail analyst Brian McGough:

When all is said and done, I think that 2019 will go down as the year where Brick & Mortar pushes back against pure-play online – most notably Amazon – which will ultimately be to the detriment of margins across the board.

This is not an overnight phenomenon – as it’s been building for the past two years, but it’s been simply masked by two factors:

- A multi-year acceleration in US Retail sales, and

- An 18-month period where incremental dollars broke a long-term trend and accrued particularly to high-margin B&M as opposed to online.

In other words, there’s been more than enough growth to go around – and more of that occurred at the (highly profitable) store-level than the consensus thinks, and more than most management teams will admit.

If you talk to the CEOs of Walmart and Target, they’ll tell you that leveraging the store as de-facto DC infrastructure while layering on home delivery tops the list of strategic initiatives by a country mile – and we’re seeing the capital deployment to back that up. Their mindset isn’t about hitting numbers in a given year – but is about long-term survival in #Retail5.0 and should ultimately lead to tempered margins for particular pockets of retail.

That means shorting Amazon. I know, I know. Amazon is going to take over the world. I get the defendability of AWS, as well as Advertising dollars as an incremental profit driver. But growth is slowing as the business model faces a different stage of its maturation curve, and we even saw the likes of TGT challenge it in 4Q with free shipping deals that incrementally pressured AMZN’s GM. In fairness, Gross Margins still went up, and will likely go up again in 2019.

But as recently as 2-years ago WalMart and Target could do virtually nothing to derail AMZN’s momentum or even put a ding in its P&L. It’s finally falling subject to at least some competitive forces such that we have to at least consider that this thing called valuation exists, especially in the context of slowing fundamentals.

When it comes to 2019/20 modeling, we’re incrementally bearish on revenue, bearish on Gross Margins, and bullish on SG&A – not the trifecta you want to see to justify pushing new peaky earnings/cash flow multiples. In 2019 we’re modeling total GMV ticking down to the high teens.

Yes, that’s still AWESOME – but even (especially) ‘awesome’ needs to respect RoC. SG&A leverage is likely to push this name to a 6-7% margin next year – something it NEEDS to print in order to justify current valuation. Slowing revenue with a weakening US consumer will put real pressure on the AMZN multiple.

The punchline here is that I’m completely on board with AMZN as the TAIL winner in retail – no argument there – same way I wouldn’t have argued with WMT as being the winner 20-years ago. But I firmly believe that it’s at a point where we need to pay close attention to the rate of change of revenue, and the earnings and cash flow drivers that apply to the other 99% of companies out there.

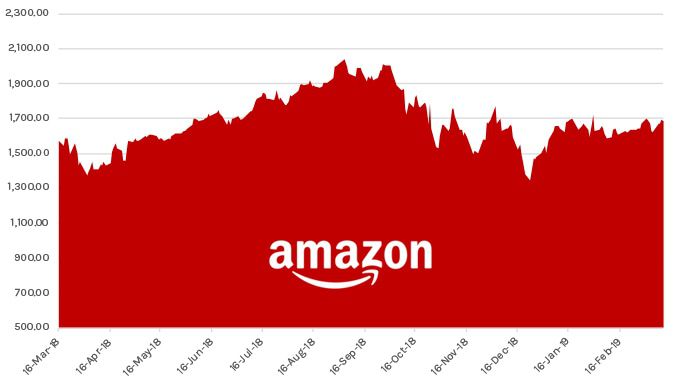

ONE-YEAR TRAILING CHART