Editor's Note: Below is an excerpt from a Demography Unplugged research note written by Demography analyst Neil Howe. Click here to get complimentary access to the entire research report.

TREND WATCH: What’s Happening? With a turbulent 2018 behind us, forecasters have turned their attention to 2019 and beyond. While most outlets have adopted a bearish-to-cautious view of the future, Morgan Stanley is unflinchingly optimistic. The firm contends that favorable demographic trends, specifically a “youth boom” powered by a rising crop of “Gen Zers,” will push U.S. GDP growth to unforeseen heights by the end of the next decade. Once you account for demography, MS argues, the 2020s look far better than the picture painted by the official forecasters.

Our Take: We are unpersuaded. Morgan Stanley relies on framing, hand-waving, and faulty assumptions in its analysis. Upon closer examination, the full force of the demographic tailwinds referred to in the report won’t hit until the 2030s and 2040s. And even when they do arrive, their impact won’t be as positive as advertised. An honest assessment of the future—one built on realistic assumptions of working-age population, employment, and productivity growth rates—is a lot more sobering.

After a year marked by tariff wars, interest-rate hikes, slowing global growth, and stock-market selloffs, you’ve got to admire those who look past the headlines and find reasons to be long-term bullish on the U.S. economy. And not just long-term bullish, but long-term bullish for demographic reasons.

That’s what makes a new report out of Morgan Stanley, The Coming Youth Boom: When Generations Y & Z Combine, so noteworthy. Analysts who know the numbers tend to regard the stagnation in workforce growth over the next decade as pretty much written in stone.

Morgan Stanley begs to differ. The report’s authors contend that “demographic headwinds turn into tailwinds starting in the 2020s, and are long-term bullish for the U.S.” A new “youth boom,” they say, will push employment, consumption, and GDP significantly above the levels that official agencies like the Congressional Budget Office are now projecting. Moreover, Morgan Stanley accuses official forecasters of understating the impact that these “tailwinds” will have on U.S. GDP growth. Indeed, so big is this boom that Social Security and Medicare may be in much better shape than anyone realizes; their expected official insolvency dates may be postponed “perhaps by decades.”

This last claim triggered gee-whiz headlines in MarketWatch and Yahoo Finance. It also triggered a withering reply from Chuck Blahous, a seasoned expert on Social Security who has served on its Board of Actuaries. (While the Morgan Stanley study itself has not been officially released to the public, it has been fed to the financial media and widely circulated among clients and friends of MS.)

IS A “YOUTH BOOM” COMING SOON?

As demographers ourselves, we feel compelled to respond to these assertions. Is a “youth boom” coming soon? Does Morgan Stanley know something that the rest of us have overlooked? Have all the researchers publishing for years in mainstream institutions—like the U.S. Census Bureau, the U.N. Population Division, and the CBO—really gotten things very wrong?

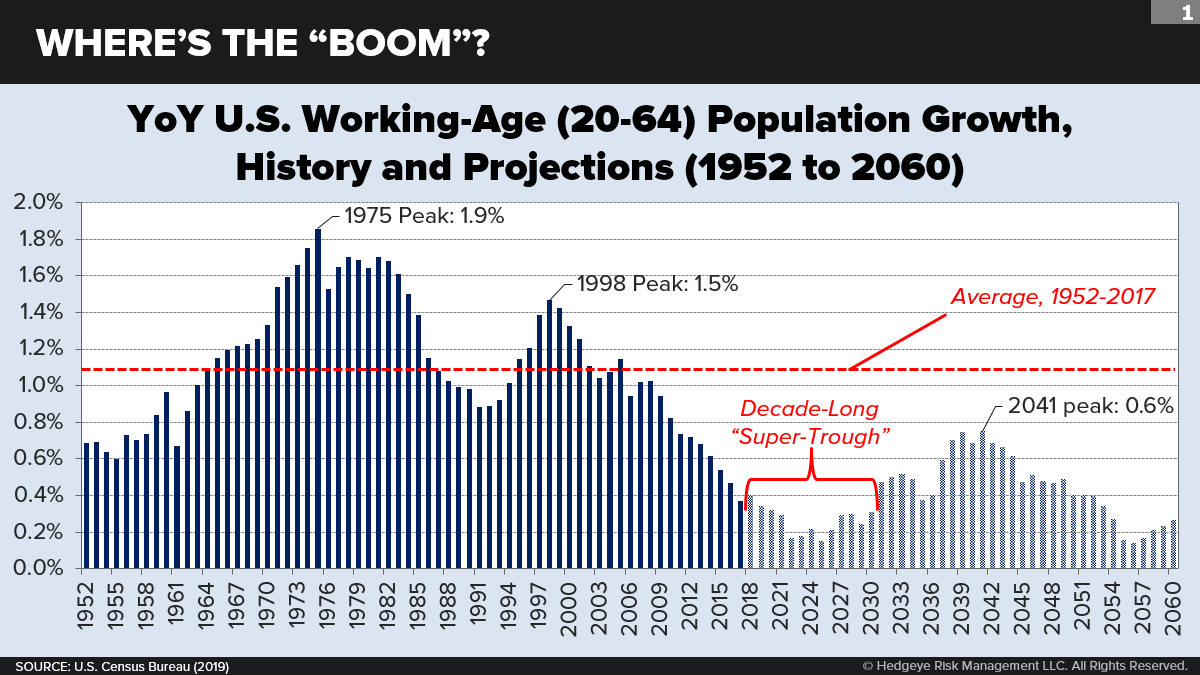

Let’s start by summing up the gist of the mainstream projections. Basically, they say that the growth rate of the U.S. working-age population, which has been slowing dramatically over the last two decades, will reach a historic low during most of the 2020s before rising modestly and temporarily in the 2030s and 2040s. (See chart below.) The boomlet of the 2030s and 2040s will happen as the children of the relatively large Millennial Generation reach working age and as a relatively small Generation X starts retiring.

Right now, and throughout the next ten years, the opposite is happening: A relatively small late-wave Millennial and Homeland Generation is entering the workplace and a relatively large Boom Generation is retiring.

That leaves the 2020s as a uniquely grim decade if you’re looking for growth in the working-age population. At just +0.2% per year, the average growth rate in the 2020s will be barely above zero. This figure is vastly lower than working-age population growth in any earlier decade in U.S. history and is almost certainly lower than any future decade until (possibly) the 2050s. The pessimistic consequences for GDP growth follow suit. Unless you have good reason to expect a dramatic change in labor force participation rates or labor productivity, the slump in the working-age population flows through directly to a slump in expected GDP growth.