Editor's Note: Below is a brief excerpt from Market Edges, our weekly big picture Macro newsletter. Click here to learn more about Market Edges.

So far, 431 of S&P 500 companies have reported aggregate year-over-year EPS growth of +10.9%. That’s down big time from the #PeakCycle Q318 growth rate of +26.2% y/y.

As we continue to remind investors, earnings recessions have always lead broader recessions. Meanwhile, our domestic and global growth forecasts suggest growth is slowing.

Looking at the 2001-2002 slowdown, you can see how fast earnings slowed after peaking in 3Q 2000 at 22.9% for the S&P 500. Just four quarters later, by the third quarter of the following year, earnings growth troughed at -18.2%.

The S&P 500 fell more than -48% from the 2000 highs to the 2002 lows.

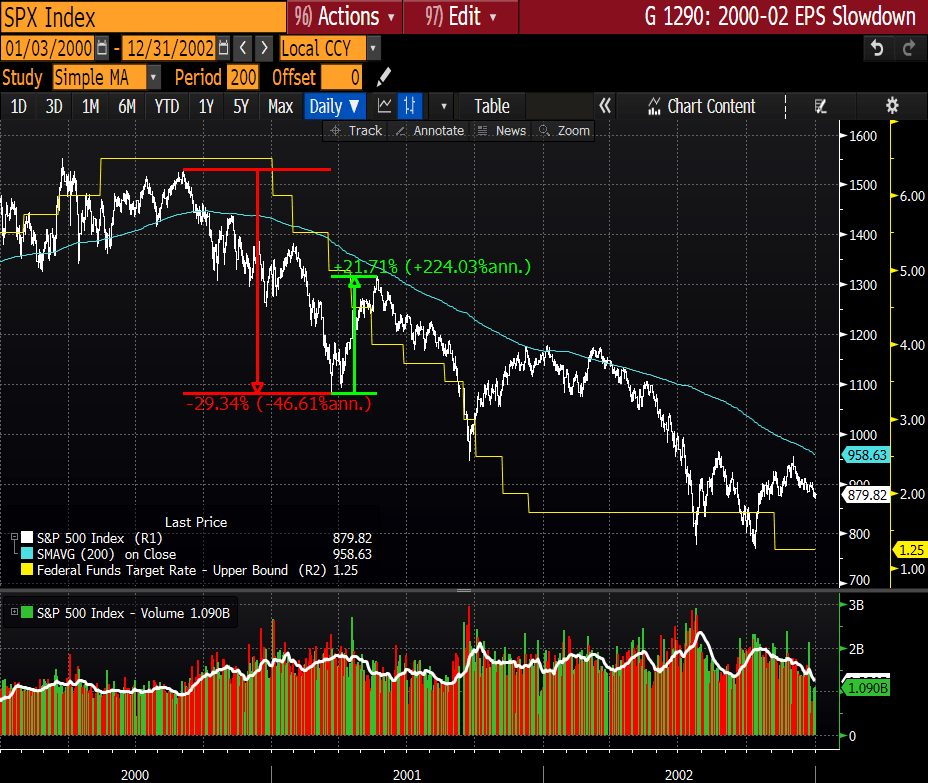

Is it the 2001-2002 slowdown all over again? Stock market bulls like to say that the Fed can rescue equities from the slowdown, but looking at the chart 2001-2002 slowdown chart below, you can see the Fed cut the Fed Funds rate from 6.25% all the way to 1.25% and stocks plummeted anyway.

To be sure, there were some sharp bounces to lower highs. After stocks dropped -29% from the 2000 highs to a new low in early 2001, the S&P 500 rallied 21.7% before continuing to tumble to the 2002 lows.

That's the thing about Fed cowbell, by the time they get around to implementing rate cuts, it's on a lag and we'll likely have already traversed the hardest parts of the growth curve. Try as he might Donald J. Powell is unlikely to trump #TheCycle.