The Macau Metro Monitor, April 13th, 2010

CONSUMER CONFIDENCE IN MAINLAND, HONG KONG AND MACAU DROPS FOR TWO QUARTERS CityU NewsCentre

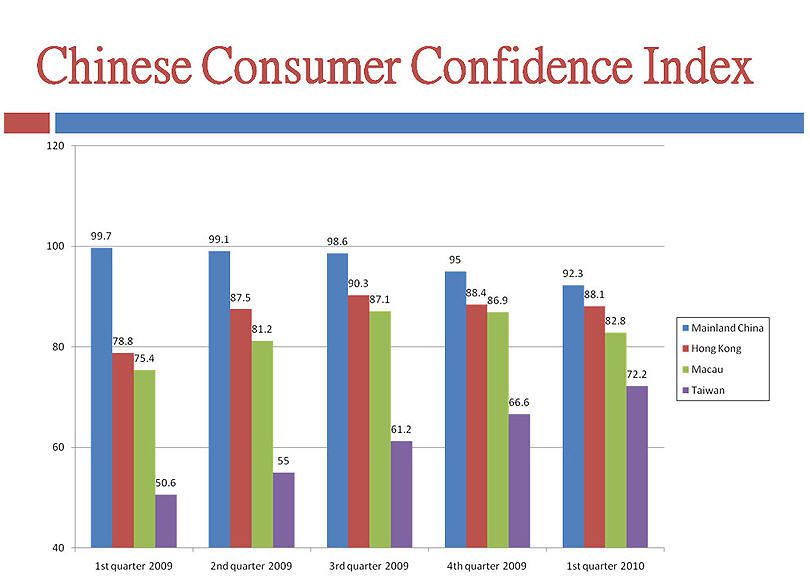

According to a survey carried out by universities in the region, consumer confidence in mainland China, Hong Kong and Macau fell QoQ to 92.3, 88.1 and 82.8, respectively. Macau's decline of 4.7% was the most of the group. The index uses a scale of 0 (representing no confidence) to 200 (complete confidence) to represent ascending levels of consumer confidence. Scores below 100 suggest people are lacking adequate confidence while scores above 100 reflect good confidence.

The drop in the overall consumer confidence in mainland China, Hong Kong and Macau was mainly due to the record low sentiment about prospects in the housing market. In this category, Macau recorded the steepest decline of 15.3%, to 37.6, while sentiment in Hong Kong and mainland China was down 12.4% (to 58.1) and 7.8% (to 62.9), respectively.

SPEYMILL MACAU AGREES HK$796MM RIVIERA SALES IBTimes, macaubusiness.com

Macau focused real estate investment company, Speymill Macau Property, has reached sale agreements for almost all the 259 apartment units the company owns in The Riviera, a two tower residential development on the Inner Harbour area, formerly known as Lorcha. The company owns a total amount of 270,951 square feet in the development, of which 231,291 sq ft were under contract as of 4/12/2010, leaving a total of 39,660 sq ft remaining to be sold. The company owns 145 units of 296 units in Tower 1 and 114 units of 222 units in Tower 2 of Riviera. The average price of the units sold in Tower 1 was HK$3,568 per square foot.The average price of the units sold in Tower 2 was HK$3,581 per square foot. The estimated total net revenue from such sales will amount to approximately HK$796MM, according to Speymill.

HAVE CASINO IN LABUAN AsiaOneNews

The Labuan Chamber of Commerce (LCC) would like a casino to boost its tourism industry. LCC chairman Datuk Francis Tee Chee Hok told the Daily Express, "A casino could be the answer and it is also compatible with Labuan's status as a free port". Aware of the government's stand of not favoring the issuance of new casino permits, Tee said the proposed Labuan casino could be an extension of the Genting Highlands casino.He suggested that the casino could be in the form of a floating ship, departing from the island at 6pm and returning at 6am with strict checks to prevent the wrong people from patronizing it.