Editor’s Note: Below is a stock report written by the Hedgeye Housing team – led by Josh Steiner and Christian Drake. The stock report lays out a broader bullish on Housing (ITB) thesis rather than a specific fundamental research call on Toll Brothers – though it’s being expressed through Toll Brothers because it does screen positively via Hedgeye CEO Keith McCullough’s quantitative Risk Ranges. The stock report below lays out the broad bullish on Housing thesis.

THE HEDGEYE EDGE

The fundamental call on Housing here isn’t for some escape velocity, step function style inflection in transaction activity – it’s for a progressive transition to ‘less bad’ as the decline in interest rates, a still strong domestic labor market and progressively easier 2019 comps work to shepherd a path to rate-of-change stabilization for a sector mired in a negative 2nd derivative volume slump for years at this point.

In short, it’s a quintessential case study in better/worse defining the investment-scape where the simple absence of further, rampant deterioration is the marginal change of consequence.

The high-frequency domestic housing data remains congruous in its YTD traversal towards less bad. Indeed – with Mortgage Purchase Application data in Jan/Feb improving, February Builder Confidence rebounding, Pending Home Sales bouncing (which should drive a bounce in EHS as well) and now January Starts data more than reversing last month’s harrowing decline – the most real-time housing data are reflecting harmonized improvement.

As we’ve detailed recurrently, the larger narrative arc here is relatively straightforward:

The twin rate shocks in 2018 served to amplify affordability concerns and drove a wedge between the bid-ask on prospective transactions, which served to further suppress already soft volume growth. Seller behavior, predictably, responded on a lag in the form of increased listing price cuts which manifest on further lag in decelerating HPI. These dynamics characterized most of 2018 and 4Q in particular as the reported fundamental data remained a lagged reflection of the prior move higher in rates.

We’re now seeing the first stabilizations/inflections in the reported data against easier comps and on a short lag to the sizeable retreat in rates to close the year.

The Data:

- Total Starts: Total Starts, driven primarily by SF strength, rose +18.6% sequentially while year-over-year growth held negative at -7.8%.

- SF Starts: SF starts rebounded off the 29-month low recorded in December, rising +25.1% M/M and accelerating to +4.5% Y/Y. Permit activity, which has been relatively stable, was less auspicious, falling -2.1% M/M and -6.7% Y/Y.

- MF Starts: Multi-family activity, while volatile on a month-to-month basis, continues to traverse the back-side of its activity curve for the present cycle = +2.4% M/M and -32% Y/Y.

We expect similar stability to characterize the near-term data with housing remaining a beneficiary of lower rates catalyzed by growth slowing conditions globally and locally. Absent an accelerating cyclical slowdown domestically, the rate of change upside in the data is likeliest to emerge alongside increasingly easier comps dynamics as we move through mid-year.

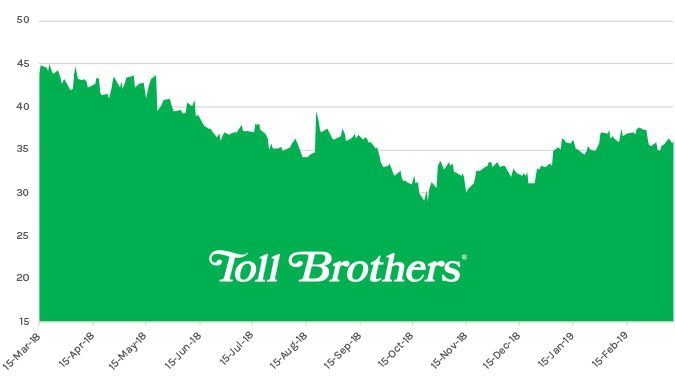

ONE-YEAR TRAILING CHART