|

MARKET WATCH: What’s Happening? Much has happened since we made our bearish call on Google and Facebook nearly a year ago. If you had incorporated these two companies into a long-short against the market last February, you would have made a hefty profit. But is the short still on? Many analysts, believing the market correction to be over, are now advocating buying these stocks—with one of them (Facebook) seemingly at a bargain-basement price. Our Take: This may be a mistake. Google and Facebook face several short-, medium-, and longer-term headwinds that the market has not fully accounted for. In the short-term, the Q4 2018 earnings season may be rough, featuring a year-over-year revenue growth slowdown for both firms. In the medium-term, Facebook is expected to experience severe margin compression stemming from market saturation. Longer-term, Google and Facebook will be met with an unforgiving U.S. advertising market, a lasting consumer tech-lash, and looming regulatory threats at home and abroad. Of the two firms, Facebook faces bigger medium-term revenue challenges—but Google clearly has the most valuation “air” to lose. |

Last February, the Hedgeye Demography Sector issued the first of two bearish calls on Google and Facebook. With the one-year anniversary of that call approaching, it’s a good time to reflect on what’s transpired since then—and how the outlook has changed for these two tech giants.

Below, you’ll find our updated thesis. For an in-depth recap of our original thesis, please revisit our February call (see: "The Next Big Thing: Danger Ahead for Google and Facebook?").

MARKET ROUT PUMMELS FACEBOOK

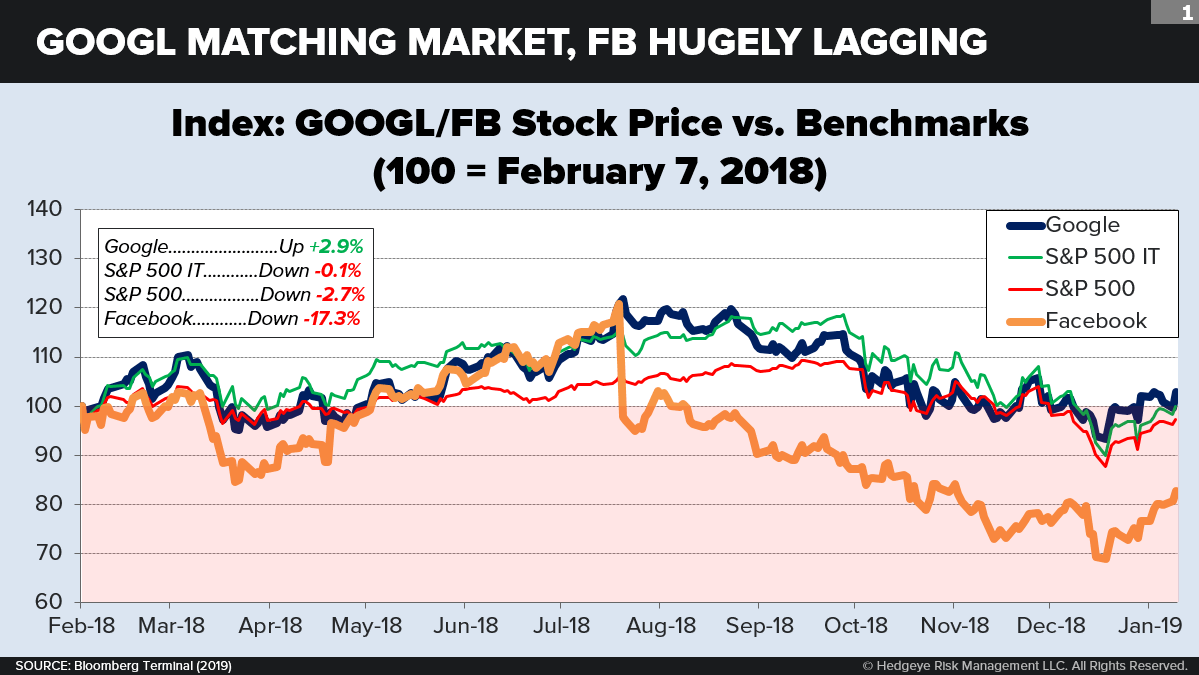

Google and Facebook have behaved very differently in the market over the past several months. Since February 7, the date of our original call, Facebook shares have plummeted –17.3%, much larger than the decline registered by the broader market (S&P 500 Total: down –2.7%; S&P 500 Infotech: down –0.1%). Google stock is up +2.9% over the same period.

Even given Google’s outperformance, our short call looks good in hindsight. If you had shorted both of these firms equally on the date of our call, you would have made a profit: A $10,000 bet placed on February 7 would have generated a +7.2% return. Even a long-short against the entire market (long S&P 500, short Google-Facebook) would have generated a +4.5% return.

To be sure, skeptics may be wondering to what extent this decline in Facebook’s share price reflects weakening earnings expectations for all of Big Tech. After all, 2018 was the year in which Big Tech finally faced a real market reckoning, which compelled analysts to rethink their buoyant earnings projections. How much did this rethinking change the prices of these two stocks in particular?

The answer: Not much. Since February, analysts have downgraded their 2020 Facebook EPS expectations by –21.0%. (For the record, EPS expectations for Google have fallen –3.4% over that time.) But analysts have not downgraded their 2020 earnings expectations for the broader tech universe by nearly as much: –2.2% for the S&P 500 Infotech sector, and –5.5% for the tech-heavy Nasdaq Composite. In essence, this tells us that only a small fraction of Facebook’s price decline since February can be explained by Big Tech’s overall troubles.

So we need to ask: Why has the joint outlook for Google-Facebook fallen behind the market at large? And why have investors treated Google and Facebook so differently, given their many similarities? We’ll answer these questions in three time frames (short-, medium-, and longer-term), and finally reflect on the prospects for each company and their industry.

CHANGE IN SHORT-TERM OUTLOOK

Facebook’s Q4 earnings report is due to be released on January 30. Google’s Q4 report is due out on February 4. That’s just days away. Both firms could use—correction, desperately need—a strong quarter.

Why? Because the last three quarters have witnessed an accumulation of disappointing news. Google shares dipped –4% following its Q3 2018 revenue miss, which executives attributed to rising traffic acquisition costs. Facebook, meanwhile, was responsible for the greatest one-day value destruction in the history of the U.S. stock market after its Q2 2018 earnings report showed the company’s slowest-ever growth in monthly usership. These concerns did not abate in Q3, when Facebook suffered a revenue miss thanks to flat North American user growth.

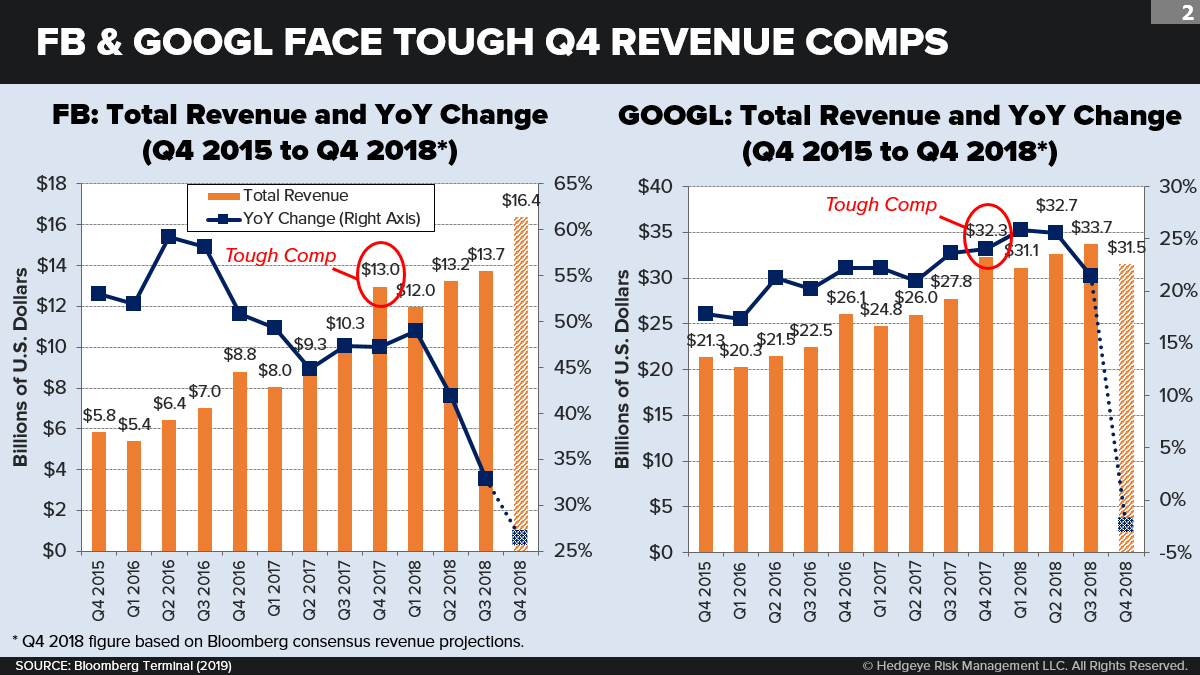

All indications are that this tough sledding will continue in Q4 2018. Only now the bad news will be compounded by the very challenging comps set for both firms by Q4 2017.

Let’s start with Facebook. Though the company’s revenue is projected to rise QoQ to $16.4 billion in Q4 2018, this figure would represent a declining YoY revenue growth rate thanks to a tough Q4 2017 comp. Moreover, $16.4 billion would mark the third consecutive quarter of slowing YoY revenue growth for Facebook—and by far the lowest growth rate in years.

The dead-ahead danger is even bigger for Google. Mean consensus estimates put Google’s total revenue at $31.5 billion in Q4. That figure would represent a decline both on a QoQ and on a YoY basis. Although Google’s click rates have been rising, its total revenue per click has been falling—down –28% in Q3 2018, the largest decline in at least three years. Playing into this decline is Google’s continued shift toward mobile and YouTube ads, which command less of a premium than desktop ads. (This is because desktop ads are more likely to generate an actual purchase than mobile and video ads.)

For Google, a consensus revenue print translates into a precipitous decline in YoY growth—from +21.5% to –2.4%. Sure, all the Old Wall analysts with a buy on Google “know” this. Right? But just wait until big investors wake up to discover that, of all equities in their portfolio with non-trivial operating margins, their biggest and most expensive mega-cap (Google, with P/E = 40 and OM = 26%) is actually shrinking in YoY revenue.

There’s no secret sauce here; our analysis hinges on publicly available figures. Anyone could have seen this tough comp coming. But the reality has been largely ignored by the mainstream financial media narrative. Instead, most outlets are talking about how these companies have bottomed, or should be bought because they’re cheap relative to their peers. Well, they may be cheap—even Google is a lot cheaper today than it was in July—but don’t be surprised if they’re even cheaper next month, after hitting “lower lows” following the Q4 earnings releases.

CHANGE IN MEDIUM-TERM OUTLOOK

When we look past the Q4 print to CY 2019, our biggest concerns shift from Google to Facebook. Many investors obviously share these concerns, which is why Facebook’s price has recently been taking a beating.

One looming threat is margin compression. In 2018, Facebook attained operating margins of 44.2%, which the consensus expects to decline to 36.6% in 2019. In hindsight, it appears that Facebook’s margins peaked in 2017, at an unsustainable 49.7%. By 2021, looking forward, analysts expect Facebook’s margins to recede to 36.0%—not much higher than Google’s expected margins (28.7%). Google, by contrast, is expected to grow its margins slightly from 2018 to 2021—an impressive feat for a company of Google’s size and maturity.

So Facebook’s revenue growth is decelerating, and it is profiting less from every dollar it does earn. Why? It comes down to effective market saturation: Facebook usership has stagnated in its most profitable region. Facebook’s Q3 earnings report shows that the company has 242 million monthly active users in the U.S. & Canada, virtually unchanged YoY. This is bad news, considering that Facebook earns three times more revenue per user in the U.S. & Canada ($27.61) compared to Europe ($8.81), 10 times more compared to Asia-Pacific ($2.67), and 15 times more compared to Rest of World ($1.82).

For all its talk about expanding to underserved markets, Facebook remains beholden to its North American business—and in the absence of growing usership, it will be forced to rely on boosting its average revenue per user (ARPU). But Facebook’s brand premium already appears to be wearing off: Even in the U.S. & Canada, Facebook’s ARPU growth rate YoY has ratcheted down for two quarters running. In fact, with only two exceptions, the ARPU growth rate YoY has declined in every quarter since Q2 2016.

CHANGE IN LONGER-TERM OUTLOOK: OUR “THREE DYNAMICS”

There’s a sense among investors that even if Google and Facebook do suffer a decline, they’re destined to make it up. After all, they’re part of the vaunted FAANGs, a group of transformational companies that have long led the market and dominated the public awareness.

But this confidence may be misplaced. Google and Facebook’s challenges extend far beyond 2019. As we pointed out in our original call, these companies face long-term headwinds—many of which have worsened in the past few months. Let’s examine.

Our “three dynamics” have shifted—but troubles remain. Recall that in our original call, we laid out three growth “dynamics” that would enable Google and Facebook to meet their revenue projections—Google and Facebook squeezing out all of their digital competitors; digital ad spending rising rapidly as a share of total ad spending; and total ad spending rising rapidly as a share of GDP. (Again, for a full recap, see our February call.)

Overall, these dynamics have quantitatively improved a bit—but they’ve also shifted in an awkward direction. We remain dubious.

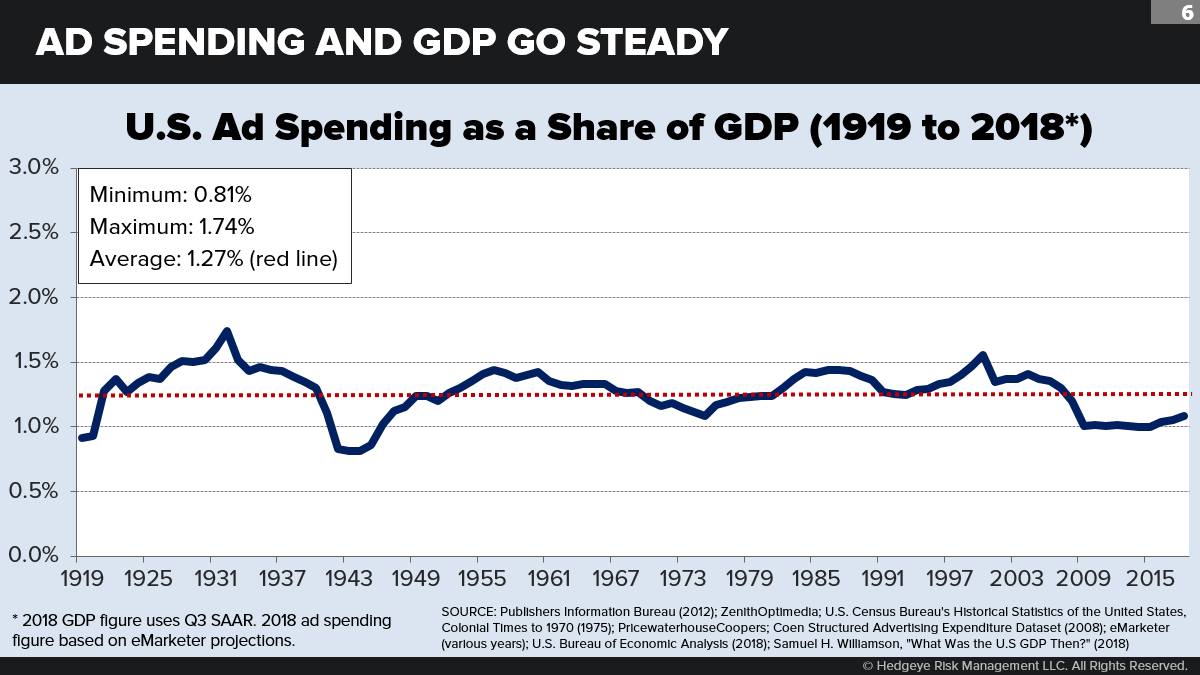

Dynamic #3: Ad Spending Rising as a Share of GDP. This was a wash. We pointed out that this relationship has been stable for the past century and is unlikely to change much—and our reasoning held true in 2018, when U.S. ad spending accounted for 1.08% of GDP (according to preliminary figures), up only +0.04 percentage points from the year prior.

Keep in mind that 2018 was a year that had everything going for it in terms of ad spending. It happened near the peak of the business cycle (ad spending is pro-cyclical), and as expected it featured large ad spending boosts due to the 2018 midterms and the Winter Olympics. Adjusted just for these two items, ad spending remained flat as a share of GDP. In fact, ad industry forecaster MAGNA Global expects U.S. ad revenue to grow slower than GDP in 2019 precisely due to the absence of such events.

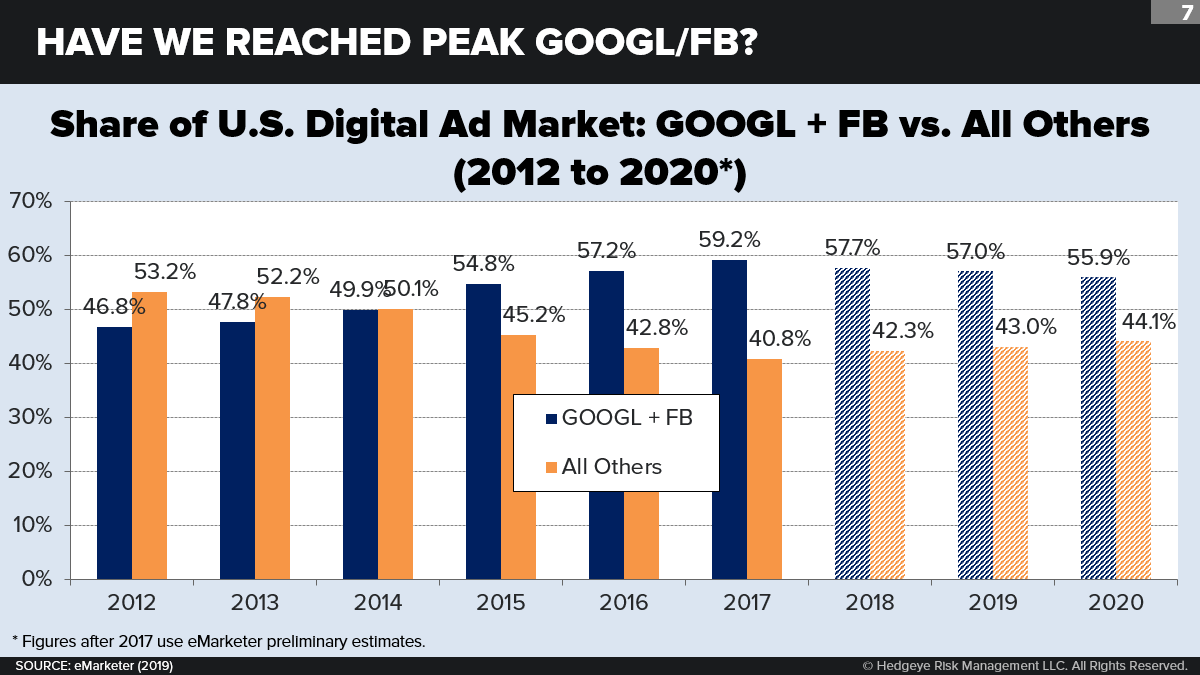

Dynamic #1: Google-Facebook Growing as a Share of All Digital Ad Revenue. The outlook here looks much worse than it did in February. In 2018, according to eMarketer, the two companies owned a combined 57.7% of the market—down significantly from 2017. The big laggard here has been Google, whose share slid by more than 2 percentage points from 2017 to 2018. Google, quite simply, has become a victim of its own success; it’s much harder for an industry incumbent to keep growing its market share indefinitely than it is for a relative newcomer to win market share. Facebook, on the other hand, has been growing its market share each year—but not enough to make up for Google’s slowdown.

A brief aside is warranted here, because this loss in combined market share was something most analysts considered unthinkable a year ago. (OK, Google perma-bear James Dix may have seen it coming, too.) But not only did we foresee this possibility, we also correctly identified the biggest single force that would thwart these firms’ drive to take over digital ad spend. That force is Amazon.

Allow us to quote from our February report: “One competitor hardly anyone suspects may yet pose a serious threat to Google and Facebook: Amazon.” And this: “Amazon points to a bigger challenge for Google in particular.”

Now let’s turn to eMarketer’s latest figures, which show that Amazon took 4.1% of the market in 2018, well above the 2.7% that eMarketer forecasted back in April. By 2020, eMarketer now expects Amazon’s market share to hit 7.0%. Meanwhile, Piper Jaffray expects Amazon’s ad business to triple over the next few years, growing larger than its cloud-computing business in the process. This improved outlook for Amazon makes it even less likely that Google and Facebook will be able to meet the consensus revenue projections thanks to increased market share.

Dynamic #2: Digital Ads Growing as a Share of All Ad Revenue. Luckily for Google and Facebook, a worsening outlook for Dynamic #1 was made up for by an improving outlook for Dynamic #2: digital ad spending rising as a share of total ad spending. Digital ads had a whopping year in 2018, gaining 6-plus percentage points of market share within the total U.S. ad universe (49.7% today by eMarketer’s count, up from 43.1% in 2017). If one assumes an unchanged growth rate in digital market share since 2012 (as we did for all three dynamics in our February call), Google-Facebook’s revenue targets are actually a bit more plausible today than they were a year ago.

Does that make us more bullish? Not really, because in our opinion this growth rate in digital share cannot possibly be repeated for several years in a row. And, without any help from Dynamic #1, Google and Facebook would have to rely entirely upon such repetition to meet their revenue goals. This would mean, as we have pointed out, that digital advertising would gobble up nearly three-quarters of all advertising by 2021. It would imply massive yearly dollar declines (roughly –2.5% per year for three years) across the entire TV, print, and radio advertising universe. Sure, times are tough for old media. But no one is projecting that sort of Armageddon.

What’s more likely is that the very fast pace of digital growth in the last few years reflects the meteoric contemporaneous increase in the daily digital hours spent by the average adult age 18 and over. That increase in turn reflects the advent of mobile digital platforms. But, as we pointed out in February, all of these growth rates have to decelerate sharply for one simple reason: There are only so many hours in the day.

Indeed, using more recently published Nielsen numbers, we can see that this abrupt slowdown is already happening. From Q2 2015 to Q2 2017, average digital hours per day soared, from 2.2 to 3.9 (+77%). One year later, in Q2 2018, the number is 3.6 (–8%). In other words, the growth is not only halting. It is backtracking. We will return to this point below: “Tech-lash” may point to a very different future than what Google and Facebook are expecting.

That’s not all. The old media firms are not just marching meekly off a cliff. Rather, they are overhauling the way they do business. Consider traditional TV, for instance, which is changing materially in three ways—all of which are bad for Google and Facebook.

One: The big telecoms are adopting “addressable advertising,” which boosts their ad pricing to levels closer to digital pricing. With its subscriber data, AT&T expects to triple its revenue per ad on its new Turner TV ad inventory. Two: TV is shifting toward digital in the form of over-the-top (OTT) offerings. This introduces new competition into the digital ad market; namely, OTT firms like Roku and Hulu. Three: TV is moving toward a subscription model. This opens up the possibility that a network could roll out ads on its captive audience—again, putting pressure on Google-Facebook’s market share. We saw this happen with Amazon, whose ad storm took everyone by surprise. Could Netflix be next?

CHANGE IN LONGER-TERM OUTLOOK: OTHER HEADWINDS

OK, let’s recap our update on the three dynamics. Quantitatively, bad news in one (Google-Facebook as a share of digital) is entirely offset by good news in another (digital as a share of total ads). But we are even less comfortable than before with the result, because we are very skeptical that the historical growth trend since 2012 in the good-news dynamic can possibly continue for three more years. And, at this point, everything hinges on that trend continuing.

Now let’s turn to the final section of our February report where we discussed other long-term headwinds facing these two firms. Three of those headwinds are worth revisiting here (tech-lash; political threats at home; and political threats abroad), since there have been significant new developments in each.

The consumer tech-lash has worsened. Tech-lash dominated the news cycle in 2018. Excessive screen time has been implicated in everything from the erosion of impulse control to rising rates of loneliness and depression (see: "The Next Big Thing: All the Lonely People"). New NIH research even shows that screen time may be altering the structure of developing brains (see: "Trendspotting: 12/17/18").

Startups are offering special apps and devices that promise to offer consumers a digital detox (see: "Trendspotting: 2/20/18"). Parents—most notably, Silicon Valley parents who know best and set the standard for the rest of us—are imposing radical screen-time limits or bans in their own homes (see: "Trendspotting: 11/5/18"). Luxury getaways are promising freedom from the Internet. States are rethinking the wisdom of allowing screens in the classroom (see: "Trendspotting: 4/30/18").

Not long ago, being glued to your mobile phone was cool and experts worried about a “digital divide” that advantages affluent kids with more screen time. Today, The New York Times is identifying a reverse digital divide that advantages affluent kids with less screen time.

Beyond the rebellion against rising digital time, we also pointed out in February a related rebellion against digital ads. Millennials are by far the most averse to digital ads, which is why a large and rising share of them are using ad-blocking software. What’s even worse for Google and Facebook, from a phase-of-life perspective, is that those Millennials who can afford it are highly motivated to subscribe to ad-free (or just “ad-lite”) content behind paywalls. This movement shows no sign of abating, with a growing number of elite and aspirational brands—from The New York Times and The Economist to HBO, Netflix, and (coming soon) Disney—choosing to thrive “off limits” to DoubleClick or AdSense. In time, we warned, all those ads cluttering the Googleverse and Facebook feeds may start making these places seem down-market.

We haven’t even mentioned yet the biggest news of the last summer and fall: the data-privacy scandals and politicized disinformation campaigns.

Google recently came under fire when it was discovered that the company failed to disclose a software glitch that left 500,000 Google+ users vulnerable to cyberattacks. Facebook’s dalliance with Cambridge Analytica was followed months later by a separate hack that exposed the Facebook profiles of nearly 50 million users. Politicized “fake news” spread on Facebook has become a tool of government regimes in Russia, Brazil, Myanmar, the Philippines, and elsewhere. The lengthy New York Times analysis of Facebook’s paranoid response to all these difficulties surely did nothing to reassure consumers—or investors.

All told, one senses genuine fatigue and distress among many users. This shift is too recent to show up yet in brand rankings. But we suspect the rankings will start registering them over the coming year.

For Google, tech-lash’s main role may be to help regulators build an antitrust case (more on that below). For Facebook, the impact of tech-lash can be observed more directly—in the company’s very fundamentals. Tech-lash is directly implicated in Facebook’s stagnant user growth. It has caused Americans to change the nature of their relationship with Facebook, either by checking the platform less frequently or by deleting their Facebook app entirely. How-to guides for living a Facebook-free life have transformed into a bona fide literature genre. Some even contend thatconsumers should be able to sue Facebook for damages stemming from data breaches.

Bottom line: The tech-lash headwind is intensifying.

Growing political threats at home. As we pointed out in February, America is not the political safe haven for Big Tech that it once was. Just three years ago, late in Obama’s presidency, the political horizon seemed cloud-free for both firms. Today, dark thunderheads are building up on every front.

On the left, the tarnishing of Google’s and Facebook’s reputation only starts with the possibility that their paid-for disinformation, in part funded by Vladimir Putin, may have put Donald Trump in the White House. Much worse is the Democratic Party’s post-election drift leftward on most policy issues (see: "The Next Big Thing: The 2018 Midterms: A Tale of Two Americas"), which has given new clout to progressives who were never comfortable with Obama’s and Clinton’s friendship with Big Tech. To them, both Google and Facebook are precisely the sort of gargantuan monopolist (or in their case, perhaps, duopolist) that the Sherman and Clayton antitrust acts were supposed to destroy or prevent. So why are they still around? Progressive think tanks are now working overtime to customize and perfect the legal arguments that would deal a death blow to each of them in turn.

A few years ago, Democratic candidates running for national office eagerly sought contributions and endorsements from these firms and their execs. Today, they had better keep their distance. Indeed, it is fair to say that none can afford not to champion aggressive regulation and antitrust enforcement against Big Tech. Elizabeth Warren, first to announce her candidacy in 2020, is a committed anti-monopolist. (Warren, remember, lauded the EU for levying a $5 billion antitrust fine against Google last summer.) Don’t expect any other Democratic contender to disagree.

In the Republican party, meanwhile, the news is hardly any better. And that’s because the GOP’s strengthening populist wing has its own reasons for hating Big Tech. For starters, populists on the right accuse Big Tech (and Silicon Valley more generally) of liberal bias: They charge Google in particular with suppressing conservative voices and biasing its search results toward left-leaning publications. Like all populists, moreover, they are deeply suspicious of big business and market power and are hardly more inclined to defend these firms than the firebrands on the left.

A good bellwether is Josh Hawley, the conservative young attorney general of Missouri who recently joined forces with other state AGs, many of them progressive Democrats, to bring antitrust cases against Google, Facebook, and other Big Tech companies. (His boyhood hero was GOP trust-buster Teddy Roosevelt.) Last fall, he was newly elected to the Senate, where he joins other Republicans like Orrin Hatch and Ted Cruz in denouncing Big Tech. President Trump himself recently reported that his administration is looking “very seriously” at the possibility of antitrust action specifically against Google, Facebook, and Amazon. Even such bastions of laissez-faire purity as the University of Chicago now favor stronger antitrust enforcement against firms with obvious pricing power—which may explain why so few libertarians have been speaking out in their defense.

What should investors make of all this? Well, one thing is clear: When both MSNBC’s Rachel Madow and Fox News’ Tucker Carlson both start inveighing regularly against the same companies, watch out. You might just be seeing social plate tectonics that are about to give way.

Investors may suppose they’ll have plenty of warning time before lawmakers or regulators get together and agree on policy changes. But that’s not necessarily how an antitrust action against Google or Facebook will work. One day, out of nowhere, the Justice Department or the FTC may announce their case—and within minutes (depending on the seriousness of the charge) the ticker could be down double digits. The only sure warning signs in the great historic cases like Standard Oil or AT&T or Microsoft were growing prior public awareness of possible antitrust violations and widespread prior efforts to bring action at the state level.

For Google and Facebook, all that has already happened. In other words, you have been officially warned.

Growing political threats abroad. If anything, the United States has been late to the party when it comes to being tough on Google and Facebook. Europe has long been the standard-bearer in the battle against U.S. Big Tech firms.

Data privacy has been one major battleground. In May, Europe implemented its sweeping general data-privacy regulations (GDPR), which among other things mandates that companies gain opt-in consent before sharing consumer data. Bad news for both companies: Americans, when asked, overwhelmingly favor GDPR in their own country.

There’s no mistaking GDPR as anything but a European shot against America’s tech titans. On the first day of enforcement, Google and Facebook were hit with lawsuits totaling $8.8 billion over their noncompliance. Germany has been particularly hawkish in its pursuit of data abusers: Led by antitrust czar Andreas Mundt, Germany’s Federal Cartel Office currently is investigating Facebook’s data-mining practices.

Antitrust has been another battleground. In the United States, proponents of stricter antitrust enforcement face an often-insurmountable obstacle: a national libertarian “spidey-sense” that is triggered by anything resembling government overreach. In Europe, no such tradition exists—and it shows.

Last year, EU regulators hit Google with a record $5 billion fine stemming from its dominance of the smartphone OS market. The EU also has been asked to open an inquiry into antitrust activity in the digital ad market. Germany has not waited for the EU to act: Its Federal Cartel Office recently completed an antitrust probe into Facebook, with results forthcoming. (For the record, Jochen Homann, the head of Germany’s network agency, says that these firms should be regulated like telecoms.) Nations including Japan and Australia have taken a cue from the Germans and have launched their own investigations into U.S. Big Tech practices.

Analysts point out that Google faces a special kind of peril abroad because of its sheer dominance of multiple business lines—advertising, smartphone operating systems, and Web search. But make no mistake: Both of these firms find themselves squarely within the regulatory crosshairs. A quickening flow of lawsuits, sanctions, and PR hits is a very real possibility.

GOOGLE VERSUS FACEBOOK

Thus far we have mainly been looking at the prospects of Google and Facebook by emphasizing what they both have in common. Which is a lot. Here we have two mega-cap Silicon Valley firms whose nearly exclusive source of revenue is selling digital advertising, an industry these two firms dominate, both in terms of market share and growth share.

But clearly in recent months investors have been struck by their differences.

Google—whose brand equity still ranks number one in most surveys and whose tech wizardry keeps awing the public—seems to sail above much of the popular backlash. Google CEO Sundar Pichai smiles indulgently at those who don’t quite understand. Not so Facebook, whose investors seem riveted on every bit of bad news that blows up in the blank face of CEO-owner Mark Zuckerberg or the nervous face of COO Sheryl Sandberg.

As each bad-news story hit, so did the price fall.

In June came a Pew Research survey showing that Facebook is no longer the most-often used online platform used by teens—that honor now going to Google-owned YouTube and Snapchat (with Facebook-owned Instagram taking third place). In August came a market research study showing that Facebook’s monthly page visits have plummeted by half over the past two years (down to 4.7 billion). Facebook.com is poised to lose its ranking as the #2 most-visited U.S. website to none other than YouTube. (Google.com owns the top spot, with 15 billion monthly visits.) Yet another study in October said that every measure of Facebook user time per person YoY was dropping.

Investors have also fretted over news that Facebook, along with most other social networks, has lost its bargaining power with ad buyers who are seeking addressable audiences over sheer traffic. Nor does it help that Facebook is facing a lawsuit in which the company is accused of overstating the amount of time users spent watching videos on its site by 150-900%—which must give advertisers pause. Ad business executives, like Robin O’Neill of GroupM, are no longer taking Facebook’s metrics for granted: “We’re increasingly holding Facebook to account to justify the levels of investment we are putting in them… We continue to press them to allow us to independently verify our metrics and operate in the real world.”

Google seems to be spared of all this bad press. Investors apparently believe that Google will transcend whatever ills afflict the digital ad business, despite the fact that 86% of its revenue—and an even larger share of its earnings—come from ads. The company is now endeavoring to take a cut of the e-commerce market with its new Google Shopping service. Investors dream of multiple future pots of gold: from Android licensing, cloud computing, and hardware to driverless cars (Waymo), AI diagnostics (Deep Mind), or even longevity elixirs (Calico).

Our opinion? Both Google and Facebook are trying to meet challenging revenue expectations in a difficult industry, for all the reasons we have discussed. But while Facebook has taken a beating as some of those challenges have turned into headlines, Google has undeservingly been spared.

Of the two names, Google is already our preferred near-term short given the likely YoY shock contained within the upcoming Q4 earnings report (see above). But it’s also our preferred near-term short because, from any conceivable valuation perspective, it still has a lot more to fall.

Look at the fundamentals. For years, Google was the larger, slower-growing company with the smaller multiple—while Facebook was the smaller, faster-growing company with the larger multiple. This made perfect sense: Investors were willing to pay more for every dollar of Facebook’s earnings because of its growth potential. But Facebook’s large recent price decline has thrown this relationship out of whack. Google now has a P/E ratio that’s twice as high as Facebook’s—although no one is suggesting that Google, in the foreseeable future, will grow as fast as Facebook or match its operating margin. Draw your own conclusions.

WHAT THE FUTURE HOLDS

A very real danger for both firms going forward is the Internet’s continued transformation into an infinite number of closed-loop “walled gardens.”

The maturation of the Internet and the rise of mobile IT have enabled companies of all shapes and sizes to build closed-loop systems. Making this venture all the more compelling has been the continued shift toward digital advertising: If you have a good enough app that people never want to leave, it gives you a huge addressable market and a great deal of bargaining power with ad companies. If you’re big enough, you can even start contracting with advertisers on your own.

This is obviously a nightmare scenario for Google, which thrives in a free and open Web where everyone starts their search on Google.com. As badly as Google wants its “Knowledge Panels” to send users on a never-ending journey through Google pages, the vast majority of the mobile-centric walled-garden world is inaccessible to Google—unless it buys its way in by paying a king’s ransom to Apple and other gatekeepers.

A closed Internet would seem to benefit Facebook, which is itself a walled garden. But here’s the important distinction: Today’s consumers are insisting, ever more loudly, that they want their walled gardens to be exclusive, intimate, small-scale experiences. At its outset, Facebook was this type of place—a site where users could connect with their small group of college friends. But years of trying to “make the world more open and connected” have de-emphasized personal connection, transforming Facebook into a humming borderless throng where you are just as likely to see posts from strangers as from friends.

As a result, Facebook is not so much beloved as it is viewed as an obligation. Quite simply, most users are more connected than they want to be. Tech author Clive Thompson got this sense when he was interviewing subjects for an upcoming book: “In three years of research and talking to hundreds of people and everyday users, I don’t think I heard anyone say once, ‘I love Facebook.’”

Facebook itself seems to be admitting that it may have lost its way. Zuckerberg started the company’s Q3 earnings call by emphasizing Facebook’s shift toward stories, and away from News Feed, acknowledging that, “People feel more comfortable being themselves when they know their content will only be seen by a smaller group.” The company in recent years has also doubled down on its private groups as a source of comfort for users who crave like-minded community.

This is a remarkable about-face by the social-media giant. Over the last decade, both Facebook and Google have repeatedly been described by economists as firms with infinite economies of scale. Which means, thanks mostly to the “network effect,” that the larger they are, the more profitable they are. This is what gives them pricing power. This is what makes them so incredibly attractive to investors. This is what makes them such obvious targets of antitrust enforcement.

But what if the economists are wrong? What if it turns out, in our emerging post-globalist era, that most people don’t actually want to be connected to Zuckerberg’s “billions”—nor do they want to be microscopically pored over by every marketing firm on the planet? In other words, what if bigness comes to be regarded by most consumers as a negative?

To be sure, Google and Facebook will continue to be growing and profitable firms for many years to come. Their deep pockets will enable them to invade whole new industries overnight. (Next up: Google into music streaming? Facebook into online dating?). But if sheer size is no longer their ally, that growth rate will inevitably start inflecting down—and those new businesses may be no more profitable after they are purchased than before. And that possibility will affect valuation premiums today.